HSBC 2004 Annual Report Download - page 357

Download and view the complete annual report

Please find page 357 of the 2004 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

347 -

348

348 -

349

349 -

350

350 -

351

351 -

352

352 -

353

353 -

354

354 -

355

355 -

356

356 -

357

357 -

358

358 -

359

359 -

360

360 -

361

361 -

362

362 -

363

363 -

364

364 -

365

365 -

366

366 -

367

367 -

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

|

|

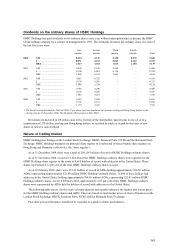

355

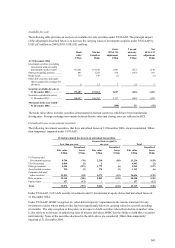

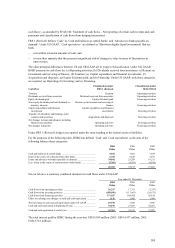

US$30.3 billion in 2004 (2003: US$25.0 billion). Net gains (gross gains less estimated credit losses under the

recourse provisions) related to these replenishments were calculated using weighted-average assumptions

consistent with those used for calculating gains on initial securitisations and totalled US$414 million in 2004

(2003: US$412 million).

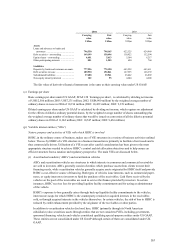

Cash flows received from securitisation trusts were as follows:

2004

Real Estate

Secured

Auto

Finance

MasterCard/

Visa

Private

Label

Personal

Non-Credit

Card Total

US$m US$m US$m US$m US$m US$m

Proceeds from initial

securitisations...................... – – 550 190 – 740

Servicing fees received ............ 1 86 185 93 161 526

Other cash flow received on

retained interests1................ 4 (9) 705 252 80 1,032

2003

Proceeds from initial

securitisations...................... – 1,158 350 1,050 2,810 5,368

Servicing fees received ............ 2 86 149 65 100 402

Other cash flow received on

retained interests1................ 8 50 635 193 132 1,018

1Other cash flows included all cash flows from interest-only strip receivables, excluding servicing fees.

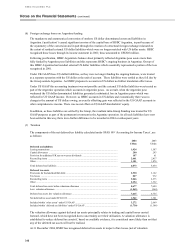

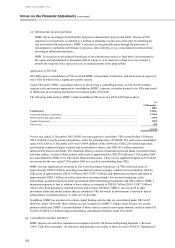

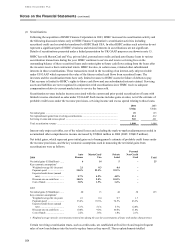

At 31 December 2004, the sensitivity of the current fair value of the interest-only strip receivables to an

immediate 10 per cent and 20 per cent unfavourable change in assumptions are presented in the table below.

These sensitivities are based on assumptions used to value interest-only strip receivables at 31 December 2004.

Real Estate

Secured

Auto

Finance

MasterCard/

Visa

Private

Label

Personal

Non-Credit

Card

Carrying value (fair value) of interest- only strip

receivables (US$ millions) ............................. 1 36 162 50 124

Weighted-average life (in years) ......................... 0.3 1.6 0.5 0.5 0.9

Payment speed assumption (annual rate) ............. 21.5% 44.7% 81.4% 79.0% 69.9%

Impact on fair value of 10% adverse change

(US$ millions) ............................................ – (16) (13) (3) (8)

Impact on fair value of 20% adverse change

(US$ millions) ............................................ – (33) (24) (5) (15)

Expected credit losses (annual rate) .................... 1.8% 8.2% 5.2% 5.7% 10.1%

Impact on fair value of 10% adverse change

(US$ millions) ............................................ – (30) (14) (8) (30)

Impact on fair value of 20% adverse change

(US$ millions) ............................................ – (59) (28) (17) (61)

Discount rate on residual cash flows (annual

rate) ................................................................. 13.0% 10.0% 9.0% 10.0% 11.0%

Impact on fair value of 10% adverse change

(US$ millions) ............................................ –(4)(1)–(1)

Impact on fair value of 20% adverse change

(US$ millions) ............................................ –(9)(2)–(2)

Variable returns to investors (annual rate) ........... 1.7% – 1.9% 3.1% 3.3%

Impact on fair value of 10% adverse change

(US$ millions) ............................................ – – (6) (5) (10)

Impact on fair value of 20% adverse change

(US$ millions)............................................. – – (13) (10) (20)

These sensitivities are hypothetical and should not be considered to be predictive of future performance. As the

figures indicate, the change in fair value based on a 10 per cent variation in assumptions cannot necessarily be

extrapolated because the relationship of the change in assumption to the change in fair value may not be linear.

Also, in this table, the effect of a variation in a particular assumption on the fair value of the residual cash flow is

calculated independently from any change in another assumption. In reality, changes in one factor may