Lexmark 2009 Annual Report Download - page 83

Download and view the complete annual report

Please find page 83 of the 2009 Lexmark annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

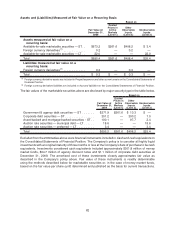

technique or multiple valuation techniques. In addition to the accounting guidance, the FSP also amends

fair value disclosure requirements to require in interim periods the disclosure of the inputs and valuation

techniques used to measure fair value and any changes in inputs and techniques during the period. The

FSP also requires that the fair value disclosures be presented for debt and equity securities by major

security type, based on the nature and risks of the security. FSP FAS 157-4 was first effective for the

Company’s second quarter 2009 financial statements and was applied prospectively. The FSP has not had

a significant impact on the valuation of the Company’s assets or liabilities. Refer to Note 3 to the

Consolidated Financial Statements for a discussion of the Company’s valuation techniques as well as

additional measures taken with respect to prices in response to the FSP.

In April 2009, the FASB issued FSP No. FAS 115-2 and FAS 124-2, Recognition and Presentation of

Other-Than-Temporary Impairments (“FSP FAS 115-2 and FAS 124-2”). This FSP amends the existing

guidance regarding the recognition of other-than-temporary impairment (“OTTI”) for debt securities. If the

fair value of a debt security is less than its amortized cost basis, an entity must assess whether the

impairment is other than temporary. If an entity intends to sell or it is more likely than not the entity will be

required to sell the debt security before its anticipated recovery of its amortized cost basis, an other-than

temporary impairment shall be considered to have occurred and the entire difference between the

amortized cost basis and the fair value must be recognized in earnings. If the entity does not expect

to sell the debt security, but the present value of cash flows expected to be collected is less than the

amortized cost basis, a credit loss is deemed to exist and OTTI shall be considered to have occurred.

However, in this case, the OTTI is separated into two components, the amount representing the credit loss

which is recognized in earnings and the amount related to all other factors which is now recognized in other

comprehensive income under the new guidance. In either case, for debt securities in which OTTI was

recognized in earnings, the difference between the new amortized cost basis (previous amortized cost

basis less OTTI recognized in earnings) and the cash flows expected to be collected shall be accreted in

accordance with existing guidance as interest income in subsequent periods. The FSP also changes the

presentation and disclosure requirements of other-than-temporary impairments on debt and equity

securities. In periods in which OTTI is determined, the total OTTI shall be presented in the statement

of earnings as well as the offset for the amount that was recognized in other comprehensive income under

the new FSP. Amounts recognized in accumulated other comprehensive income for which a portion of an

OTTI has been recognized in earnings must also be presented separately. The FSP also expands interim

and annual disclosure requirements for debt and equity securities including but not limited to the

methodology and significant inputs used to measure the credit loss portion of OTTI as well as a

tabular rollforward of the amount of credit losses recognized in earnings. The FSP became effective

for the Company’s new and existing investments as of April 1, 2009. The Company recognized a favorable

$2.1 million cumulative effect adjustment to the opening balance of retained earnings and a corresponding

adjustment to accumulated other comprehensive income, before consideration of tax effects, related to the

initial application of the FSP to its debt securities held by the Company at April 1, 2009 for which OTTI had

been previously recognized. This adjustment was calculated by comparing the present value of the cash

flows expected to be collected to the amortized cost bases of the debt securities at the transition date.

Under the new guidance, the Company has recognized in earnings net impairment losses of $3.1 million.

See Note 6 to the Consolidated Financial Statements for further details.

In May 2009, the FASB issued FAS No. 165, Subsequent Events (“FAS 165”). FAS 165 provides

accounting guidance and disclosure requirements for events that occur after the balance sheet date

but before financial statements are issued or available to be issued. FAS 165 should be applied to the

accounting for and disclosure of subsequent events not addressed in other GAAP and is not expected to

change current accounting practices. The standard requires that the effects of all subsequent events that

provide additional evidence about conditions that existed at the balance sheet date be recognized in the

financial statements. However, an entity shall not recognize subsequent events that provide evidence

about conditions that did not exist at the date of the balance sheet. For nonrecognized subsequent events,

the nature of the event and an estimate of the financial effects, or statement that such an estimate cannot

be made, should be disclosed if necessary to keep the financial statements from being misleading.

FAS 165 also requires that an entity disclose the date through which subsequent events have been

77