ADT 2008 Annual Report Download - page 156

Download and view the complete annual report

Please find page 156 of the 2008 ADT annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

|

|

would be required to pay, equally with any other non-defaulting party, the amounts in default. In

addition, if another party to the Tax Sharing Agreement that is responsible for all or a portion of an

income tax liability were to default in its payment of such liability to a taxing authority, the Company

could be legally liable under applicable tax law for such liabilities and required to make additional tax

payments. Accordingly, under certain circumstances, the Company may be obligated to pay amounts in

excess of its agreed-upon share of Tyco’s, Covidien’s and Tyco Electronics’ tax liabilities. See Note 14 to

the Consolidated Financial Statements for further discussion of guarantees and indemnifications

extended between Tyco, Covidien and Tyco Electronics.

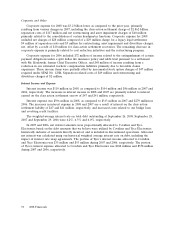

Other Income Tax Matters

The Company and its subsidiaries’ income tax returns periodically are examined by various tax

authorities. In connection with these examinations, tax authorities, including the Internal Revenue

Service (‘‘IRS’’), have raised issues and proposed tax adjustments. The Company is reviewing and

contesting certain of the proposed tax adjustments. Management has assessed the issues related to

these adjustments for recognition and measurement under FIN No. 48 and has recorded unrecognized

tax benefits in accordance with FIN No. 48. The ultimate resolution of these matters is uncertain and

could result in a material impact to the Company’s financial position, results of operations, cash flows

or the effective tax rate in future reporting periods.

In 2004, in connection with the IRS audit of the 1997 through 2000 years, the Company submitted

to the IRS proposed adjustments to these prior period U.S. federal income tax returns resulting in a

reduction in the taxable income previously filed. During 2006, the IRS accepted substantially all of the

proposed adjustments, and the Company developed proposed amendments to U.S. federal income tax

returns for additional periods through 2002. On the basis of previously accepted amendments, the

Company has determined that these adjustments will more-likely-than-not be accepted and, accordingly,

has recorded them in the Consolidated Financial Statements. Such adjustments did not have a material

impact on the Company’s financial condition, results of operations or cash flows.

Additionally, during 2008 the Company completed proposed amendments to its U.S. federal

income tax returns for periods subsequent to 2002, which primarily reflect the roll forward through

2006 of the amendments for the periods 1997 to 2002. Such adjustments did not have a material impact

on the Company’s financial condition, results of operations or cash flows. While the final adjustments

cannot be determined until the income tax return amendment process and the IRS review is completed,

the Company believes that any resulting adjustments will not have a material impact on its financial

condition, results of operations or cash flows.

During the third quarter of 2007, the IRS concluded its field examination of certain of Tyco’s U.S.

federal income tax returns for the years 1997 though 2000 and issued anticipated Revenue Agents’

Reports (‘‘RARs’’) which reflect the IRS’ determination of proposed tax adjustments for the periods

under audit. The RARs propose tax audit adjustments to certain of the Company’s previously filed tax

return positions. The Company agreed with the IRS on adjustments totaling $498 million, with an

estimated cash impact to the Company of $458 million, and during the third quarter of 2007, the

Company paid $458 million, of which $163 million related to the Company’s discontinued operations.

The Company appealed other proposed tax audit adjustments totaling approximately $1 billion relating

to Tyco, Covidien and Tyco Electronics, and, as Audit Managing Party as specified in the Tax Sharing

Agreement, the Company intends to vigorously defend its prior filed tax return positions.

During the second quarter of 2008, the IRS issued additional RARs asserting a withholding tax

liability of approximately $106 million associated with the prior proposed tax adjustments related to

Tyco, Covidien and Tyco Electronics for the 1997 to 2000 period. The withholding tax amount asserted

against Tyco is immaterial. During the first quarter of fiscal 2009, the Company reached an agreement

with the IRS appeals team to work towards timely resolution of all unagreed issues related to this time

period. The Company, as Audit Managing Party as specified in the Tax Sharing Agreement, intends to

2008 Financials 53