Volvo 1999 Annual Report Download - page 85

Download and view the complete annual report

Please find page 85 of the 1999 Volvo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

|

|

83

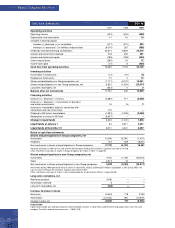

The costs for other benefits include the following components

1997 1998 1999

Benefits earned during the year 42 46 35

Interest expense 97 77 60

Reported insurance profits and losses (4) 12 (5)

Costs attributable to restructuring 1 – –

Net post retirement benefit expenses 136 135 90

Comprehensive income 1997 1998 1999

Net income in accordance with U.S. GAAP 6,556 9,432 31,690

Other comprehensive income, net of tax

Translation differences (367) 1,173 (1,389)

Unrealized gains on securities (SFAS 115):

Unrealized gains (losses) arising during the year 207 (186) (419)

Less: Reclassification adjustment for gains included in net income 1,295 (2,655) (43)

Adjustment for pensions and similar commitments

(minimum liability) 118 452 (54)

Other 212 (141) (8)

Other comprehensive income, subtotal 1,465 (1,357) (1,913)

Comprehensive income

in accordance with U.S. GAAP 8,021 8,075 29,777

An increase of one percentage point per year in health-

care costs would change the accumulated post retire-

ment benefit obligation as of December 31, 1998 by

approximately 189, and the net post-retirement benefit

expense by approximately 19. A decrease of 1% would

decrease the accumulated value of obligations by about

156 and reduce costs by approximately 18. In 1999, an

increase of 1% would increase the accumulated value of

obligations by about 65 and increase costs by about 6; a

decrease of 1% would reduce the accumulated value of

obligations by about 57 and cut costs by about 5.

Calculations made as of December 31, 1999 show an

annual increase of 8% in the weighted average per cap-

ita costs of covered health-care benefits; it is assumed

that the percentage will decline gradually to 5% in 2010

and then remain at that level.

The discount rate used in determining the accumulat-

ed post-retirement benefit obligation as of December 31,

1997, 1998 and 1999 was 7.0%, 6.75% and 7.5%

respectively.

J. Software development. Software development, used in

the Group’s operations, is conducted in Volvo IT. In Volvo’s

accounts, these expenditures are expensed as incurred.

In accordance with Statement of Position (SOP) 98–1

“Accounting for the Costs of Computer Software

Developed or Obtained for Internal Use” such expenditu-

res should be capitalized and amortized over the useful

lives of the projects. In Volvo’s accounting in accordance

with U.S. GAAP, SOP 98-1 is applied as of January 1999.

The new accounting principle should not be applied retro-

actively.

Supplementary U.S. GAAP information

Classification. In accordance with SFAS 95, “cash and

cash equivalents” comprise only funds with a maturity of

three months or less from the date of purchase. Some

of Volvo’s liquid funds (see Notes 19 and 20) do not

meet this requirement. Consequently, in accordance with

SFAS 95, changes in this portion of liquid funds should

be reported as investing activities.

Recent U.S. accounting pronouncement issued

but not yet adopted. In June 1998, the Financial

Accounting Standards Board issued SFAS No. 133,

“Accounting for Derivative Instruments and Hedging

Activities”, which establishes accounting and reporting

standards for derivative instruments, including certain

derivative instruments embedded in other contracts and

for hedging activities. This statement, as amended, is

effective for fiscal years beginning after June 15, 2000.

Volvo has not determined the impact SFAS No. 133 will

have on its consolidated financial statements.