Kraft 2012 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2012 Kraft annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

|

|

Item 7A. Quantitative and Qualitative Disclosures about Market Risk.

As we operate primarily in North America but source our commodities on global markets and periodically enter into

financing or other arrangements abroad, we use financial instruments to manage our primary market risk exposures, which

are commodity price, foreign currency exchange rate, and interest rate risks. We monitor and manage these exposures as

part of our overall risk management program. Our risk management program focuses on the unpredictability of financial

markets and seeks to reduce the potentially adverse effects that the volatility of these markets may have on our operating

results. We maintain commodity price, foreign currency, and interest rate risk management policies that principally use

derivative instruments to reduce significant, unanticipated earnings fluctuations that may arise from volatility in commodity

prices, foreign currency exchange rates, and interest rates. We also sell commodity futures to unprice future purchase

commitments, and we occasionally use related futures to cross-hedge a commodity exposure. We are not a party to

leveraged derivatives and, by policy, do not use financial instruments for speculative purposes. Refer to Note 1, Summary

of Significant Accounting Policies, and Note 11, Financial Instruments, to the consolidated financial statements for further

details of our commodity price, foreign currency, and interest rate risk management policies and the types of derivative

instruments we use to hedge those exposures.

Value at Risk:

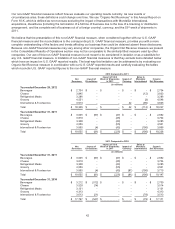

We use a value at risk (“VAR”) computation to estimate: 1) the potential one-day loss in pre-tax earnings of our commodity

price and foreign currency-sensitive derivative financial instruments; and 2) the potential one-day loss in the fair value of

our interest rate-sensitive financial instruments. We included our debt, commodity futures, forwards and options, foreign

currency forwards and interest rate swaps in our VAR computation. Excluded from the computation were anticipated

transactions and foreign currency trade payables and receivables which the financial instruments are intended to hedge.

We made the VAR estimates assuming normal market conditions, using a 95% confidence interval. We used a “variance /

co-variance” model to determine the observed interrelationships between movements in interest rates and various

currencies. These interrelationships were determined by observing interest rate and forward currency rate movements

over the prior quarter for the calculation of VAR amounts at December 29, 2012 and December 31, 2011, and over each of

the four prior quarters for the calculation of average VAR amounts during each year. The values of commodity options do

not change on a one-to-one basis with the underlying currency or commodity, and were valued accordingly in the VAR

computation.

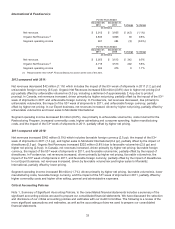

As of December 29, 2012, the estimated potential one-day loss in pre-tax earnings from our commodity and foreign

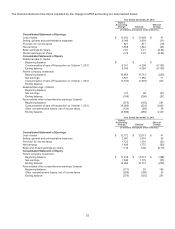

currency instruments and the estimated potential one-day loss in fair value of our interest rate-sensitive instruments, as

calculated in the VAR model, were (in millions):

Pre-Tax Earnings Impact Fair Value Impact

At 12/29/12 Average High Low At 12/29/12 Average High Low

Instruments sensitive to:

Foreign currency rates $ 2 $ 2 $ 3 $ 1

Commodity prices 6 13 18 6

Interest rates $59$42$59$14

Pre-Tax Earnings Impact Fair Value Impact

At 12/31/11 Average High Low At 12/31/11 Average High Low

Instruments sensitive to:

Foreign currency rates $ 1 $ 2 $ 2 $ 1

Commodity prices 14 17 20 13

Interest rates $9$2$9$ -

This VAR computation is a risk analysis tool designed to statistically estimate the maximum probable daily loss from

adverse movements in commodity prices, foreign currency rates, and interest rates under normal market conditions. The

computation does not represent actual losses in fair value or earnings to be incurred by us, nor does it consider the effect

of favorable changes in market rates. We cannot predict actual future movements in such market rates and do not present

these VAR results to be indicative of future movements in such market rates or to be representative of any actual impact

that future changes in market rates may have on our future financial results.

43