Metro PCS 2011 Annual Report Download - page 126

Download and view the complete annual report

Please find page 126 of the 2011 Metro PCS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

MetroPCS Communications, Inc. and Subsidiaries

Notes to Consolidated Financial Statements

December 31, 2011, 2010 and 2009

F-20

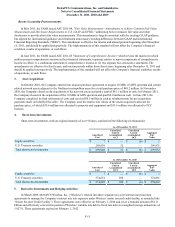

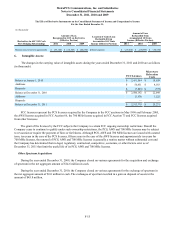

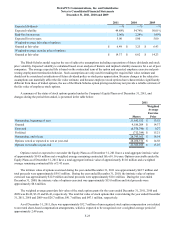

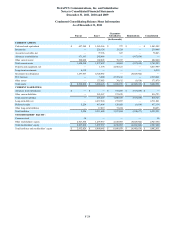

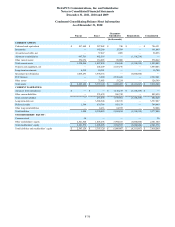

The following table summarizes the changes in fair value of the Company’s net derivative liabilities included in Level 2

assets (in thousands):

Fair Value Measurements of Net Derivative Liabilities Using Level 2 Inputs Net Derivative Liabilities

2011 2010

Beginning balance $ 8,309 $ 24,859

Total losses (realized or unrealized):

Included in earnings (1) 23,414 28,696

Included in accumulated other comprehensive loss (36,120)(12,146)

Transfers in and/or out of Level 2 — —

Purchases, sales, issuances and settlements — —

Ending balance $ 21,015 $ 8,309

————————————

(1) Losses included in earnings that are attributable to the reclassification of the effective portion of those derivative liabilities still held at the reporting

date as reported in interest expense in the consolidated statements of income and comprehensive income.

The following table summarizes the changes in fair value of the Company’s Level 3 assets (in thousands):

Fair Value Measurements of Assets Using Level 3 Inputs Long-Term Investments

2011 2010

Beginning balance $ 6,319 $ 6,319

Total losses (realized or unrealized):

Included in earnings — —

Included in accumulated other comprehensive income (loss) — —

Transfers in and/or out of Level 3 — —

Purchases, sales, issuances and settlements — —

Ending balance $ 6,319 $ 6,319

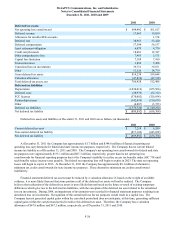

The carrying value of the Company’s financial instruments, with the exception of long-term debt including current

maturities, reasonably approximate the related fair values as of December 31, 2011 and 2010. The fair value of the Company’s

long-term debt, excluding capital lease obligations, is estimated based on the quoted market prices for the same or similar

issues or on the current rates offered to the Company for debt of the same remaining maturities. As of December 31, 2011, the

carrying value and fair value of long-term debt, including current maturities, were $4.5 billion and approximately $4.4 billion,

respectively. As of December 31, 2010, the carrying value and fair value of long-term debt, including current maturities, were

$3.5 billion and $3.5 billion, respectively.

Although the Company has determined the estimated fair value amounts using available market information and

commonly accepted valuation methodologies, considerable judgment is required in interpreting market data to develop fair

value estimates. The fair value estimates are based on information available at December 31, 2011 and 2010 and have not been

revalued since those dates. As such, the Company’s estimates are not necessarily indicative of the amount that the Company, or

holders of the instruments, could realize in a current market exchange and current estimates of fair value could differ

significantly.

10. Concentrations:

The Company purchases a substantial portion of its wireless infrastructure equipment and handset equipment from only a

few major suppliers. Further, the Company generally relies on one or two key vendors in each of the following areas: network

infrastructure equipment, billing services, payment services, customer care, handset logistics, roaming services and long

distance services. Loss of any of these suppliers could adversely affect operations temporarily until a comparable substitute

could be found.

Local and long distance telephone and other companies provide certain communication services to the Company.

Disruption of these services could adversely affect operations in the short term until an alternative telecommunication provider

was found.