HSBC 2004 Annual Report Download - page 267

Download and view the complete annual report

Please find page 267 of the 2004 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

262 -

263

263 -

264

264 -

265

265 -

266

266 -

267

267 -

268

268 -

269

269 -

270

270 -

271

271 -

272

272 -

273

273 -

274

274 -

275

275 -

276

276 -

277

277 -

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

|

|

265

HSBC is not obliged to support any losses that may be suffered by the FRN holders and does not intend to provide

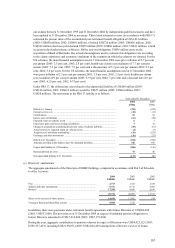

such support.

HSBC has taken up US$58 million (2003: US$73 million) of subordinated FRNs that are repayable after payments in

respect of senior FRNs. HSBC has made subordinated loans of US$37 million (2003: US$46 million) to Clover

Funding that are repayable after all other payments. Interest is payable on the subordinated FRNs and subordinated

loans conditional upon Clover Funding having funds available.

Clover Securitisation Limited’ s entire share capital is held by Clover Holdings Limited. Clover Funding’ s entire

share capital is held by Clover Holdings Limited. Clover Holdings Limited’ s entire share capital is held by trustees

under the terms of a trust for charitable purposes.

HSBC recognised net income of US$8 million (2003: US$7 million) which comprised US$114 million (2003:

US$108 million) of interest receivable by Clover Funding less US$106 million (2003: US$101 million) of interest on

FRNs and other third party expenses payable by Clover Funding.

HFC Bank Limited Securitisations

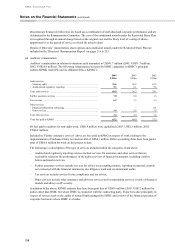

HSBC, through its wholly-owned subsidiary company, HFC Bank, has securitised certain amounts of its personal

loan portfolios. The transactions were effected through equitable assignment of those loans to receivables trusts,

beneficial interests in which were purchased by several special purpose companies.

To fund the acquisition of these beneficial interests, the special purpose companies have issued asset backed notes,

discounted notes, and subordinated loans, or have received funds on-lent by other companies that have issued such

securities and loans for this purpose. Certain of the notes issued were credit enhanced by a third party to provide the

required ratings at the time of issue. The securitisation documentation sets out the acknowledgement by the special

purpose companies that they will seek to repay their financing only to the extent that repayment is funded by the

proceeds generated by the securitised personal loans, and that they will not seek recourse in any other form from

HFC Bank.

As at 31 December 2004 non-returnable proceeds of US$149 million (2003: US$409 million) received by HFC Bank

from the receivables trusts have been deducted from ‘Loans and advances to customers’ . Certain of the special

purpose companies have entered into swap agreements with HFC Bank (via a third party swap provider) under which

the special purpose companies pay the fixed rate of interest on the personal loans and receive a floating interest rate.

The proceeds generated from the loans are used in priority to meet the claims of the note holders and other lenders,

and amounts payable in respect of the interest rate swap arrangements after the payment of trustee and administration

expenses. HFC Bank is entitled to any residual income from the personal loans after the claims of the note-holders,

other lenders and swap counterparties are met.

Under the terms of the securitisation agreements, during the initial periods of the securitisations, HFC Bank was able

to substitute securitised loans that were prepaid or expired with further loans that met the same criteria as those

originally securitised. In 2004, the special purpose companies acquired no qualifying personal loans from HFC Bank

under these arrangements (2003, in the period since the acquisition of HFC Bank by HSBC: US$94 million). The

initial periods have now expired, and further substitutions are no longer possible.

There is no provision whatsoever, either in the financing arrangements or otherwise, whereby HFC Bank has a right

or obligation either to keep the loans and advances on repayment of the finance or to repurchase them at any time

other than in certain circumstances where HFC Bank is in breach of warranty.

HFC Bank is not obliged to support any losses that may be suffered by the note-holders and does not intend to

provide such support.

The entire share capital of the special purpose companies is indirectly held by trustees under the terms of a trust for

charitable purposes.

In 2004, HFC Bank recognised net income of US$9 million (2003, in the period since the acquisition of HFC Bank

by HSBC: US$33 million) from these personal loan securitisations.