TCF Bank 2005 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2005 TCF Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

|

|

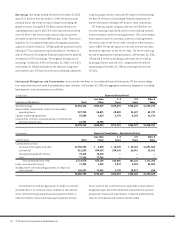

46 TCF Financial Corporation and Subsidiaries

Note 1. Summary of Significant

Accounting Policies

Basis of Presentation The consolidated financial statements

include the accounts of TCF Financial Corporation and its wholly

owned subsidiaries. TCF Financial Corporation (“TCF” or the

“Company”) is a Delaware national financial holding company

engaged primarily in community banking and leasing and equip-

ment finance through its wholly owned subsidiary, TCF Bank.

TCF Bank owns leasing and equipment finance, mortgage banking,

securities brokerage and investment and insurance sales, and

Real Estate Investment Trust (“REIT”) subsidiaries. These

subsidiaries are consolidated with TCF Bank and are therefore

included in the consolidated financial statements of TCF Financial

Corporation. All significant intercompany accounts and transac-

tions have been eliminated in consolidation.

Certain reclassifications have been made to prior years’

financial statements to conform to the current year presentation.

For Consolidated Statements of Cash Flows purposes, cash and

cash equivalents include cash and due from banks.

The preparation of financial statements in conformity with

generally accepted accounting principles requires management

to make estimates and assumptions that affect the reported

amounts of assets and liabilities and disclosure of contingent

assets and liabilities at the date of the financial statements and

the reported amounts of revenues and expenses during the report-

ing period. These estimates are based on information available to

management at the time the estimates are made. Actual results

could differ from those estimates.

Policies Related to Critical Accounting Estimates

Summary of Critical Accounting Estimates Critical account-

ing estimates occur in certain accounting policies and procedures

and are particularly susceptible to significant change. Policies that

contain critical accounting estimates include the determination of

the allowance for loan and lease losses, mortgage servicing rights,

lease financings, pension liability and expenses and income taxes.

Critical accounting policies are discussed with and reviewed by

TCF’s Audit Committee.

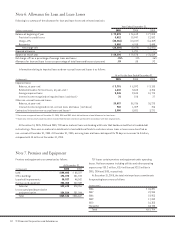

Allowance for Loan and Lease Losses The allowance for

loan and lease losses is maintained at a level believed to be

appropriate by management to provide for probable loan and

lease losses inherent in the portfolio as of the balance sheet date,

including known or anticipated problem loans and leases, as well

as for loans and leases which are not currently known to require

specific allowances. Management’s judgement as to the amount

of the allowance is a result of ongoing review of larger individual

loans and leases, the overall risk characteristics of the portfolios,

changes in the character or size of the portfolios, geographic

location and prevailing economic conditions. Additionally, the

level of impaired and non-performing assets, historical net

charge-off amounts, delinquencies in the loan and lease portfo-

lios, values of underlying loan and lease collateral and other

relevant factors are reviewed to determine the amount of the

allowance. In 2005, TCF refined its allowance for loan and lease

losses allocation methodology resulting in an allocation of the

entire allowance for loan and lease losses to the individual loan

and lease portfolios. This change resulted in the allocation of the

previous unallocated portion of the allowance for loan and lease

losses. Impaired loans include all non-accrual and restructured

commercial real estate and commercial business loans and

equipment finance loans. Consumer loans, residential real estate

loans and leases are excluded from the definition of an impaired

loan. Loan impairment is measured as the present value of the

expected future cash flows discounted at the loan’s initial effective

interest rate or the fair value of the collateral for collateral-

dependent loans. Consumer loans, residential loans, smaller-

balance commercial loans and leases and equipment finance loans

are segregated by loan type and sub-type, and are evaluated on

a pool basis. Loans and leases are charged off to the extent they

are deemed to be uncollectible. The amount of the allowance for

loan and lease losses is highly dependent upon management’s

estimates of variables affecting valuation, appraisals of collateral,

evaluations of performance and status, and the amounts and

timing of future cash flows expected to be received on impaired

loans. Such estimates, appraisals, evaluations and cash flows may

be subject to frequent adjustments due to changing economic

prospects of borrowers, lessees or properties. These estimates are

reviewed periodically and adjustments, if necessary, are recorded

in the provision for credit losses in the periods in which they

become known.

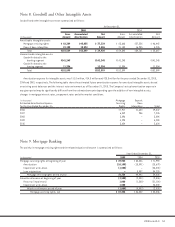

Mortgage Servicing Rights TCF records a mortgage servicing

rights asset for its right to service mortgage loans it has sold to

third parties, but continues to service for a fee. The total cost of

loans sold is allocated between the loans sold and the servicing

rights retained based on the relative fair values of each. Mortgage

servicing rights are initially recorded at cost and are subsequently

carried at the lower of cost, adjusted for amortization, or estimated

fair value. Mortgage servicing rights are amortized in proportion

to, and over the period of, estimated net servicing income.

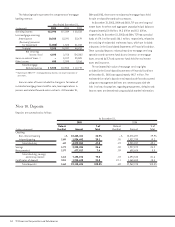

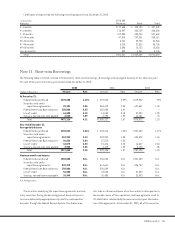

Notes to Consolidated Financial Statements