HSBC 2004 Annual Report Download - page 124

Download and view the complete annual report

Please find page 124 of the 2004 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

|

|

HSBC HOLDINGS PLC

Financial Review (continued)

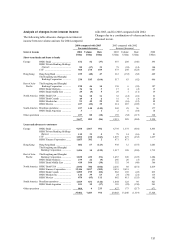

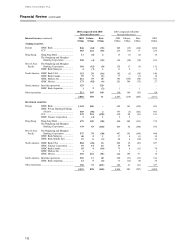

122

US GAAP

The Financial Accounting Standards Board

(‘FASB’ ) (US GAAP) has issued the following

accounting standards, which become fully effective

in future financial statements.

In December 2003, the American Institute of

Certified Public Accountants (‘AICPA’ ) released

Statement of Position 03-3, ‘Accounting for Certain

Loans or Debt Securities Acquired in a Transfer’

(‘SOP 03-3’ ). SOP 03-3 addresses accounting for

differences between contractual cash flows and cash

flows expected to be collected from an investor’ s

initial investment in loans or debt securities acquired

in a transfer if those differences are attributable to

credit quality. SOP 03-3 is effective for loans

acquired in fiscal years beginning after 15 December

2004. Adoption is not expected to have a material

impact on the US GAAP information in HSBC’ s

financial statements.

In March 2004, the FASB reached a consensus

on Emergent Issues Task Force (‘EITF’ ) 03-1, ‘The

Meaning of Other-Than-Temporary Impairment and

Its Application to Certain Investments’ . EITF 03-1

provides guidance for determining when an

investment is impaired and whether the impairment

is other than temporary. EITF 03-1 also incorporates

into its consensus the required disclosures about

unrealised losses on investments announced by the

EITF in late 2003 and adds new disclosure

requirements relating to cost-method investments.

The new disclosure requirements are effective for

annual reporting periods ending after June 15, 2004

and the new impairment accounting guidance was to

become effective for reporting periods beginning

after June 15, 2004. In September 2004, the FASB

delayed the effective date of EITF 03-1 for

measurement and recognition of impairment losses

until implementation guidance is issued. In

December 2004, the FASB decided to reconsider in

its entirety all guidance on disclosing, measuring and

recognising other-than-temporary impairments of

debt and equity securities and requires companies to

continue to comply with existing accounting

literature. Until the new guidance is finalised, the

impact on HSBC’ s financial position and results of

operations cannot be determined.

SFAS 123 (revised 2004) ‘Share-Based

Payment’ (‘SFAS 123R’ ) was issued in December

2004 to replace SFAS 123 ‘Accounting for Stock

Based Compensation’ (‘SFAS 123’ ). SFAS 123R

requires a fair value method of accounting for stock-

based compensation plans. Under the fair value

method, compensation cost is measured at the date

of grant based on the value of the award and is

recognised over the service period. HSBC had

already elected to follow the fair value method

encouraged by SFAS 123. Where annual bonuses are

awarded in restricted shares, and the employee must

remain with HSBC for a fixed period in order to

receive the shares, HSBC has, to date, interpreted the

service period as being the year to which the bonus

relates. HSBC has fully expensed the share award in

that year under US GAAP, consistent with the UK

GAAP treatment. Under SFAS 123R, the service

period is presumed to be the vesting period, i.e. the

period the employee must remain with HSBC.

Accordingly, for awards granted after the effective

date of SFAS 123R, the expense of such awards will

be spread forward over the vesting period. HSBC

will adopt SFAS 123R from 1 July 2005.

The effect of adopting this new accounting

treatment will be that 2005 bonuses paid in restricted

shares will be excluded from staff costs for 2005 and

instead will be expensed over the vesting period with

a corresponding increase in net income. The amount

of these awards is dependent on 2005 performance.

2004 bonuses that will be paid in restricted shares

were approximately US$130 million.