Boeing 2006 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2006 Boeing annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

64 The Boeing Company and Subsidiaries

Notes to Consolidated Financial Statements

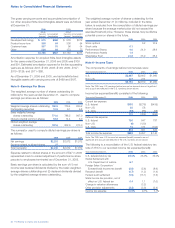

Amounts recognized in Accumulated other comprehensive loss

at December 31, 2006 are as follows:

Other

Postretirement

Pensions Benefits

At December 31, 2006 2006

Net actuarial loss (gain) $10,201 $2,494

Prior service cost (credit) 1,336 (568)

Total recognized in Accumulated

other comprehensive loss $11,537 $1,926

The estimated amount that will be amortized from Accumulated

other comprehensive loss into net periodic benefit cost in 2007

is as follows:

Other

Postretirement

Pensions Benefits

Year ending December 31, 2007 2007

Recognized net actuarial loss/(gain) $762 $159

Amortization of prior service costs 197 (88)

Total $959 $÷71

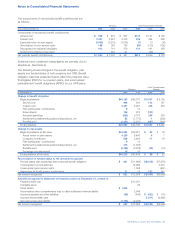

The accumulated benefit obligation (ABO) for all pension plans

was $41,706 and $40,999 at September 30, 2006 and 2005.

All of our major tax qualified pension plans, have plan assets

that exceed ABOs at September 30, 2006. The following table

shows the key information for all plans with ABO in excess of

plan assets:

At September 30, 2006 2005

Projected benefit obligation $1,602 $10,638

Accumulated benefit obligation 1,342 10,343

Fair value of plan assets 573 9,405

The Medicare Prescription Drug, Improvement and

Modernization Act of 2003 reduced our APBO by $156 at

September 30, 2005 and $439 at September 30, 2004. These

reductions/actuarial gains are amortized over the expected

average future service of current employees.

Assumptions

At September 30, 2006 2005 2004 2003

Discount rate:

pension and OPB 5.90%5.50%5.75%6.00%

Expected return on

plan assets 8.25%8.50%8.50%8.75%

Rate of compensation

increase 5.50%5.50%5.50%5.50%

In 2005, we modified our method of determining the discount

rate so that the discount rate for each individual pension plan

is determined separately based on the duration of each plan’s

liabilities. Previously, we determined a single discount rate for all

our postretirement benefit plans. We made the change mainly

because of the divergence in the populations of our various

plans due to employee transfers, layoffs and divestitures. The

new method continues to include a matching of the plans’

expected future benefit payments against a yield curve that’s

based on high quality, non-callable bonds in the Bloomberg

index as of the measurement date, omitting bonds with the

ten percent highest and the ten percent lowest yields. The dis-

closed rate is the average rate for all the plans, weighted by the

projected benefit obligation. As of September 30, 2006, the

weighted average was 5.9%, and the rates for individual plans

ranged from 5.00% to 6.00%. As of September 30, 2005, the

weighted average was 5.50%, and the rates for individual plans

ranged from 5.00% to 6.00%.

The pension fund’s expected return on assets assumption

is derived from an extensive study conducted by our Trust

Investments group and its actuaries on a periodic basis. The

study includes a review of actual historical returns achieved by

the pension trust and anticipated future long-term performance

of individual asset classes with consideration given to the

related investment strategy. While the study gives appropriate

consideration to recent trust performance and historical returns,

the assumption represents a long-term prospective return.

The expected return on plan assets determined on each

measurement date is used to calculate the net periodic benefit

cost/(income) for the upcoming plan year.

At September 30, 2006 2005

Assumed healthcare cost trend rates

Healthcare cost trend rate assumed next year 8.00%9.00%

Ultimate trend rate 5.00%5.00%

Year that trend reached ultimate rate 2013 2013

Assumed healthcare cost trend rates have a significant

effect on the amounts reported for the healthcare plans. To

determine the healthcare cost trend rates we look at a

combination of information including ongoing claims cost

monitoring, annual statistical analyses of claims data, reconcilia-

tion of forecast claims against actual claims, review of trend

assumptions of other plan sponsors and national health trends,

and adjustments for plan design changes, workforce changes,

and changes in plan participant behavior. A one-percentage-

point change in assumed healthcare cost trend rates would

have the following effect:

Increase Decrease

Effect on postretirement benefit obligation $683 $(653)

Effect on total of service and interest cost 58 (50)