Boeing 2006 Annual Report Download - page 40

Download and view the complete annual report

Please find page 40 of the 2006 Boeing annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

Cost estimates are based largely on negotiated and anticipated

contracts with suppliers, historical performance trends, and

business base and other economic projections. Factors that

influence these estimates include production rates, internal and

subcontractor performance trends, asset utilization, anticipated

labor agreements, and inflationary trends.

To ensure reliability in our estimates, we employ a rigorous esti-

mating process that is reviewed and updated on a quarterly basis.

Changes in estimates are recognized on a prospective basis.

Due to the significance of judgment in the estimation process

described above, it is likely that materially different cost of sales

amounts could be recorded if we used different assumptions,

or if the underlying circumstances were to change. Changes in

underlying assumptions/estimates, or circumstances may ad-

versely or positively affect financial performance in future periods.

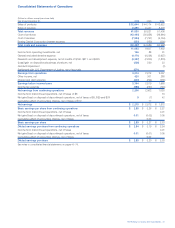

If combined cost of sales percentages for all commercial air-

plane programs for all of 2006 had been estimated to be higher

or lower by 1%, it would have increased or decreased pre-tax

income for 2006 by approximately $243 million.

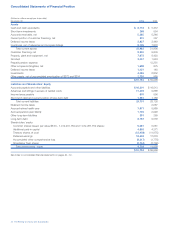

Aircraft Valuation

Used Aircraft Under Trade-in Commitments The fair value of

trade-in aircraft is determined using aircraft specific data such

as, model, age and condition, market conditions for specific air-

craft and similar models, and multiple valuation sources. Trade-

in aircraft valuation varies significantly depending on which

market we determine is most likely for each aircraft. This process

begins years before the return of the aircraft. On a quarterly

basis, we update our valuation analysis based on the actual

activities associated with placing each aircraft into a market.

Based on the best market information available at the time, it is

probable that we would be obligated to perform on trade-in

commitments with net amounts payable to customers totaling

$19 million and $72 million at December 31, 2006 and 2005.

Accounts payable and other liabilities included $22 million at

December 31, 2005, which represents the exposure related to

these trade-in commitments.

Had the estimate of trade-in value used to calculate our obliga-

tion related to probable trade-in commitments been 10% lower

than our actual assessment, using a measurement date of

December 31, 2006, Accounts payable and other liabilities

would have increased by approximately $2 million. We continu-

ally update our assessment of the likelihood of our trade-in air-

craft purchase commitments and continue to monitor all these

commitments for adverse developments.

Impairment Review for Assets Under Operating Leases and Held

for Sale or Re-lease When events or circumstances indicate, we

evaluate assets under operating lease or held for re-lease for

impairment utilizing an expected undiscounted cash flow

analysis. We use various assumptions when determining the

expected undiscounted cash flow including our intention to hold

or dispose of an asset before the end of its economic useful

life, the expected future lease rates, lease terms, residual value

of the aircraft or equipment, periods in which the asset may be

held in preparation for a follow-on lease, maintenance costs,

remarketing costs and the remaining economic life of the asset.

When we determine that impairment is indicated for an asset,

the amount of asset impairment expense recorded is the

excess of the carrying value over the fair value of the asset.

Had future lease rates on these assets we evaluate for

impairment been 10% lower, we estimate that no additional

impairment expense would have been recognized as of

December 31, 2006. We are unable to predict the likelihood

of any future impairments.

Used aircraft acquired by the Commercial Airplanes segment

are included in Inventories at the lower of cost or market as it

is our intent to sell these assets. To mitigate costs and en-

hance marketability, aircraft may be placed on operating lease.

While on operating lease, the assets are included in “Customer

financing,” however, the valuation continues to be based on

the lower of cost or market.

Allowance for Losses on Receivables The allowance for losses

on receivables (valuation provision) is used to provide for poten-

tial impairment of receivables on the Consolidated Statements

of Financial Position. The balance represents an estimate of

reasonably possible and probable but unconfirmed losses in the

receivables portfolio. The estimate is based on various qualita-

tive and quantitative factors, including historical loss experience,

collateral values, and results of individual credit reviews. Factors

considered in assessing collectibility include, but are not limited

to, a customer’s extended delinquency, requests for restructur-

ing and filings for bankruptcy. The adequacy of the allowance is

assessed quarterly. There can be no assurance that actual

results will not differ from estimates or that the consideration of

these factors in the future will not result in an increase or

decrease to the allowance for losses on receivables.

Had the applicable cumulative default rate been changed by

plus or minus 15%, excluding impaired customers for which the

default rate is maintained at 100%, we estimate that the

allowance would have been higher or lower by approximately

$34 million.

Lease Residual Values Equipment under operating leases is

carried at cost less accumulated depreciation and is depreci-

ated to estimated residual value using the straight-line method

over the lease term or projected economic life of the asset.

Estimates used in determining residual values significantly

impact the amount and timing of depreciation expense for

equipment under operating leases. For example, a change in

the estimated residual values of 1% as of December 31, 2006

could result in a cumulative pre-tax earnings impact of $20 mil-

lion to be recognized over time.

38 The Boeing Company and Subsidiaries

Management’s Discussion and Analysis