Redbox 2008 Annual Report Download - page 69

Download and view the complete annual report

Please find page 69 of the 2008 Redbox annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

|

|

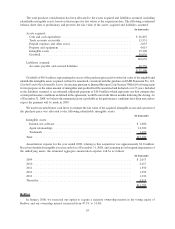

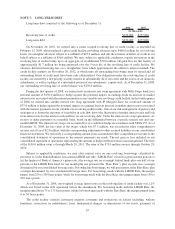

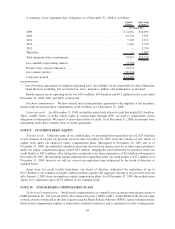

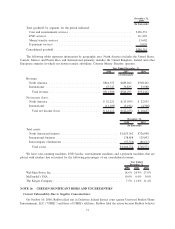

NOTE 7: LONG-TERM DEBT

Long-term debt consisted of the following as of December 31:

2008 2007

(In thousands)

Revolving line of credit ........................................ $270,000 $257,000

Long-term debt .............................................. $270,000 $257,000

On November 20, 2007, we entered into a senior secured revolving line of credit facility, as amended on

February 12, 2009, which replaced a prior credit facility, providing advances up to $400.0 million for (i) revolving

loans, (ii) swingline advances subject to a sublimit of $25.0 million, and (iii) the issuance of letters of credit in our

behalf subject to a sublimit of $50.0 million. We may, subject to applicable conditions, request an increase in the

revolving line of credit facility up to an aggregate of an additional $50.0 million. Original fees for this facility of

approximately $1.7 million are being amortized over the 5-year life of the revolving line of credit facility. We

amortize deferred financing fees on a straight-line basis which approximates the effective interest method. The

credit facility matures on November 20, 2012, at which time all outstanding borrowings must be repaid and all

outstanding letters of credit must have been cash collateralized. Our obligations under the revolving line of credit

facility are secured by a first priority security interest in substantially all of our assets and the assets of our domestic

subsidiaries, as well as a pledge of a substantial portion of our subsidiaries’ capital stock. As of December 31, 2008,

our outstanding revolving line of credit balance was $270.0 million.

During the first quarter of 2008, we entered into an interest rate swap agreement with Wells Fargo bank for a

notional amount of $150.0 million to hedge against the potential impact on earnings from an increase in market

interest rates associated with the interest payments on our variable-rate revolving credit facility. In the fourth quarter

of 2008 we entered into another interest rate swap agreement with JP Morgan Chase for a notional amount of

$75.0 million to hedge against the potential impact on earnings from an increase in market interest rates associated

with the interest payments on our variable-rate revolving credit facility. One of our risk management objectives and

strategies is to lessen the exposure of variability in cash flow due to the fluctuation of market interest rates and lock

in an interest rate for the interest cash outflows on our revolving debt. Under the interest rate swap agreements, we

receive or make payments on a monthly basis, based on the differential between a specific interest rate and one-

month LIBOR. The interest rate swaps are accounted for as a cash flow hedge in accordance with SFAS 133. As of

December 31, 2008, the fair value of the swaps, which was $7.5 million, was recorded in other comprehensive

income, net of tax of $2.9 million, with the corresponding adjustment to other accrued liabilities in our consolidated

financial statements. We reclassify a corresponding amount from accumulated other comprehensive income to the

consolidated statement of operations as the interest payments are made. The net gain or loss included in our

consolidated statement of operations representing the amount of hedge ineffectiveness is inconsequential. The term

of the $150.0 million swap is through March 20, 2011. The term of the $75.0 million swap is through October 28,

2010.

Subject to applicable conditions, we may elect interest rates on our revolving borrowings calculated by

reference to (i) the British Bankers Association LIBOR rate (the “LIBOR Rate”) fixed for given interest periods or

(ii) the highest of Bank of America’s prime rate, (the average rate on overnight federal funds plus one half of one

percent, or the LIBOR Rate fixed for one month plus one percent) (the “Base Rate”), plus, in each case, a margin

determined by our consolidated leverage ratio. For swing line borrowings, we will pay interest at the Base Rate, plus

a margin determined by our consolidated leverage ratio. For borrowings made with the LIBOR Rate, the margin

ranges from 250 to 350 basis points, while for borrowings made with the Base Rate, the margin ranges from 150 to

250 basis points.

As of December 31, 2008, our weighted average interest rate on the revolving line of credit facility was 2.2%

which was based on the debt agreement before the amendment. For borrowing made with the LIBOR Rate, the

margin ranged from 75 to 175 basis points, while for borrowings made with the Base Rate, the margin ranged from

0 to 50 basis points.

The credit facility contains customary negative covenants and restrictions on actions including, without

limitation, restrictions on indebtedness, liens, fundamental changes or dispositions of our assets, payments of

67