TCF Bank 2005 Annual Report Download - page 83

Download and view the complete annual report

Please find page 83 of the 2005 TCF Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

|

|

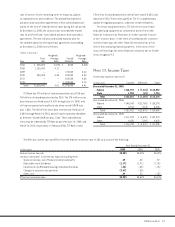

632005 Form 10-K

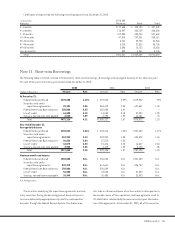

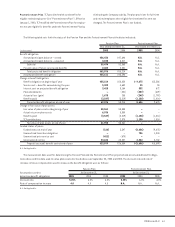

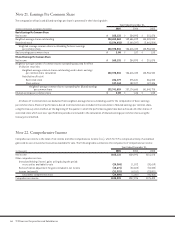

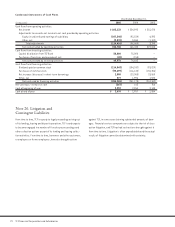

The following are expected future benefit payments used to

determine projected benefit obligations:

Pension Postretirement

(In thousands) Plan Plan

2006 $ 6,562 $ 863

2007 5,863 841

2008 6,182 826

2009 6,310 806

2010 6,576 762

2011-2015 36,796 3,360

The following table presents assumed health care cost trend

rates for the Postretirement Plan at December 31, 2005 and 2004:

2005 2004

Health care cost trend rate assumed

for next year 8.6% 10%

Final health care cost trend rate 5% 5%

Year that final health care trend rate

is reached 2009 2009

Assumed health care cost trend rates have an effect on the

amounts reported for the Postretirement Plan. A one-percentage-

point change in assumed health care cost trend rates would have

the following effects:

1-Percentage-Point

(In thousands) Increase Decrease

Effect on total of service and interest

cost components $ 33 $ (20)

Effect on postretirement

benefits obligations 364 (298)

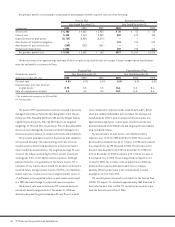

Note 18. Derivative Instruments

and Hedging Activities

TCF had no derivatives outstanding as of December 31, 2005

and 2004.

Prior to the restructuring of the residential mortgage banking

operation in 2004, TCF’s pipeline of locked residential mortgage

loan commitments, adjusted for loans not expected to close, and

forward sales contracts were considered derivatives and recorded

at fair value, with the changes in fair value recognized in gains on

sales of loans under mortgage banking revenue in the Consolidated

Statements of Income. TCF also utilized forward sales contracts

to hedge its risk of changes in the fair value, due to changes

in interest rates, of both its locked residential mortgage loan

commitments and its residential loans held for sale. Residential

mortgage loans held for sale were carried at the lower of cost

or market as adjusted for the effects of fair value hedges using

quoted market prices. Because the fair value of the residential

loans held for sale were hedged with forward sales contracts of

the same loan types, or substantially the same loan types, the

hedges were highly effective at managing the risk of changing

fair values of such loans. Any differences between the changes

in fair value of the hedged residential loans held for sale and in

the fair value of the forward sales contracts were not material

due to the nature of the hedging instruments and were recorded

in gains on sales of loans.

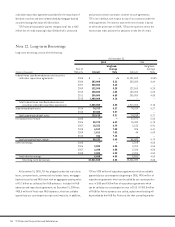

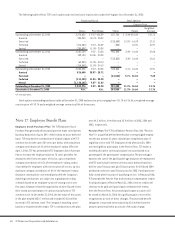

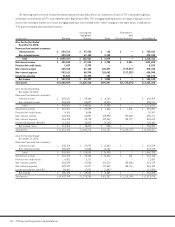

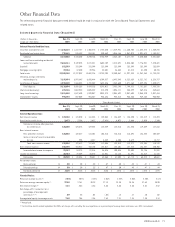

Note 19. Financial Instruments

with Off-Balance Sheet Risk

TCF is a party to financial instruments with off-balance sheet

risk, primarily to meet the financing needs of its customers.

These financial instruments, which are issued or held by TCF

for purposes other than trading, involve elements of credit and

interest-rate risk in excess of the amount recognized in the

Consolidated Statements of Financial Condition.

TCF’s exposure to credit loss in the event of non-performance

by the counterparty to the financial instrument for commitments

to extend credit and standby letters of credit is represented by the

contractual amount of the commitments. TCF uses the same credit

policies in making these commitments as it does for on-balance

sheet instruments. TCF evaluates each customer’s creditworthiness

on a case-by-case basis. The amount of collateral obtained is

based on management’s credit evaluation of the customer.

Financial instruments with off-balance sheet risk are summa-

rized as follows:

At December 31,

(In thousands) 2005 2004

Commitments to extend credit:

Consumer home equity and other $1,750,738 $1,576,381

Commercial 811,652 684,029

Leasing and equipment finance 74,418 72,614

Other 77,766 55,343

Total commitments to

extend credit 2,714,574 2,388,367

Loans serviced with recourse 71,332 97,568

Standby letters of credit and

guarantees on industrial

revenue bonds 100,892 75,957

Total $2,886,798 $2,561,892

Commitments to Extend Credit Commitments to extend credit

are agreements to lend to a customer provided there is no violation

of any condition in the contract. These commitments generally

have fixed expiration dates or other termination clauses and may

require payment of a fee. Since certain of the commitments are