HSBC 2004 Annual Report Download - page 327

Download and view the complete annual report

Please find page 327 of the 2004 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

317 -

318

318 -

319

319 -

320

320 -

321

321 -

322

322 -

323

323 -

324

324 -

325

325 -

326

326 -

327

327 -

328

328 -

329

329 -

330

330 -

331

331 -

332

332 -

333

333 -

334

334 -

335

335 -

336

336 -

337

337 -

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

|

|

325

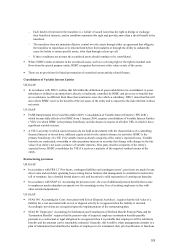

Derivatives

UK GAAP

• Non-trading derivatives are those which are held for hedging purposes as part of HSBC’ s risk management

strategy against cash flows, assets, liabilities, or positions measured on an accruals basis. Non-trading

transactions include qualifying hedges and positions that synthetically alter the characteristics of specified

financial instruments.

• Non-trading derivatives are accounted for on an equivalent basis to the underlying assets, liabilities or net

positions. Any profit or loss arising is recognised on the same basis as that arising from the related assets,

liabilities or positions.

• To qualify as a hedge, a derivative must effectively reduce the price, foreign exchange or interest rate risk of the

asset, liability or anticipated transaction to which it is linked and be designated as a hedge at inception of the

derivative contract. Accordingly, changes in the market value of the derivative must be highly correlated with

changes in the market value of the underlying hedged item at inception of the hedge and over the life of the

hedge contract. If these criteria are met, the derivative is accounted for on the same basis as the underlying

hedged item. Derivatives used for hedging purposes include swaps, forwards and futures.

• Interest rate swaps are also used to alter synthetically the interest rate characteristics of financial instruments. In

order to qualify for synthetic alteration, a derivative instrument must be linked to specific individual, or pools of

similar, assets or liabilities by the notional principal and interest rate risk of the associated instruments, and must

achieve a result that is consistent with defined risk management objectives. If these criteria are met, accrual

based accounting is applied, i.e. income or expense is recognised and accrued to the next settlement date in

accordance with the contractual terms of the agreement.

• Any gain or loss arising on the termination of a qualifying derivative is deferred and amortised to earnings over

the original life of the terminated contract. Where the underlying asset, liability or position is sold or terminated,

the qualifying derivative is immediately marked-to-market through the profit and loss account.

• Derivatives that do not qualify as hedges or synthetic alterations at inception are marked-to-market through the

profit and loss account, with gains and losses included within ‘Dealing profits’ .

US GAAP

• All derivatives must be recognised as either assets or liabilities in the balance sheet and be measured at fair value

(SFAS 133 ‘Accounting for Derivative Instruments and Hedging Activities’ ).

• The accounting for changes in the fair value of a derivative (i.e. gains and losses) depends on the intended use of

the derivative and the resulting designation as described below:

– For a derivative designated as hedging exposure to changes in the fair value of a recognised asset or liability

or a firm commitment, the gain or loss is recognised in earnings in the period of change together with the

associated loss or gain on the hedged item attributable to the risk being hedged. Any resulting net gain or

loss represents the ineffective portion of the hedge.

– For a derivative designated as hedging exposure to variable cash flows of a recognised asset or liability, or

of a forecast transaction, the derivative’ s gain or loss associated with the effective portion of the hedge is

initially reported as a component of other comprehensive income and subsequently reclassified into earnings

when the forecast transaction affects earnings. The ineffective portion is reported in earnings immediately.

– For net investment hedges in which derivatives hedge the foreign currency exposure of a net investment in a

foreign operation, the change in fair value of the derivative associated with the effective portion of the hedge

is included as a component of other comprehensive income (‘OCI’ ), together with the associated loss or gain

on the hedged item. The ineffective portion is reported in earnings immediately.

– In order to apply hedge accounting it is necessary to comply with documentation requirements and to

demonstrate the effectiveness of the hedge on a retrospective and prospective basis.

– For a derivative not designated as a hedging instrument, the gain or loss is recognised in earnings in the

period of change in fair value.