Lexmark 2009 Annual Report Download - page 56

Download and view the complete annual report

Please find page 56 of the 2009 Lexmark annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

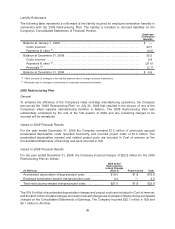

2007. Of the $17.8 million of 2006 project costs incurred, $11.1 million is included in Cost of revenue and

$6.7 million in Selling, general and administrative on the Company’s Consolidated Statements of Earnings.

For the year ended December 31, 2007, the Company incurred total pre-tax 2006 project costs of

$5.7 million in PSSD and $14.8 million in All other, while ISD realized a $2.7 million net benefit after the sale

of the Rosyth, Scotland facility.

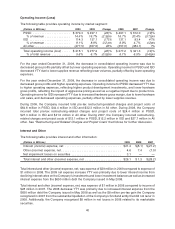

Liability Rollforward

As of December 31, 2009, the Company had a liability balance of $1.2 million related to contract

termination and lease charges in connection with the 2006 actions. Of the total $1.2 million

restructuring liability, $0.5 million is included in Accrued liabilities and $0.7 million is included in Other

liabilities on the Company’s Consolidated Statements of Financial Position.

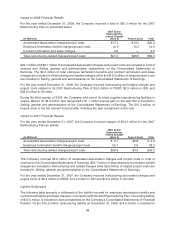

PENSION AND OTHER POSTRETIREMENT PLANS

The following table provides the total pre-tax cost related to Lexmark’s pension and other postretirement

plans for the years 2009, 2008 and 2007. Cost amounts are included as an addition to the Company’s cost

and expense amounts in the Consolidated Statements of Earnings.

(Dollars in Millions) 2009 2008 2007

Total cost of pension and other postretirement plans . . . . . . . . . . . . . . . . . $41.2 $37.0 $40.2

Comprised of:

Defined benefit pension plans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $20.3 $11.4 $13.2

Defined contribution plans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21.4 25.1 25.8

Other postretirement plans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (0.5) 0.5 1.2

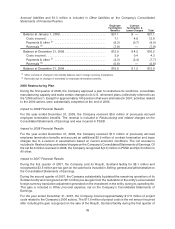

The increase in the cost of the defined benefit pension plans in 2009 compared to 2008 was primarily due

to curtailment losses recognized on restructuring related activity in the U.S. The decrease in the cost of

defined contribution plans in 2009 compared to 2008 was mainly due to a reduction in the number of

participants in the U.S. plan. Changes in actuarial assumptions did not have a significant impact on the

Company’s results of operations in 2008 and 2009, nor are they expected to have a material effect in 2010.

Future effects of retirement-related benefits on the operating results of the Company depend on economic

conditions, employee demographics, mortality rates and investment performance. Refer to Part II, Item 8,

Note 15 of the Notes to Consolidated Financial Statements for additional information relating to the

Company’s pension and other postretirement plans.

In 2008, there was a significant decline in the value of pension plan assets primarily resulting from a large

decline in equity markets. Because the Company defers current year differences between actual and

expected asset returns on equity investments over the subsequent five years in accordance with

prescribed accounting guidelines, the impact to 2009 pension expense was only $5 million.

The Pension Protection Act of 2006 (“the Act”) was enacted on August 17, 2006. Most of its provisions

became effective in 2008. The Act significantly changed the funding requirements for single-employer

defined benefit pension plans. The funding requirements are now largely based on a plan’s calculated

funded status, with faster amortization of any shortfalls. The Act directs the U.S. Treasury Department to

develop a new yield curve to discount pension obligations for determining the funded status of a plan when

calculating the funding requirements. The provisions of the Act resulted in the need for additional funding in

2009 of $73 million in the first quarter in the U.S.

50