HSBC 2004 Annual Report Download - page 123

Download and view the complete annual report

Please find page 123 of the 2004 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

|

|

121

For securities carried at amortised cost

impairment may result from changes in their

estimated fair value if management changes its

assumptions regarding the above variables. In such

circumstances, it will also be necessary for

management to exercise judgement as to whether or

not the indicative change in estimated fair value

arising from revisions to the underlying valuation

assumptions are only temporary.

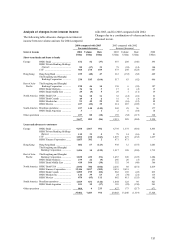

The table below summarises HSBC’ s trading

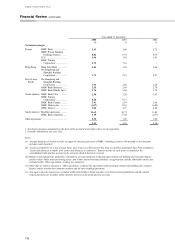

portfolios by valuation methodology at 31 December

2004:

Trading assets Trading liabilities

Securities

purchased Derivatives

Securities

sold Derivatives

%%%%

Fair value based on:

Quoted market prices .................................................... 81.0 6.0 81.0 6.0

Internal models with significant observable

market parameters ..................................................... 18.0 93.0 19.0 94.0

Internal models with significant unobservable

market parameters ..................................................... 1.01.0––

Total .............................................................................. 100.0 100.0 100.0 100.0

For a discussion of market risk management, see

Market Risk Management on pages 167 to 172.

UK GAAP compared with US GAAP

2004 2003 2002

US$m US$m US$m

Net income

US GAAP .................... 12,506 7,231 4,900

UK GAAP .................... 11,840 8,774 6,239

Shareholders’ equity

US GAAP .................... 90,082 80,251 55,831

UK GAAP .................... 86,623 74,473 51,765

Differences in net income and shareholders’ equity

are explained in Note 49 of the ‘Notes on the

Financial Statements on pages 322 to 356.

Future accounting developments

Transition to International Financial Reporting

Standards

The adoption of International Financial Reporting

Standards (‘IFRS’ ) from 1 January 2005 is the most

significant accounting development for HSBC.

The European Union (‘EU’ ) requires that listed

European companies prepare their 2005 financial

statements in accordance with EU-endorsed IFRS.

HSBC’ s 2005 interim financial statements will,

therefore, be prepared in accordance with IFRS. The

European Union endorsement process for IFRS is

ongoing but the majority of standards are now

endorsed including IAS 32 ‘Financial Instruments:

Disclosure and Presentation’ and most of IAS 39

‘Financial Instruments: Recognition and

Measurement’ with the exception of the deletion of a

limited number of words and paragraphs in IAS 39

including those relating to the use of the ‘fair value

option’ for financial liabilities.

HSBC has substantially completed its transition

to IFRS. The process of refining systems and

processes in order to collect data on a fully IFRS-

compliant basis for 2005 reporting is well advanced.

On 9 December 2004, HSBC filed with the US

Securities and Exchange Commission a summary of

the applicable significant differences between UK

GAAP and IFRS. This should be referred to for

details of the major IFRS effects on HSBC Group,

and is available from http://www.hsbc.com/hsbc/

investor_centre/financial-results.

IFRS will also impact HSBC Holdings’

individual accounts. Investments in subsidiary

undertakings will be carried at cost rather than net

asset value, including attributable goodwill, adjusted

for shares held by subsidiaries in HSBC Holdings.

Under IFRS, in addition to the balance sheet, HSBC

Holdings will publish an income statement and other

primary financial statements.

HSBC currently intends to file 2004

comparative data and the 2005 opening balance

sheet on an IFRS basis in the second quarter of 2005.

FRS 27 ‘Life Assurance’ was issued by the UK

Accounting Standards Board (‘ASB’ ) in December

2004. This standard is effective under UK GAAP for

2005 reporting and thus should not ostensibly be

applicable to companies adopting IFRS for 2005.

However, FRS 27 adds to the requirements of IFRS

4 ‘Insurance contracts’ with regard to further

requirements in relation to measurement of realistic

liabilities and disclosure of capital position. HSBC

continues to assess the likely impact of this

accounting standard.