TCF Bank 2005 Annual Report Download - page 25

Download and view the complete annual report

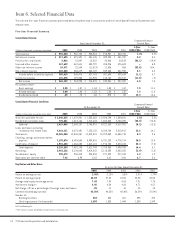

Please find page 25 of the 2005 TCF Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

|

|

52005 Form 10-K

Regulatory Capital Requirements TCF Financial and TCF Bank

are subject to regulatory capital requirements of the FRB and the

OCC, respectively. These requirements are described below. In

addition, these regulatory agencies are required by law to take

prompt action when institutions do not meet certain minimum

capital standards. The Federal Deposit Insurance Corporation

Improvement Act of 1991 (“FDICIA”) defines five levels of capital

condition, the highest of which is “well-capitalized.” It requires that

regulatory authorities subject undercapitalized institutions to

various restrictions such as limitations on dividends or other capi-

tal distributions, limitations on growth or activity restrictions.

Undercapitalized banks must also develop a capital restoration

plan and the parent financial holding company is required to

guarantee compliance with the plan. TCF Financial and TCF Bank

are “well-capitalized” under the FDICIA capital standards.

The FRB and the OCC also have adopted rules that could permit

them to quantify and account for interest-rate risk exposure and

market risk from trading activity and reflect these risks in higher

capital requirements. New legislation, additional rulemaking, or

changes in regulatory policies may affect future regulatory capital

requirements applicable to TCF Financial and TCF Bank. The ability

of TCF Financial and TCF Bank to comply with regulatory capital

requirements may be adversely affected by legislative changes or

future rulemaking or policies of their regulatory authorities or by

unanticipated losses or lower levels of earnings.

Restrictions on Distributions Dividends or other capital

distributions from TCF Bank to TCF Financial are an important

source of funds to enable TCF Financial to pay dividends on its

common stock, to make payments on TCF Financial’s borrowings,

or for its other cash needs. TCF Bank’s ability to pay dividends is

dependent on regulatory policies and regulatory capital require-

ments. The ability to pay such dividends in the future may be

adversely affected by new legislation or regulations, or by changes

in regulatory policies. In general, TCF Bank may not declare or

pay a dividend to TCF Financial in excess of 100% of its net profits

during a year combined with its retained net profits for the pre-

ceding two years without prior approval of the OCC. TCF Bank’s

ability to make capital distributions in the future may require

regulatory approval and may be restricted by its regulatory author-

ities. TCF Bank’s ability to make any such distributions may also

depend on its earnings and ability to meet minimum regulatory

capital requirements in effect during future periods. These capital

adequacy standards may be higher than existing minimum capital

requirements. The OCC also has the authority to prohibit the

payment of dividends by a national bank when it determines such

payments would constitute an unsafe and unsound banking prac-

tice. In addition, income tax considerations may limit the ability

of TCF Bank to make dividend payments in excess of its current

and accumulated tax “earnings and profits” (“E&P”). Annual div-

idend distributions in excess of E&P could result in a tax liability

based on the amount of excess earnings distributed and current

tax rates. See “Management’s Discussion and Analysis of

Financial Condition and Results of Operations — Consolidated

Financial Condition Analysis – Liquidity Management” and Note

14 of Notes to Consolidated Financial Statements.

Regulation of TCF Financial and Affiliates and Insider

Transactions TCF Financial is subject to FRB regulations, exami-

nations and reporting requirements relating to bank or financial

holding companies. As a subsidiary of a financial holding company,

TCF Bank is subject to certain restrictions in its dealings with

TCF Financial and with companies affiliated with TCF Financial.

A holding company must serve as a source of strength for its

subsidiary banks, and the FRB may require a holding company to

contribute additional capital to an undercapitalized subsidiary

bank. In addition, Section 55 of the National Bank Act may permit

the OCC to order the pro rata assessment of shareholders of a

national bank where the capital of the bank has become impaired.

If a shareholder fails to pay such an assessment within three

months, the OCC may order the sale of the shareholder’s stock to

cover a deficiency in the capital of a subsidiary bank. In the event

of a holding company’s bankruptcy, any commitment by the hold-

ing company to a federal bank regulatory agency to maintain the

capital of a subsidiary bank would be assumed by the bankruptcy

trustee and may be entitled to priority over other creditors.

Under the Bank Holding Company Act (“BHCA”), a bank hold-

ing company must obtain FRB approval before acquiring more

than 5% control, or substantially all of the assets, of another

bank, or bank or financial holding company, or merging or con-

solidating with such a holding company. The BHCA also generally

prohibits a bank holding company, with certain exceptions, from

acquiring direct or indirect ownership or control of more than

5% of the voting shares of any company which is not a bank or

bank holding company, or from engaging directly or indirectly in

activities other than those of banking, managing or controlling

banks, providing services for its subsidiaries, or conducting

activities permitted by the FRB as being closely related and

proper incidents to the business of banking.