Boeing 2006 Annual Report Download - page 51

Download and view the complete annual report

Please find page 51 of the 2006 Boeing annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

|

|

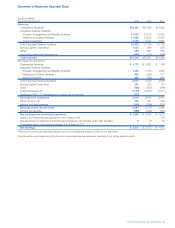

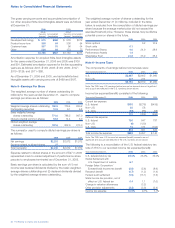

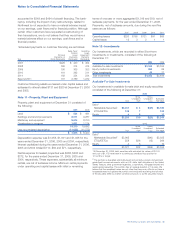

The Boeing Company and Subsidiaries 49

Notes to Consolidated Financial Statements

Effective December 31, 2006, we adopted SFAS No.158,

Employers’ Accounting for Defined Benefit Pension and Other

Postretirement Plans – an amendment of FASB Statements

No. 87, 88, 106 and 132(R) (SFAS No. 158) which requires that

the Consolidated Statements of Financial Position reflect the

funded status of the pension and postretirement plans. In future

reporting periods, the difference between actual amounts and

estimates based on actuarial assumptions will be recognized in

Other comprehensive loss in the period in which they occur.

Postemployment Plans

We record a liability for postemployment benefits, such as

severance or job training, when payment is probable, the

amount is reasonably estimable, and the obligation relates to

rights that have vested or accumulated.

Environmental Remediation

We are subject to federal and state requirements for protection

of the environment, including those for discharge of hazardous

materials and remediation of contaminated sites. We routinely

assess, based on in-depth studies, expert analyses and legal

reviews, our contingencies, obligations and commitments for

remediation of contaminated sites, including assessments of

ranges and probabilities of recoveries from other responsible

parties who have and have not agreed to a settlement and of

recoveries from insurance carriers. Our policy is to immediately

accrue and charge to current expense identified exposures

related to environmental remediation sites based on our best

estimate within a range of potential exposure for investigation,

cleanup and monitoring costs to be incurred.

Cash and Cash Equivalents

Cash and cash equivalents consist of highly liquid instruments,

such as certificates of deposit, time deposits, and other money

market instruments, which have original maturities of less than

three months. We aggregate our cash balances by bank, and

reclassify any negative balances to a liability account presented

as a component of Accounts payable and other liabilities.

Inventories

Inventoried costs on commercial aircraft programs and long-

term contracts include direct engineering, production and

tooling costs, and applicable overhead, which includes fringe

benefits, production related indirect and plant management

salaries and plant services, not in excess of estimated net

realizable value. To the extent a material amount of such costs

are related to an abnormal event or are fixed costs not appro-

priately attributable to our programs or contracts, they will be

expensed in the current period rather than inventoried. In

accordance with industry practice, inventoried costs include

amounts relating to programs and contracts with long production

cycles, a portion of which is not expected to be realized within

one year. Included in inventory for federal government contracts

is an allocation of allowable costs related to manufacturing

process re-engineering. We net advances and progress billings

on long-term contracts against costs incurred to date for each

contract in the Consolidated statements of financial position.

Contracts where costs incurred to date exceed advances and

progress billings are reported in Inventories, net of advances

and progress billings. Contracts where advances and progress

billings exceed costs incurred to date are reported in Advances

and billings in excess of related costs.

Because of the higher unit production costs experienced at the

beginning of a new or derivative commercial airplane program

(known as the learning curve effect), the actual costs incurred

for production of the early units in the program may exceed the

amount reported as cost of sales for those units. In addition,

the use of a total program gross profit rate to delivered units

may result in costs assigned to delivered units in a reporting

period being less than the actual cost of those units. The excess

actual costs incurred over the amount reported as cost of sales

is disclosed as deferred production costs, which are included in

inventory along with unamortized tooling costs.

The determination of net realizable value of long-term contract

costs is based upon quarterly contract reviews that determine

an estimate of costs to be incurred to complete all contract

requirements. When actual contract costs and the estimate to

complete exceed total estimated contract revenues, a loss

provision is recorded. The determination of net realizable value

of commercial aircraft program costs is based upon quarterly

program reviews that determine an estimate of revenue and

cost to be incurred to complete the program accounting quantity.

When estimated costs to complete exceed estimated program

revenues to go, a loss provision is recorded.

Used aircraft purchased by the Commercial Airplanes segment

and general stock materials are stated at cost not in excess of

net realizable value. See “Aircraft valuation” within this Note for

our valuation of used aircraft purchased by the Commercial

Airplanes segment. Spare parts inventory is stated at lower of

average unit cost or market. We review our commercial spare

parts and general stock materials each quarter to identify

impaired inventory, including excess or obsolete inventory,

based on historical sales trends, expected production usage,

and the size and age of the aircraft fleet using the part.

Impaired inventories are written-off as an expense to Cost of

products in the period the impairment occurs.

Included in inventory for commercial aircraft programs are

amounts paid or credited in cash, or other consideration to

certain airline customers, that are referred to as early issue

sales consideration. Early issue sales consideration is recognized

as a reduction to revenue when the delivery of the aircraft under

contract occurs. In the unlikely situation that an airline customer

was not able to perform and take delivery of the contracted

aircraft, we believe that we would have the ability to recover

amounts paid through retaining amounts secured by advances

received on aircraft to be delivered. However, to the extent

early issue sales consideration exceeds advances and is not

considered to be recoverable it would be recognized as a

current period expense.