HSBC 2004 Annual Report Download - page 160

Download and view the complete annual report

Please find page 160 of the 2004 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

|

|

HSBC HOLDINGS PLC

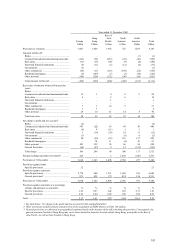

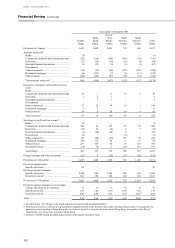

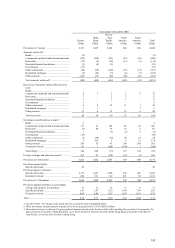

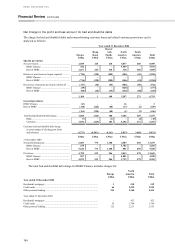

Financial Review (continued)

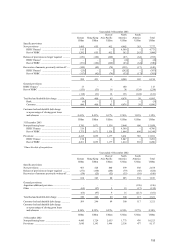

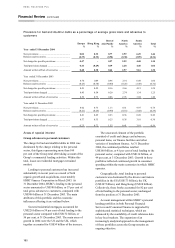

158

quarter, improved collections and the sales of

charged-off accounts. In Europe, excluding

HSBC Finance, releases and recoveries were

US$344 million higher, of which US$51 million

arose from currency translation effects. At

constant currencies, the increase reflected

releases of provisions in the energy, utilities and

petroleum sectors in the UK and manufacturing

and transport equipment sectors in France, while

recoveries benefited from the sale in the

secondary market of loans to a borrower in the

engineering sector. In North America, excluding

HSBC Finance, releases and recoveries

increased by US$126 million. The improvement

reflected an ongoing workout programme to

reduce the legacy bad debt portfolio in Mexico,

higher repayments of previously non-

performing loans in the US and the sale of

impaired loans in the US secondary market. In

Hong Kong, the benign credit environment and

rising house prices contributed to a rise in

releases and recoveries for residential

mortgages. This offset a general fall in the levels

of releases and recoveries in the Hong Kong

commercial sector that was also evident across

the Rest of Asia-Pacific. The sharp increase in

releases and recoveries in South America largely

reflected the inclusion of the Losango consumer

lending business and organic growth in Brazil,

together with successful collections activities in

Argentina.

• The general provision release of

US$436 million in 2004 compared with a

release of US$121 million in 2003. In Hong

Kong, the net release of US$224 million

reflected a reduction in the estimated latent loan

losses at 31 December 2004. Estimates of latent

losses reflect the historical experience of the rate

at which such losses occur and are based on the

structure of the credit portfolio and the

economic and credit conditions prevailing at the

balance sheet date. A similar situation was seen

in Malaysia, Singapore and Indonesia where

stable economic conditions were reflected in an

improvement in credit quality and reduction in

latent loan losses. As a result, the net charge for

the Rest of Asia-Pacific in 2003 became a net

release in 2004. In North America, the small

general provision release compared with a

charge of US$136 million in 2003 and reflected

an improvement in the economic outlook and

delinquency roll-rate trends in HSBC Finance

Corp, and a smaller charge in Mexico. In

Europe, the increase in general provisions

required from the growth in lending balances

was offset by the impact of the improvement in

both historical loss experience and credit

conditions in general. The substantial general

provision release in South America in 2003

reflecting improved collections and an

improvement in the general quality of the loan

book in Argentina was not repeated in 2004.

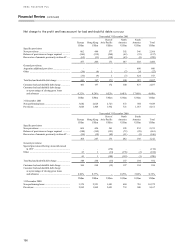

Year ended 31 December 2003 compared

with year ended 31 December 2002

The increase in the level of new specific provisions

was principally driven by:

• New provisions in North America, which were

US$4,563 million higher than in 2002,

essentially reflected the acquisition of HSBC

Finance Corporation, which reported

US$4,580 million of new provisions. The

majority of HSBC Finance’ s customer loans are

in the consumer finance sector and are

geographically well-spread across the United

States. During the period since its acquisition,

HSBC Finance Corporation’ s new provisions

reflected the impact of the weak economy,

including higher personal bankruptcy filings and

a higher level of amounts becoming past due. In

the latter part of 2003, there were signs of an

improvement in credit quality and delinquency

levels stabilised. At 31 December 2003, HSBC

Finance’ s two-month-and-over consumer

contractual delinquency ratio was 5.8 per cent.

A charge of US$48 million from HSBC Mexico

arose from consumer lending and credit card

portfolios, which are provisioned on a portfolio

basis. In Canada, new provisions in 2003 were

US$66 million lower than in 2002, when

significant new provisions for a small number of

commercial facilities were necessary, most

notably in the telecommunications sector.

• In Europe, new provisions were US$522 million

higher than in 2002 of which US$193 million

related to HSBC Finance Corporation’s UK

consumer finance business, which is

provisioned on a portfolio basis. Elsewhere in

the UK, the increase in new provisions in

personal lending reflected the growth in loan

portfolios. In the corporate and commercial

portfolio, new provisions were raised to cover a

number of accounts in the energy and

manufacturing sectors. In France, there were

higher provisions, principally due to the

deterioration of a borrower in the engineering

sector.

• New provisions in Hong Kong were

US$127 million higher than in 2002. Higher

levels of new provisions were required in the