Kraft 2012 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2012 Kraft annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

|

|

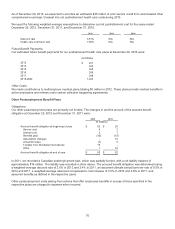

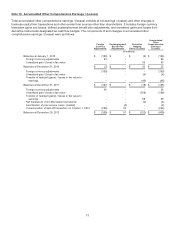

The fair values of our derivative instruments at December 31, 2011 were determined using:

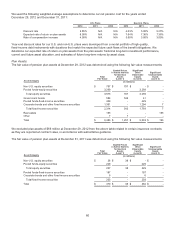

Total

Fair Value of Net

Asset / (Liability)

Quoted Prices in

Active Markets

for Identical

Assets

(Level 1)

Significant

Other Observable

Inputs

(Level 2)

Significant

Unobservable

Inputs

(Level 3)

(in millions)

Commodity contracts $ (11) $ (4) $ (7) $ -

Foreign exchange contracts 3 - 3 -

Interest rate contracts (25) - (25) -

Total derivatives $ (33) $ (4) $ (29) $ -

Level 2 financial assets and liabilities consist of commodity forwards and options; foreign exchange forwards, currency

swaps, and options; and interest rate swaps. Commodity derivatives are valued using an income approach based on the

observable market commodity index prices less the contract rate multiplied by the notional amount or based on pricing

models which rely on market observable inputs such as commodity prices. Foreign currency contracts are valued using an

income approach based on observable market forward rates less the contract rate multiplied by the notional amount. Our

calculation of the fair value of interest rate swaps is derived from a discounted cash flow analysis based on the terms of

the contract and the observable market interest rate curve. Our calculation of the fair value of financial instruments takes

into consideration the risk of nonperformance, including counterparty credit risk.

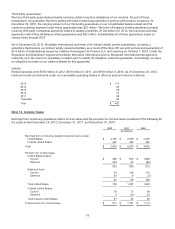

Derivative Volume:

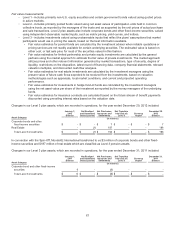

The net notional values of our derivative instruments as of December 29, 2012 and December 31, 2011 were:

2012 2011

(in millions)

Commodity contracts $ 518 $ 891

Foreign exchange contracts 947 59

Interest rate contracts - 1,000

Cash Flow Hedges:

Cash flow hedge activity, net of income taxes, within accumulated other comprehensive earnings / (losses) included:

2012 2011 2010

(in millions)

Accumulated other comprehensive earnings / (losses) at

beginning of period $ (18) $ 32 $ (3)

Unrealized gain / (loss) in fair value (199) (4) 35

Transfer of realized (gains) / losses in fair value to earnings 69 (46) -

Transfer from Mondele¯ z International (4) - -

Accumulated other comprehensive earnings / (losses) at end

of period $ (152) $ (18) $ 32

The unrealized gains / (losses), net of income taxes, recognized in other comprehensive income / (loss) were:

2012 2011 2010

(in millions)

Commodity contracts $ (57) $ 16 $ 37

Foreign exchange contracts (5) (4) (2)

Interest rate contracts (137) (16) -

Total $ (199) $ (4) $ 35

In connection with the $6.0 billion of senior unsecured notes we issued on June 4, 2012, we entered into an interest rate

swap. We recorded the loss related to that interest rate contract in accumulated other comprehensive earnings / (losses).

We expect to transfer these losses into earnings over the life of the related debt.

72