Kodak 2013 Annual Report Download - page 90

Download and view the complete annual report

Please find page 90 of the 2013 Kodak annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

|

|

Table of Contents

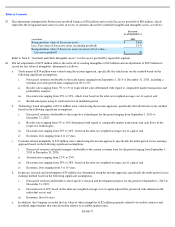

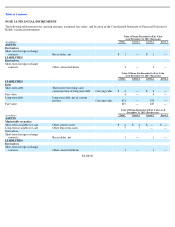

Cash expenditures for pollution prevention and waste treatment for Kodak’s current facilities were as follows:

Environmental expenditures that relate to an existing condition caused by past operations and that do not provide future benefits are expensed

as incurred. Costs that are capital in nature and that provide future benefits are capitalized. Liabilities are recorded when environmental

assessments are made or the requirement for remedial efforts is probable, and the costs can be reasonably estimated. The timing of accruing for

these remediation liabilities is generally no later than the completion of feasibility studies. Kodak has an ongoing monitoring and identification

process to assess how the activities, with respect to the known exposures, are progressing against the accrued cost estimates.

Cash expenditures for the aforementioned investigation, remediation and monitoring activities are expected to be incurred over the next thirty

years for most of the sites. For these known environmental liabilities, the accrual reflects Kodak

’s best estimate of the amount it will incur

under the agreed-upon or proposed work plans. Kodak’s cost estimates were determined using the ASTM Standard E 2137-06, “Standard

Guide for Estimating Monetary Costs and Liabilities for Environmental Matters,” and have not been reduced by possible recoveries from third

parties. The overall method includes the use of a probabilistic model which forecasts a range of cost estimates for the remediation required at

individual sites. The projects are closely monitored and the models are reviewed as significant events occur or at least once per year. Kodak’s

estimate includes investigations, equipment and operating costs for remediation and long-term monitoring of the sites. Accrued liabilities of

Debtor entities related to sites subject to the bankruptcy proceedings were classified as Liabilities subject to compromise as of December 31,

2012. Liabilities subject to compromise were reported at Kodak’s current estimate, where an estimate was determinable, of the allowed claim

amount.

The Amended EBP Settlement Agreement includes a settlement of certain of the Company’

s historical environmental liabilities at EBP through

the establishment of the $49 million EBP Trust. Upon implementation of the Amended EBP Settlement Agreement, (i) the EBP Trust will be

responsible for investigation and remediation at EBP arising from the Company’s historical subsurface environmental liabilities in existence

prior to the effective date of the EBP Settlement, (ii) the Company will fund the EBP Trust with a $49 million payment and transfer of certain

equipment and fixtures used for remediation at EBP, and (iii) in the event the historical liabilities exceed $99 million, the Company will

become liable for 50% of the portion above $99 million. As of the Effective Date, approximately $31 million was already held in a separate

trust to support the environmental liabilities related to EBP, and an escrow account of $18 million was established for the balance of the trust

obligation. The Amended EBP Settlement Agreement is not yet effective and is subject to the satisfaction or waiver of certain conditions

including Bankruptcy Court approval of a covenant not to sue from the U.S. Environmental Protection Agency (“EPA”). The deadline for

implementation of the Amended EBP Settlement Agreement is May 15, 2014.

Prior to the bankruptcy filing, Kodak was designated as a potentially responsible party (“PRP”) under the Comprehensive Environmental

Response, Compensation and Liability Act of 1980, as amended (the “Superfund Law”), or under similar state laws, for environmental

assessment and cleanup costs as the result of Kodak’s alleged arrangements for disposal of hazardous substances at eight Superfund sites. In

connection with the Bankruptcy Filing, the Debtors provided withdrawal notifications or entered into settlement negotiations with involved

regulatory agencies. Each of these sites has been resolved, with the exception of two sites which are contained in a claim by the USA that is

still in the process of resolution.

In addition, the Company provided an indemnity as part of the 1994 sale of Sterling Corporation (now “STWB”), which covered a number of

environmental sites including the Lower Passaic River Study Area (“LPRSA”) portion of the Diamond Alkali Superfund Site. STWB, now

owned by Bayer Corporation, is a potentially responsible party at the site based on alleged releases from facilities formerly owned by

subsidiaries of Sterling. On February 29, 2012, the Company notified STWB and Bayer that, under the bankruptcy proceeding, it has elected to

discontinue funding and participation in remedial investigations of the LPRSA. STWB and its parent, Bayer, filed proofs of claim against the

Debtors in the Chapter 11 Cases. These claims are being discharged pursuant to the Plan.

Estimates of the amount and timing of future costs of environmental remediation requirements are by their nature imprecise because of the

continuing evolution of environmental laws and regulatory requirements, the availability and application of technology, the identification of

presently unknown remediation sites and the allocation of costs among the potentially responsible parties. Based on information presently

available, Kodak does not believe it is reasonably possible that losses for known exposures could exceed current accruals by material amounts,

Successor

Predecessor

(in millions)

For the Four Months

Ended December 31,

2013

For the Eight

Months Ended

August 31, 2013

For the Year Ended

December 31, 2012

For the Year Ended

December 31, 2011

Recurring costs for

pollution prevention and

waste treatment

$

5

$

16

$

28

$

33

Capital expenditures for

pollution prevention and

waste treatment

2

—

1

1

Site remediation costs

—

—

1

2

Total

$

7

$

16

$

30

$

36