TCF Bank 2005 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2005 TCF Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

|

|

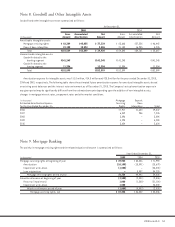

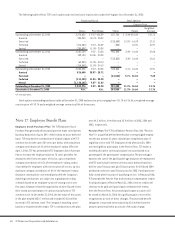

54 TCF Financial Corporation and Subsidiaries

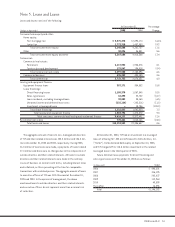

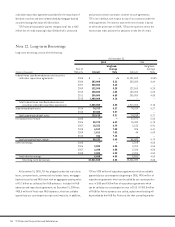

The following table represents the components of mortgage

banking revenue:

Year Ended December 31,

(In thousands) 2005 2004 2003

Servicing income $13,998 $17,349 $ 20,533

Less mortgage servicing:

Amortization 10,108 13,091 23,679

(Recovery) provision

for impairment (1,000) 1,500 21,154

Subtotal 9,108 14,591 44,833

Net servicing

income (loss) 4,890 2,758 (24,300)

Gains on sales of loans (1) –8,107 33,505

Other income 688 2,095 3,514

Total mortgage

banking revenue $ 5,578 $12,960 $ 12,719

(1) Beginning in 2005, TCF’s mortgage banking business no longer originates or

sells loans.

Gains on sales of loans include the changes in fair value of

residential mortgage loans held for sale, loan applications in

process and related forward sales contracts. At December 31,

2004 and 2005, there were no residential mortgage loans held

for sale or related forward sales contracts.

At December 31, 2005, 2004 and 2003, TCF was servicing real

estate loans for others with aggregate unpaid principal balances

of approximately $3.4 billion, $4.5 billion and $5.1 billion,

respectively. At December 31, 2005 and 2004, TCF had custodial

funds of $74.1 million and $106.1 million, respectively, related to

the servicing of residential real estate loans, which are included

in deposits in the Consolidated Statements of Financial Condition.

These custodial deposits relate primarily to mortgage servicing

operations and represent funds due to investors on mortgage

loans serviced by TCF and customer funds held for real estate

taxes and insurance.

The estimated fair value of mortgage servicing rights

included in the Consolidated Statements of Financial Condition

at December 31, 2005 was approximately $45.7 million. The

estimated fair value is based on estimated cash flows discounted

using rates management believes are commensurate with the

risks involved. Assumptions regarding prepayments, defaults and

interest rates are determined using available market information.

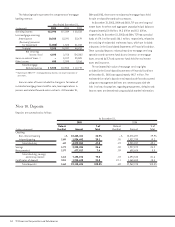

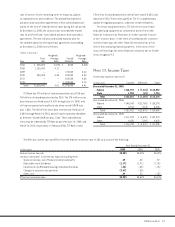

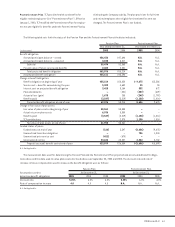

Note 10. Deposits

Deposits are summarized as follows:

At December 31,

2005 2004

Rate at % of Rate at % of

(Dollars in thousands) Year End Amount Total Year End Amount Total

Checking:

Non-interest bearing –% $2,445,411 26.9% –% $2,378,697 29.9%

Interest bearing 1.60 1,834,442 20.1 .55 1,527,290 19.2

Total checking .69 4,279,853 47.0 .22 3,905,987 49.1

Savings 1.77 2,238,204 24.6 .59 1,927,872 24.2

Money market 1.97 677,017 7.4 .59 659,686 8.3

Total checking, savings,

and money market 1.14 7,195,074 79.0 .37 6,493,545 81.6

Certificates of deposit 3.51 1,915,620 21.0 2.11 1,468,650 18.4

Total deposits 1.64 $9,110,694 100.0% .69 $7,962,195 100.0%