TCF Bank 2005 Annual Report Download

Download and view the complete annual report

Please find the complete 2005 TCF Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

|

|

TCF Financial Corporation

2005 Annual Report

The leader

in convenience banking

Table of contents

-

Page 1

TCF Financial Corporation 2005 Annual Report The leader in convenience banking -

Page 2

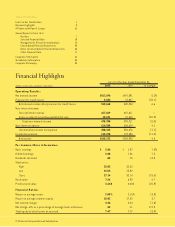

... Stock price: High Low Close Book value Price to book value Financial Ratios: Return on average assets Return on average common equity Net interest margin Net charge-offs as a percentage of average loans and leases Total equity to total assets at year end TCF Financial Corporation and Subsidiaries... -

Page 3

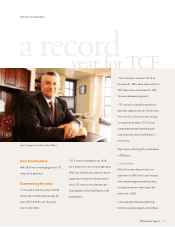

...TCF, it was still a good year. • TCF's return on average assets (ROA) was 2.08 percent, return on average equity (ROE) was 28.03 percent, and net interest margin was 4.46 percent. Based on these 1. Interest Rates While short-term interest rates rose eight times in 2005, the 10-year Treasury rate... -

Page 4

... strong. Consumer home equity loan credit quality remains very good, despite a slowing housing market and changes in the bankruptcy laws. However, there were two unusual credit events in 2005. First, there was a large non-recurring commercial loan recovery of $3.3 million. Second, we charged off our... -

Page 5

... equipment buyout transactions that did not reoccur in 2005. 4. Power Assets and Power Liabilities TCF's Power Asset lending operations continued to generate strong growth. Power Assets totaled $9.4 billion at the end of 2005 and increased 13 percent over the prior year. Consumer home equity loans... -

Page 6

... 14 percent in 2005. TCF's new premier products totaled $1.6 billion at year end and increased $973.9 million in 2005. For the first time in many years, TCF's Power Liability growth more than funded our Power Asset growth, which allowed us to decrease borrowings. 5. Asset Sale Gains TCF recorded $10... -

Page 7

...may slow in future Free Checking product. This impact was years due to our balance sheet growth. felt in 2005 with a slowing growth in 6. We will continue to focus on the development of management and employee talent. People make the difference. checking accounts. We must find new and better ways to... -

Page 8

... big efforts to reduce their card interchange expenses through litigation with Visa or through technological changes in how customer card payments are processed. The debit card is now an integral part of the checking account and TCF has nearly $80 million of card revenues at stake. The success and... -

Page 9

... Cooper as CEO. Under Bill's leadership, TCF went from a near bankrupt savings and loan to one of the best-run banks in America. His unique skills, experience and personality have powered TCF to an 18 percent annualized return to stockholders over his 20-year tenure. I will always appreciate Bill... -

Page 10

... extended hours in both our supermarket and traditional branches, to ensure that our customers can do business when it's convenient for them. Even on most holiCampus banking is the cornerstone of TCF days, TCF customers know that personal service is available to open new accounts, make deposits and... -

Page 11

... 2005, TCF installed "Express Service", a userfriendly teller platform system designed to improve work production efficiencies and enhance the customer experience. program for our small business customers. TCF continues to expand its customer base by offering services like TCF Check Cashing , free... -

Page 12

... campus card checking account offered to students, faculty and staff of 11 participating colleges and universities. During 2005, TCF proudly added DePaul University (Illinois) and Milwaukee Area Technical College (Wisconsin) to its impressive list of schools. By organizing management teams to most... -

Page 13

...services such as data processing, bank operations, product development and marketing, finance, treasury services, employee benefits, legal, compliance, credit review, and internal audit. This structure gives locally managed banks the flexibility to share, compare and refine new products and services... -

Page 14

... Fees & Other Revenue millions of dollars 1 Branches opened since January 1, 2000. 2 Consisting of fees and services charges, card revenue, ATM revenue, and investments and insurance revenue. New Branch1 Total Deposits millions of dollars 1 Branches opened since January 1, 2000. Commercial lending... -

Page 15

...cost checking, savings, money market and certificate of deposit accounts). A principal strategy of TCF's Power Assets is to lend on a secured basis. Our strong credit quality is evidence that this important strategy is working; TCF has one of the lowest charge-off ratios in the banking industry. TCF... -

Page 16

...-dollar by TCF. • Employee's Fund - Funds contributed by employees through payroll deduction; contributions are matched 100 percent by the TCF Foundation. • TCF Foundation and Corporate Giving - Larger grants and multi-year commitments awarded to local and some national organizations. TCF Bank... -

Page 17

... Executive Officer; and Whereas , during that period and under his leadership TCF, which had limited financial capacity and prospects when he joined TCF in 1985, has become one of the best performing banks in the United States, with branches in Minnesota, Michigan, Illinois, Wisconsin, Colorado... -

Page 18

16 TCF Financial Corporation and Subsidiaries -

Page 19

....) 200 Lake Street East, Mail Code EX0-03-A, Wayzata, Minnesota 55391-1693 (Address and zip code of principal executive offices) Registrant's telephone number, including area code: 612-661-6500 Securities registered pursuant to Section 12(b) of the Act (all registered on the New York Stock Exchange... -

Page 20

... Item 10. Item 11. Item 12. Item 13. Item 14. Directors and Executive Officers of the Registrant Executive Compensation Security Ownership of Certain Beneficial Owners and Management Certain Relationships and Related Transactions Principal Accounting Fees and Services 74 74 74 74 74 Part IV Item 15... -

Page 21

... ("TCF" or the "Company") is a Delaware national financial holding company based in Wayzata, Minnesota. Its principal subsidiary, TCF Bank® , is headquartered in Minnesota and operates in Minnesota, Illinois, Michigan, Wisconsin, Colorado and Indiana. At December 31, 2005, TCF had total assets... -

Page 22

...rate. TCF's consumer lending activities primarily include home equity real estate secured loans. They also include loans secured by personal property and to a limited extent, unsecured personal loans. Consumer loans may be made on a revolving line of credit or fixed-term basis. Education Lending TCF... -

Page 23

... market areas through the offering of a broad selection of deposit instruments including consumer, small business and commercial demand deposit accounts, interest-bearing checking accounts, money market accounts, regular savings accounts, certificates of deposit and retirement savings plans. 2005... -

Page 24

... selling money market mutual funds and corporate and government securities. TCF competes for the origination of loans with commercial banks, mortgage bankers, mortgage brokers, consumer and commercial finance companies, credit unions, insurance companies and savings institutions. TCF also... -

Page 25

..., to make payments on TCF Financial's borrowings, or for its other cash needs. TCF Bank's ability to pay dividends is dependent on regulatory policies and regulatory capital requirements. The ability to pay such dividends in the future may be adversely affected by new legislation or regulations, or... -

Page 26

... all of TCF's deposits are Savings Association Insurance Fund ("SAIF") insured, but TCF also has deposits insured by the Bank Insurance Fund ("BIF"). The FDIC establishes deposit insurance rates to maintain a mandated designated reserve ratio of 1.25% ($1.25 against $100 of insured deposits). The... -

Page 27

... a wide array of Available Information TCF's website, www.tcfexpress.com, includes free access to Company news releases, investor presentations, conference calls to discuss quarterly financial results, TCF's Annual Report and periodic filings required by the Securities and Exchange Commission ("SEC... -

Page 28

.... Management continually reviews the adequacy and effectiveness of these policies, systems and procedures. As an integral part of the risk management process, management has established various committees consisting of senior executives and others within the Company. These committees closely monitor... -

Page 29

... types. Cash flow variances may cause minor day-to-day excesses over this guideline. A contingency funding plan is in place should certain liquidity triggers occur. Other Market Risks Other sources of market risk include the Company's investment in mortgage servicing rights and FHLB stock. Mortgage... -

Page 30

... result in higher numbers of closed accounts and increased account acquisition costs. TCF actively monitors customer behavior and adjusts policies and marketing efforts accordingly to attract new and retain existing checking account customers. New Branch Expansion Opening new branches is an integral... -

Page 31

..., results of operations, and financial condition. The financial services industry is extensively regulated. Federal and state laws and regulations are designed primarily to protect the deposit insurance funds and consumers, and not necessarily to benefit a financial company's shareholders. These... -

Page 32

...such activity, or other events outside of TCF's control, could have a material adverse impact either on the financial services industry as a whole, or on TCF's business, results of operations, and financial condition. Estimates and Assumptions TCF's consolidated financial for 139 of its bank branch... -

Page 33

... at the time, including TCF's earnings, financial condition and capital requirements, the cash available to pay such dividends (derived mainly from dividends and distributions from TCF Bank), as well as regulatory and contractual limitations and such other factors as the Board of Directors may deem... -

Page 34

....04% 375 1,249 Return on average assets Return on average equity Average total equity to average assets Net interest margin (1) Net charge-offs as a percentage of average loans and leases Common dividend payout ratio Number of: Banking locations Checking accounts (in thousands) N.M. Not Meaningful... -

Page 35

... banking; small business banking; consumer lending; leasing and equipment finance; and investments, securities brokerage and insurance services. The retail banking business includes traditional and supermarket branches, campus banking, Express Teller ATMs and Visa U.S.A. Inc. ("Visa") cards. TCF... -

Page 36

... or to local customers. TCF's largest core lending business is its consumer home equity loan operation, which offers fixed- and variable-rate loans and lines of credit secured by residential real estate properties. The leasing and equipment finance businesses consist of TCF Equipment Finance, Inc... -

Page 37

... mortgagebacked securities. Banking non-interest expense totaled $553.2 million, up 7.1% from $516.4 million in 2004. The increases were primarily due to compensation and benefits and occupancy costs associated with new branch expansion, increases in card processing and issuance expenses related to... -

Page 38

...during the years ended December 31, 2005 and 2004, respectively. (2) Average balance and yield of securities available for sale are based upon the historical amortized cost. (3) Substantially all leasing and equipment finance loans and leases have fixed rates. (4) Average balance of loans and leases... -

Page 39

... Small business Commercial and custodial Total non-interest bearing deposits Interest-bearing deposits: Premier checking Other checking Subtotal Premier savings Other savings Subtotal Money market Subtotal Certificates of deposit Total interest-bearing deposits Total deposits Borrowings Short-term... -

Page 40

...rate Commercial business: Fixed- and adjustable-rate Variable-rate Leasing and equipment finance Residential real estate Total loans and leases Total interest income Interest expense: Premier checking Other checking Premier savings Other savings Money market Certificates of deposit Borrowings: Short... -

Page 41

... offset by an adverse impact on deposit account balances and rates, as competition for checking, savings and money market deposits, important sources of lowercost funds for TCF, is intense. See "Consolidated Financial Condition Analysis - Deposits" and "Quantitative and Qualitative Disclosures about... -

Page 42

...Year Ended December 31, (Dollars in thousands) Fees and service charges Card revenue ATM revenue Investments and insurance revenue Subtotal Leasing and equipment finance Mortgage banking Other Fees and other revenue Gains on sales of securities available for sale Losses on termination of debt Total... -

Page 43

...,795 4,279 $12,042 (Dollars in thousands) Servicing income Less mortgage servicing: Amortization (Recovery) impairment Net servicing income (loss) Gains on sales of loans (1) Other income Total mortgage banking revenue (1) Beginning in 2005, TCF's mortgage banking business no longer originates or... -

Page 44

.... A key component in determining the fair value of mortgage servicing rights is the projected cash flows of the underlying loan portfolio. TCF uses projected cash flows and related prepayment assumptions based on management's best estimates. The prepayment rate on the third-party servicing portfolio... -

Page 45

...996 Compound Annual Growth Rate 1-Year 5-Year 2005/2004 2005/2000 .5% 5.6% 4.5 12.0 1.1 8.7 (2.5) (8.5) 12.1 4.1 - 4.1 6.4 6.8 6.0 .9 6.7 6.3 N.M. 6.0 Compensation and Employee Benefits Compensation and employee benefits, representing 53%, 55% and 54% of total noninterest expense in 2005, 2004 and... -

Page 46

... and normal payment and prepayment activity. At December 31, 2005, the increase in mortgage-backed securities partially offsets the declines in residential loans in the treasury services portfolio. TCF's securities available for sale portfolio included $1.6 billion and $5.3 million of fixed-rate and... -

Page 47

...: Lines of credit Closed-end loans Total consumer home equity Other Total consumer home equity and other Commercial real estate Commercial business Total commercial Leasing and equipment finance (1) Residential real estate Total loans and leases (1) Compound Annual Growth Rate 1-Year 5-Year 2005... -

Page 48

... loan amount (current outstanding balance on closed-end loans and the total commitment on lines of credit) plus deferred loan origination costs net of fees, plus the amount of senior liens, if any. Property values represent the most recent market value or property tax assessment value known to TCF... -

Page 49

... were secured by properties located in its primary markets. The following tables summarize TCF's leasing and equipment finance portfolio by marketing segment and by equipment type: At December 31, (Dollars in thousands) 2005 Over 30-Day Delinquency as Percent a Percentage of Total of Balance 58... -

Page 50

.... At December 31, 2005, TCF's residential real estate loan portfolio was comprised of $616.8 million of fixed-rate loans and $153.6 million of adjustable-rate loans. Loan and leases outstanding at December 31, 2005 are shown in the following table by maturity: Consumer Home Equity and Other $ 277... -

Page 51

... Consumer home equity and other Commercial real estate Commercial business Leasing and equipment finance Residential real estate Total recoveries Net charge-offs Provision charged to operations Acquired allowance Balance at end of year Key Indicators: Net charge-offs as a percentage of average loans... -

Page 52

...of Average Loans and Leases .08% .02 .04 .43 .01 .11% (Dollars in thousands) Consumer home equity and other Commercial real estate Commercial business Leasing and equipment finance (1) Residential real estate Total (1) For the year ended December 31, 2005, leasing and equipment finance net charge... -

Page 53

... 51,974 12,830 1,825 14,655 $66,629 .82% .59 (Dollars in thousands) Non-accrual loans and leases: Consumer home equity and other Commercial real estate Commercial business Leasing and equipment finance Residential real estate Total non-accrual loans and leases Other real estate owned: Residential... -

Page 54

...parent company only) include cash dividends from TCF's wholly owned bank subsidiary, issuance of equity securities and borrowings under a $105 million line of credit. TCF Bank's ability to pay dividends or make other capital distributions to TCF is restricted by regulation and may require regulatory... -

Page 55

... 2005/2004 (Dollars in thousands) 2005 2001 Number of new branches opened during the year: Traditional Supermarket Campus Total Number of new branches at year end: Traditional Supermarket Campus Total Percent of total branches Number of checking accounts Deposits: Checking Savings Money market... -

Page 56

... 5,103 - $263,937 After 5 Years $1,723,678 83,737 41,572 - $1,848,987 Commitments Commitments to lend: Consumer home equity and other Commercial Leasing and equipment finance Other Total commitments to lend Loans serviced with recourse Standby letters of credit and guarantees on industrial revenue... -

Page 57

... 21, 2005, TCF's Board of Directors and the University of Minnesota Board of Regents ratified contracts for TCF's sponsorship of a new on-campus football stadium to be called "TCF Bank Stadium" and an extension of TCF's sponsorship of the U Card. The U Card serves as a key for access to a variety... -

Page 58

... of 2004. Card revenues, included in banking fees and other revenue, totaled $21.4 million for the fourth quarter of 2005, up $3.8 million, or 21.6% over the same quarter in 2004. The increase was primarily due to increased customer transaction volumes and related fees. Leasing and equipment finance... -

Page 59

... operations; denial of insurance coverage for claims made by TCF; technological, computer-related or operational difficulties or loss or theft of information; adverse changes in securities markets; the risk that TCF could be unable to effectively manage the volatility of its mortgage servicing... -

Page 60

... on TCF's deposit account balances, if customers transfer some of their funds to higher interest rate deposit products or other investments, resulting in an increase in the total cost of funds for TCF. TCF estimates that an immediate 100 basis point decrease in current mortgage loan interest rates... -

Page 61

... 2005 and 2004, and the related consolidated statements of income, stockholders' equity, and cash flows for each of the years in the three-year period ended December 31, 2005. These consolidated financial statements are the responsibility of the Company's management. Our responsibility is to express... -

Page 62

... estate Total loans and leases Allowance for loan and lease losses Net loans and leases Premises and equipment Goodwill Mortgage servicing rights Other assets Total assets Liabilities and Stockholders' Equity Deposits: Checking Savings Money market Certificates of deposit Total deposits Short-term... -

Page 63

... service charges Card revenue ATM revenue Investments and insurance revenue Subtotal Leasing and equipment finance Mortgage banking Other Fees and other revenue Gains on sales of securities available for sale Losses on termination of debt Total non-interest income Non-interest expense: Compensation... -

Page 64

... Cancellation of shares for tax withholding Amortization of stock compensation Exercise of stock options, 66,064 shares Stock compensation tax benefits Change in shares held in trust for deferred compensation plans, at cost Balance, December 31, 2005 185,277,874 214,540) (36,624) - - - - 185,026... -

Page 65

...and equipment Sales of deposits, net of cash paid Other, net Net cash (used) provided by investing activities Cash flows from financing activities: Net increase (decrease) in deposits Net (decrease) increase in short-term borrowings Proceeds from long-term borrowings Payments on long-term borrowings... -

Page 66

...") is a Delaware national financial holding company engaged primarily in community banking and leasing and equipment finance through its wholly owned subsidiary, TCF Bank. TCF Bank owns leasing and equipment finance, mortgage banking, securities brokerage and investment and insurance sales, and Real... -

Page 67

... in the capitalized mortgage servicing rights and a charge to the related valuation allowance. Lease Financing TCF provides various types of lease financing that are classified for accounting purposes as either direct financing, sales-type, leveraged or operating leases. Leases that transfer... -

Page 68

... leases that have been funded on a non-recourse basis by third-party financial institutions, the related debt is also placed on non-accrual status. Interest payments received on non-accrual loans and leases are generally applied to principal unless the remaining principal balance has been determined... -

Page 69

... from the date of overdraft. Uncollectible deposit fees are reversed against fees and service charges. Note 2. Cash and Due from Banks At December 31, 2005, TCF was required by Federal Reserve Board regulations to maintain reserve balances of $77.7 million in cash on hand or at the Federal Reserve... -

Page 70

... related to TCF's borrowings from these banks. All new FHLB borrowing activity since 2000 is done with the FHLB of Des Moines. FHLBs Balance represents Federal Reserve Bank and Federal Home Loan Bank ("FHLB") stock, required regulatory investments. Note 4. Securities Available for Sale Securities... -

Page 71

... of business on normal credit terms, including interest rates and collateral, as those prevailing at the time for comparable transactions with unrelated persons. The aggregate amount of loans to executive officers of TCF was $115 thousand at December 31, 2005 and 2004. In the opinion of management... -

Page 72

... Balance, at year-end Interest income recognized on non-accrual loans and leases (cash basis) Contractual interest on non-accrual loans and leases (2) (1) (2) There were no impaired loans at December 31, 2005, 2004 and 2003 which did not have a related allowance for loan losses. Represents interest... -

Page 73

..., changes in mortgage interest rates, prepayment rates and other market conditions. (In thousands) Estimated Amortization Expense for the Year Ended December 31,: 2006 2007 2008 2009 2010 Mortgage Servicing Rights $7,917 6,249 5,096 4,298 3,624 Deposit Base Intangibles $1,630 956 - - - Total... -

Page 74

... loans, which are included in deposits in the Consolidated Statements of Financial Condition. These custodial deposits relate primarily to mortgage servicing operations and represent funds due to investors on mortgage loans serviced by TCF and customer funds held for real estate taxes and insurance... -

Page 75

... Home Loan Bank advances 150,000 Line of credit 16,500 Treasury, tax and loan note payable 6,525 Total $472,126 Year ended December 31, Average daily balance Federal funds purchased $308,062 Securities sold under repurchase agreements 518,953 Federal Home Loan Bank advances 68,630 Line of credit... -

Page 76

...agreement. The interest rate on the line of credit is based on either the prime rate or LIBOR. TCF has the option to select the interest rate index and term for advances on the line of credit. Note 12. Long-term Borrowings Long-term borrowings consist of the following: At December 31, 2005 (Dollars... -

Page 77

... the market rate on all of the fixed-rate callable advances and repurchase agreements. The next call year and stated maturity year for the callable advances and repurchase agreements outstanding at December 31, 2005 were as follows: (Dollars in thousands) Year 2006 2008 2009 2010 2011 2015 Total... -

Page 78

...Restricted stock and deferred compensation plans Allowance for loan and lease losses Securities available for sale Other Total deferred tax assets Deferred tax liabilities: Lease financing Loan fees and discounts Mortgage servicing rights Pension plan Premises and equipment Investments in FHLB Stock... -

Page 79

... 6.00 10.00 10.00 At December 31, 2005, TCF and TCF Bank exceeded their regulatory capital requirements and are considered "well-capitalized" under guidelines established by the FRB and the OCC pursuant to the Federal Deposit Insurance Corporation Improvement Act of 1991. Note 16. Incentive Stock... -

Page 80

... the account balance based on the five-year Treasury rate plus 25 basis points for 2005 and 2004 and based on the ten-year Treasury rate for 2003. Participants are fully vested after five years of qualifying service. In February 2006, TCF amended the Pension Plan to discontinue compensation credits... -

Page 81

... plan provisions for full-time and retired employees then eligible for these benefits were not changed. The Postretirement Plan is not funded. The following table sets forth the status of the Pension Plan and the Postretirement Plan at the dates indicated: Pension Plan Year Ended December 31, 2005... -

Page 82

... Year Ended December 31, 2005 2004 2003 6.0% 6.0% 6.5% N.A. N.A. N.A. N.A. N.A. N.A. The assets of TCF's pension plan assets are invested in passively managed index mutual funds that are designed to track the performance of the Standard and Poor's 500 and the Morgan Stanley Capital International... -

Page 83

... mortgage loans held for sale were carried at the lower of cost or market as adjusted for the effects of fair value hedges using (In thousands) Commitments to extend credit: Consumer home equity and other Commercial Leasing and equipment finance Other Total commitments to extend credit Loans... -

Page 84

...offered for loans with similar terms to borrowers with similar credit risk characteristics. Deposits The fair value of checking, savings and money market industrial revenue bonds are conditional commitments issued by TCF guaranteeing the performance of a customer to a third-party. These conditional... -

Page 85

... Closed-end loans and other Total consumer home equity and other Commercial real estate Commercial business Equipment finance loans Residential real estate Allowance for loan losses (1) Total financial instrument assets Financial instrument liabilities: Checking, savings and money market deposits... -

Page 86

... time periods...total of net income and other comprehensive income (loss), which for TCF is comprised entirely of unrealized gains and losses on investment securities available for sale. The following table summarizes the components of comprehensive income: Year Ended December 31, (In thousands) 2005... -

Page 87

...Total other expense Note 24. Business Segments Banking and leasing and equipment finance have been identified as reportable operating segments. Banking includes the following operating units that provide financial services to customers: deposits and investment products, commercial banking, consumer... -

Page 88

... totals. Beginning in 2005, TCF's mortgage banking business no longer originates or sells loans to the secondary market. As a result, mortgage banking is now included in the "other" category in the table below, in addition to TCF's parent company and corporate functions. Leasing and Equipment... -

Page 89

... expense Dividends from TCF Bank Other non-interest income: Affiliate service fees Other Total other non-interest income Non-interest expense: Compensation and employee benefits Occupancy and equipment Other Total non-interest expense Income before income tax benefit and equity in undistributed... -

Page 90

... actions as part of its lending and leasing collection activities. From time to time, borrowers and other customers, or employees or former employees, have also brought actions against TCF, in some cases claiming substantial amounts of damages. Financial services companies are subject to the risk... -

Page 91

... Financial Condition Data: Securities available for sale Residential real estate loans Subtotal Loans and leases excluding residential real estate loans Goodwill Mortgage servicing rights Total assets Checking, savings and money market deposits Certificates of deposit Total deposits Short-term... -

Page 92

... 31, 2005. KPMG LLP, TCF's registered public accounting firm that audited the consolidated financial statements included in this annual report, has issued an unqualified attestation report on management's assessment of the Company's internal control over financial reporting. Any control system, no... -

Page 93

... and the related consolidated statements of income, stockholders' equity, and cash flows for each of the years in the three-year period ended December 31, 2005, and our report dated February 16, 2006 expressed an unqualified opinion on those consolidated financial statements. Minneapolis, Minnesota... -

Page 94

... of Directors, Report of Compensation/Nominating/Corporate Governance Committee, Summary Compensation Table, Option Grants and Exercises and Benefits for Executives. Item 12. Security Ownership of Certain Beneï¬cial Owners and Management Information regarding ownership of TCF's common stock by TCF... -

Page 95

...' Equity for each of the years in the three-year period ended December 31, 2005 Consolidated Statements of Cash Flows for each of the years in the three-year period ended December 31, 2005 Notes to Consolidated Financial Statements Other Financial Data Management's Report on Internal Control... -

Page 96

... duly authorized. TCF Financial Corporation Registrant By /s/Lynn A. Nagorske Lynn A. Nagorske Chief Executive Officer and Director Dated: February 16, 2006 Pursuant to the requirements of the Securities Exchange Act of 1934, this report has been signed below by the following persons on behalf of... -

Page 97

... filed April 29, 2005] Form of TCF Financial Corporation Restricted Stock Agreement and Non-solicitation/Confidentiality Agreement Summary of Stock Award Program for Consumer Lending and Business Banker Divisions TCF Financial Corporation Executive Deferred Compensation Plan as amended and restated... -

Page 98

..., No. 001-10253]; Restated Trust Agreement as executed with First National Bank in Sioux Falls as trustee effective as of October 1, 2000 [incorporated by reference to Exhibit 10(d) of TCF Financial Corporation's Annual Report on Form 10-K for the fiscal year ended December 31, 2000, No. 001-10253... -

Page 99

... for the quarter ended March 31, 2004, No. 001-10253] and 2005 Management Incentive Plan - Executive [incorporated by reference to TCF Financial Corporation's Current Report on Form 8-K (filed January 27, 2005)] TCF Performance-Based Compensation Policy for Covered Executive Officers as amended and... -

Page 100

... to Exhibit 10(y) to TCF Financial Corporation's Annual Report on Form 10-K for the fiscal year ended December 31, 1995, No. 001-10253] Supplemental Employee Retirement Plan for TCF Cash Balance Pension Plan, as amended and restated through January 24, 2005 [incorporated by reference to Exhibit... -

Page 101

...TCF Investments and Insurance President and Chief Executive Officer Peter O. Torvik TCF Bank Illinois/Wisconsin/Indiana Chief Operating Officer James L. Koon Senior Vice Presidents Ronald L. Britz Beverly M. Craig Peter R. Daugherty Timothy J. Donnegan James T. Dowiak TCF Bank Colorado President... -

Page 102

...ï¬ces Executive Offices TCF Financial Corporation 200 Lake Street East Mail Code EX0-03-A Wayzata, MN 55391-1693 (612) 661-6500 Michigan Headquarters 401 East Liberty Street Ann Arbor, MI 48104 (734) 769-8300 Chairman of the Board Lynn A. Nagorske CPA/Managing Director, George Johnson & Company... -

Page 103

...access to investor information, news releases, investor presentations, access to TCF's quarterly conference calls, TCF's annual report,and SEC filings. Information may also be obtained, free of charge, from: TCF Financial Corporation Corporate Communications 200 Lake Street East EX0-02-C Wayzata, MN... -

Page 104

... TCF Financial Corporation: Long-term senior Short-term TCF Bank: Long-term deposits Short-term deposits Stock Price Performance (In Dollars) $35 Stock Price Dividends 30 $1.0 0.9 0.8 25 0.7 0.6 0.5 20 15 Stock Split 11/28/97 Stock Split 9/3/04 0.4 0.3 0.2 0.1 10 5 Year 6-86 12-86 Ending... -

Page 105

... open 12 hours a day, seven days a week, 364 days per year. TCF banks a large and diverse customer base. We provide customers innovative products through multiple banking channels, including traditional, supermarket and campus branches, TCF EXPRESS TELLER® and other ATMs, debit cards, phone banking... -

Page 106

TCF Financial Corporation 200 Lake Street East Wayzata, MN 55391-1693 www.tcfexpress.com 002CS-10279 TCFIR9332