Lexmark 2009 Annual Report Download - page 87

Download and view the complete annual report

Please find page 87 of the 2009 Lexmark annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

the Level 3 reconciliation which may be presented on a net or a gross basis. The ASU also makes clear the

appropriate level of disaggregation for fair value disclosures, which is generally by class of assets and

liabilities, as well as clarifies the requirement to provide disclosures about valuation techniques and inputs

for both recurring and nonrecurring fair value measurements that fall under Level 2 or Level 3. The new

disclosure requirements will be effective for the Company in the first quarter of 2010 with the exception of

the requirement to separately disclose purchases, sales, issuances, and settlements which will be

effective in the first quarter of 2011. The Company will incorporate the required disclosures into its

first quarter 2010 fair value footnote but has not yet decided whether or not it will early adopt the 2011

requirements as permitted under the guidance.

The FASB and SEC issued several accounting standards updates and staff accounting bulletins not

discussed above that related to technical corrections of existing guidance or new guidance that is not

meaningful to the Company’s current financial statements.

Reclassifications:

Certain prior year amounts have been reclassified, if applicable, to conform to the current presentation.

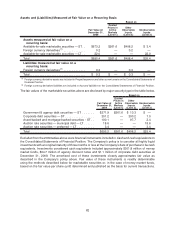

3. FAIR VALUE

General

Effective January 1, 2008 the Company adopted the authoritative guidance for fair value measurements

issued by the Financial Accounting Standards Board (“FASB”). This guidance defines fair value,

establishes a framework for measuring fair value in generally accepted accounting principles (“GAAP”)

and expands disclosures about fair value measurements. The guidance defines fair value as the price that

would be received to sell an asset or paid to transfer a liability in an orderly transaction between market

participants at the measurement date. As part of the framework for measuring fair value, the guidance

establishes a hierarchy of inputs to valuation techniques used in measuring fair value that maximizes the

use of observable inputs and minimizes the use of unobservable inputs by requiring that the most

observable inputs be used when available.

The guidance issued by the FASB in April 2009 for determining fair value when the volume and level of

activity for the asset or liability have significantly decreased and identifying transactions that are not orderly

was considered in preparation of the December 31, 2009 financial statements. The additional disclosures

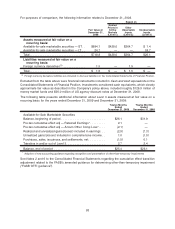

required by this guidance have been provided below, namely the disaggregation of fair value information to

the level of major security types used in Note 6 to the Consolidated Financial Statements. The guidance

does not require such disclosures for earlier periods presented for comparative purposes at initial

adoption.

See Note 2 to the Consolidated Financial Statements for information regarding the guidance issued by the

FASB in 2009 discussed above.

Fair Value Hierarchy

The three levels of the fair value hierarchy are:

• Level 1 — Quoted prices (unadjusted) in active markets for identical, unrestricted assets or

liabilities that the Company has the ability to access at the measurement date;

• Level 2 — Inputs other than quoted prices included in Level 1 that are observable for the asset or

liability, either directly or indirectly; and

• Level 3 — Unobservable inputs used in valuations in which there is little market activity for the asset

or liability at the measurement date.

Fair value measurements of assets and liabilities are assigned a level within the fair value hierarchy based

on the lowest level of any input that is significant to the fair value measurement in its entirety.

81