Kodak 2013 Annual Report Download - page 30

Download and view the complete annual report

Please find page 30 of the 2013 Kodak annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

|

|

Table of Contents

Additionally, during the eight months ended August 31, 2013, Kodak determined that it was more likely than not that a portion of the deferred

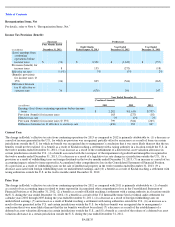

tax assets outside the U.S. would not be realized due to the change in the company’s business as a result of restructuring associated with the

emergence from bankruptcy and accordingly, recorded a provision of $46 million associated with the establishment of a valuation allowance on

those deferred tax assets. During 2012 and 2011, Kodak determined that it was more likely than not that a portion of the deferred tax assets

outside the U.S. would not be realized due to reduced manufacturing volumes negatively impacting profitability in a location outside the U.S.

and accordingly, recorded a provision of $30 million and $53 million, respectively, associated with the establishment of a valuation allowance

on those deferred tax assets.

In general, the amount of tax expense or benefit from continuing operations is determined without regard to the tax effects of other categories

of income or loss, such as Other comprehensive (loss) income. However, an exception to this rule applies when there is a loss from continuing

operations and income from items outside of continuing operations that must be considered. This exception requires that income from

discontinued operations, extraordinary items, and items charged or credited directly to other comprehensive income be considered in

determining the amount of tax benefit that results from a loss in continuing operations. This exception affects the allocation of the tax provision

amongst categories of income.

The undistributed earnings of Kodak’s foreign subsidiaries are not considered permanently reinvested. Kodak recorded a deferred tax liability

(net of related foreign tax credits) of $213 million and $374 million on the foreign subsidiaries’ undistributed earnings for years ended

December 31, 2013 and 2012, respectively. This deferred tax liability was fully offset by Kodak’s U.S. valuation allowance Kodak also

recorded a deferred tax liability of $23 million and $42 million for the potential foreign withholding taxes on the undistributed earnings for

years ended December 31, 2013 and 2012, respectively.

Kodak operates within multiple taxing jurisdictions worldwide and is subject to audit in these jurisdictions. These audits can involve complex

issues, which may require an extended period of time for resolution. Management’s ongoing assessments of the more-likely-than-not outcomes

of these issues and related tax positions require judgment, and although management believes that adequate provisions have been made for

such issues, there is the possibility that the ultimate resolution of such issues could have an adverse effect on the earnings of

Kodak. Conversely, if these issues are resolved favorably in the future, the related provisions would be reduced, thus having a positive impact

on earnings.

Pension and Other Postretirement Benefits

Kodak’s defined benefit pension and other postretirement benefit costs and obligations are estimated using several key assumptions. These

assumptions, which are reviewed at least annually by Kodak, include the discount rate, long-term expected rate of return on plan assets

(“EROA”), salary growth, healthcare cost trend rate, mortality trends and other economic and demographic factors. Actual results that differ

from Kodak’

s assumptions are recorded as unrecognized gains and losses and are amortized to earnings over the estimated future service period

of the active participants in the plan or, if almost all of a plan’s participants are inactive, the average remaining lifetime expectancy of inactive

participants, to the extent such total net unrecognized gains and losses exceed 10% of the greater of the plan’s projected benefit obligation or

the calculated value of plan assets. Significant differences in actual experience or significant changes in future assumptions would affect

Kodak’s pension and other postretirement benefit costs and obligations.

Asset and liability modeling studies are utilized by Kodak to adjust asset exposures and review a liability hedging program through the use of

forward looking correlation, risk and return estimates. Those forward looking estimates of correlation, risk and return generated from the

modeling studies are also used to estimate the EROA. The EROA is estimated utilizing a forward-

looking building block model factoring in the

expected risk of each asset category, return and correlation over a five to seven year horizon, and weighting the exposures by the current asset

allocation. Historical inputs are utilized in the forecasting model to frame the current market environment with adjustments made based on the

forward looking view. Kodak aggregates investments into major asset categories based on the underlying benchmark of the strategy. Kodak’s

asset categories include broadly diversified exposure to U.S. and non-U.S. equities, U.S. and non-U.S. government and corporate bonds,

inflation-linked bonds, commodities and absolute return strategies. Each allocation to these major asset categories is determined within the

overall asset allocation to accomplish unique objectives, including enhancing portfolio return, providing portfolio diversification, or hedging

plan liabilities.

The EROA, once set, is applied to the calculated value of plan assets in the determination of the expected return component of Kodak’

s pension

expense. Kodak uses a calculated value of plan assets, which recognizes gains and losses in the fair value of assets over a four-year period, to

calculate expected return on assets. At December 31, 2013, the calculated value of the assets of Kodak’s major U.S. and non-U.S. defined

benefit pension plans was approximately $5.0 billion and the fair value was approximately $5.1 billion. Asset gains and losses that are not yet

reflected in the calculated value of plan assets are not included in amortization of unrecognized gains and losses.

PAGE 28