HSBC 2004 Annual Report Download - page 324

Download and view the complete annual report

Please find page 324 of the 2004 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

314 -

315

315 -

316

316 -

317

317 -

318

318 -

319

319 -

320

320 -

321

321 -

322

322 -

323

323 -

324

324 -

325

325 -

326

326 -

327

327 -

328

328 -

329

329 -

330

330 -

331

331 -

332

332 -

333

333 -

334

334 -

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

|

|

HSBC HOLDINGS PLC

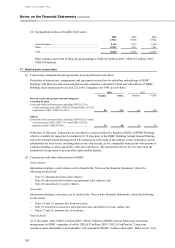

Notes on the Financial Statements (continued)

322

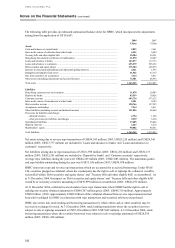

49 Differences between UK GAAP and US GAAP

The consolidated financial statements of HSBC are prepared in accordance with UK GAAP which differs in certain

significant respects from US GAAP. The following is a summary of the significant differences applicable to HSBC:

Leasing

UK GAAP

• Finance lease income is recognised so as to give a constant rate of return on the net cash investment in the lease,

taking into account tax payments and receipts associated with the lease.

• Leases are categorised as finance leases when the substance of the agreement is that of a financing transaction

and the lessee assumes substantially all of the risks and benefits relating to the asset. All other leases are

categorised as operating leases.

• Operating leased assets are depreciated over their useful lives so that, for each asset, rentals less depreciation are

recognised at a constant periodic rate of return on the net cash invested in that asset. Rentals receivable under

operating leases are accounted for on a straight-line basis over the lease term.

US GAAP

• Unearned income on finance leases is taken to income at a rate calculated to give a constant rate of return on the

investment in the lease, but generally no account is taken of the tax flows generated by the lease.

• Leases are classified as capital leases when any of the criteria outlined under Statement of Financial Accounting

Standards (‘SFAS’ ) 13 ‘Accounting for leases’ are met.

• Operating leased assets are depreciated so that in each period the depreciation charge is at least equal to that

which would have arisen on a straight-line basis.

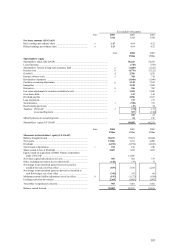

Shareholders’ interest in the long-term assurance fund

UK GAAP

• The value placed on HSBC’ s interest in long-term assurance business includes a valuation of the discounted

future earnings expected to emerge from business currently in force, taking into account factors such as recent

experience and general economic conditions, together with the surplus retained in the long-term assurance funds.

These are determined annually in consultation with external actuaries and are included in ‘Other assets’ .

• Changes in the value of HSBC’ s interest in long-term assurance business are calculated on a post-tax basis and

are reported in the profit and loss account as part of ‘Other operating income’ after adjusting for taxation.

US GAAP

• The net present value of these profits is not recognised. Acquisition costs and fees are deferred and amortised in

accordance with SFAS 97 ‘Accounting and reporting by insurance enterprises for certain long-duration contracts

and for realised gains and losses from the sale of investments’ .

Long-term assurance assets and liabilities

UK GAAP

• Long-term assurance fund assets, excluding own shares held, and liabilities attributable to policyholders are

recognised at fair value in ‘Other assets’ and ‘Other liabilities’ as summary amounts ‘Long-term assurance

assets/liabilities attributable to policyholders’ .

US GAAP

• Under the Statement of Position issued by the American Institute of Certified Public Accountants (‘AICPA

SOP’ ) 03-1, ‘Accounting and reporting by Insurance Enterprises for certain Non-traditional and Long-duration

Contracts and for Separate Accounts’ , which became fully effective in 2004, where assets qualify for separate

accounting they should be measured at fair value and be reported in the financial statements as a summary total,

with an equivalent summary total for related liabilities, consistent with the UK GAAP presentations. Otherwise,

assets representing policyholders funds under the arrangements should be accounted for and recognised as