Hyundai 2014 Annual Report Download - page 51

Download and view the complete annual report

Please find page 51 of the 2014 Hyundai annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

|

|

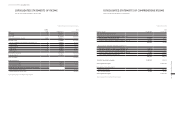

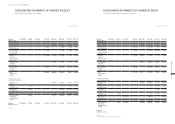

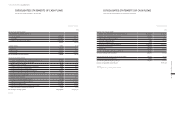

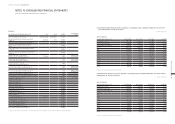

HYUNDAI MOTOR COMPANY Annual Report 2014

FINANCIAL STATEMENTS / 101100

share of losses of an associate or a joint venture exceeds the

Group’s interest in that associate or joint venture (which in-

cludes any long-term interests that, in substance, form part of

the Group’s net investment in the associate or the joint ven-

ture), the Group discontinues recognizing its share of further

losses. Additional losses are recognized only to the extent that

the Group has incurred legal or constructive obligations or made

payments on behalf of the associate or the joint venture.

Any excess of the cost of acquisition over the Group’s share of

the net fair value of the identifiable assets, liabilities and con-

tingent liabilities of an associate or a joint venture recognized

at the date of acquisition is recognized as goodwill, which is in-

cluded within the carrying amount of the investment. The entire

carrying amount of the investment including goodwill is tested

for impairment and presented at the amount less accumulated

impairment losses. Any excess of the Group’s share of the net

fair value of the identifiable assets, liabilities and contingent

liabilities over the cost of acquisition, after reassessment, is

recognized immediately in profit or loss.

Upon disposal of an associate or a joint venture that results in

the Group losing significant influence over that associate or joint

venture, any retained investment is measured at fair value at that

date and the fair value is regarded as its fair value on initial rec-

ognition as a financial asset in accordance with K-IFRS 1039. The

difference between the previous carrying amount of the asso-

ciate or joint venture attributable to the retained interest and its

fair value is included in the determination of the gain or loss on

disposal of the associate or joint venture. In addition, the Group

accounts for all amounts previously recognized in other com-

prehensive income in relation to that associate or joint venture

on the same basis we would be required if that associate or joint

venture had directly disposed of the related assets or liabilities.

Therefore, if a gain or loss previously recognized in other com-

prehensive income by that associate or joint venture would be

reclassified to profit or loss on the disposal of the related assets

or liabilities, the Group reclassifies the gain or loss from equity

to profit or loss (as reclassification adjustment) when it loses

significant influence over that associate or joint venture.

When the Group reduces its ownership interest in an associate

or a joint venture but the Group continues to use the equity

method, the Group reclassifies to profit or loss the proportion

of the gain or loss that had previously been recognized in other

comprehensive income relating to that reduction in ownership

interest if that gain or loss would be reclassified to profit or loss

on the disposal of the related assets or liabilities. In addition, the

Group applies K-IFRS 1105 to a portion of investment in an as-

sociate or a joint venture that meets the criteria to be classified

as held for sale.

The Group continues to use the equity method when an invest-

ment in an associate becomes an investment in a joint venture

or an investment in a joint venture becomes an investment in an

associate. There is no remeasurement to fair value upon such

changes in ownership interests.

Unrealized gains from transactions between the Group and its

associates or joint ventures are eliminated up to the shares in

associate (joint venture) stocks. Unrealized losses are also elim-

inated unless evidence of impairment in assets transferred is

produced. If the accounting policy of associates or joint ventures

differs from the Group, financial statements are adjusted accord-

ingly before applying equity method of accounting. If the Group’s

ownership interest in an associate or a joint venture is reduced,

but the significant influence is continued, the Group reclassifies

to profit or loss only a proportionate amount of the gain or loss

previously recognized in other comprehensive income.

(12) Property, plant and equipment

Property, plant and equipment is to be recognized if, and only if

it is probable that future economic benefits associated with the

asset will flow to the Group, and the cost of the asset can be

measured reliably. After the initial recognition, property, plant

and equipment is stated at cost less accumulated depreciation

and accumulated impairment losses. The cost includes any cost

directly attributable to bringing the asset to the location and

condition necessary for it to be capable of operating in the

manner intended by management and the initial estimate of the

costs of dismantling and removing the item and restoring the

site on which it is located. In addition, in case the recognition

criteria are met, the subsequent costs will be added to the car-

rying amount of the asset or recognized as a separate asset,

and the carrying amount of what was replaced is derecognized.

Depreciation is computed using the straight-line method based

on the estimated useful lives of the assets. The representative

useful lives are as follows:

Representative useful lives (years)

Buildings and structures 2 - 50

Machinery and equipment 2 - 25

Vehicles 3 - 20

Dies, molds and tools 2 - 15

Office equipment 2 - 20

Other 2 - 30

The Group reviews the depreciation method, the estimated use-

ful lives and residual values of property, plant and equipment at

the end of each annual reporting period. If expectations differ

from previous estimates, the changes are accounted for as a

change in accounting estimate.

(13) Investment property

Investment property is property held to earn rentals or for cap-

ital appreciation or both. An investment property is measured

initially at its cost and transaction costs are included in the

initial measurement. After initial recognition, the book value of

investment property is presented at the cost less accumulated

depreciation and accumulated impairment losses.

Subsequent costs are recognized as the carrying amount of the

asset when, and only when it is probable that future economic

benefits associated with the asset will flow to the Group, and

the cost of the asset can be measured reliably, or recognized

as a separate asset if appropriate. The carrying amount of what

was replaced is derecognized.

Land is not depreciated, and other investment properties are

depreciated using the straight-line method over the period from

20 to 50 years. The Group reviews the depreciation method, the

estimated useful lives and residual values at the end of each

annual reporting period. If expectations differ from previous es-

timates, the changes are accounted for as a change in account-

ing estimate.

(14) Intangible assets

1) Goodwill

Goodwill arising from a business combination is recognized as

an asset at the time of obtaining control (the acquisition-date).

Goodwill is measured as the excess of the aggregate of the

consideration transferred, the amount of any non-controlling

interest in the acquiree, and the acquisition-date fair value of

the Group’s previously held equity interest in the acquiree over

the net of the acquisition-date amounts of the identifiable as-

sets acquired and the liabilities assumed.

If, after reassessment, the net of the acquisition-date amounts

of the identifiable assets acquired and the liabilities assumed

exceeds the aggregate of the consideration transferred, the

amount of any non-controlling interest in the acquiree, and the

acquisition-date fair value of the Group’s previously held equity

interest in the acquiree, the excess is recognized immediately in

profit or loss as a bargain purchase gain.

Goodwill is not amortized but tested for impairment at least an-

nually. For purposes of impairment tests, goodwill is allocated

to those cash generating units (“CGU”) of the Group expected

to have synergy effect from the business combination. CGU

that goodwill has been allocated is tested for impairment every

year or when an event occurs that indicates impairment. If re-

coverable amount of a CGU is less than its carrying amount, the

impairment will first decrease the goodwill allocated to that CGU

and the remaining impairment will be allocated among other

assets relative to its carrying value. Impairment recognized for

goodwill may not be reversed. When disposing a subsidiary, re-

lated goodwill will be included in gain or loss from disposal.

2) Development costs

The expenditure on research is recognized as an expense when

it is incurred. The expenditure on development is recognized

as an intangible asset if, and only if, all of the following can be

demonstrated:

■ the technical feasibility of completing the intangible asset so

that it will be available for use or sale;

■ the intention to complete the intangible asset and use or sell it;

■ the ability to use or sell the intangible asset;

■ how the intangible asset will generate probable future eco-

nomic benefits;

■ the availability of adequate technical, financial and other re-

sources to complete the development and to use or sell the

intangible asset; and

■ the ability to measure reliably the expenditure attributable to

the intangible asset during its development.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

AS OF AND FOR THE YEARS ENDED DECEMBER 31, 2014 AND 2013