DIRECTV 2004 Annual Report Download - page 59

Download and view the complete annual report

Please find page 59 of the 2004 DIRECTV annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

|

|

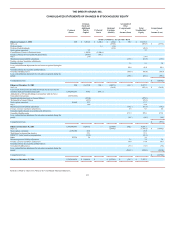

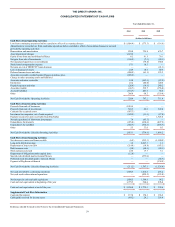

THE DIRECTV GROUP, INC.

The goodwill evaluation requires the estimation of the fair value of reporting units where we record goodwill. We determine fair

values primarily using estimated cash flows discounted at a rate commensurate with the risk involved, when appropriate.

Estimation of future cash flows requires significant judgment about future operating results, and can vary significantly from one

evaluation to the next. Risk adjusted discount rates are not fixed and are subject to change over time. As a result, changes in

estimated future cash flows and/or changes in discount rates could result in a write-down of goodwill or intangible assets with

indefinite lives in a future period which could be material to our consolidated results of operations and financial position.

Recognition of Rebate Related to Long-Term Purchase Agreement. As part of our sale of HNS’ set-top receiver manufacturing

operations to Thomson in June 2004, DIRECTV U.S. entered into a long-term purchase agreement with Thomson for the supply

of set-top receivers. As part of this transaction, DIRECTV U.S. can earn an additional $50 million rebate from Thomson if

Thomson’s aggregate sales of DIRECTV U.S.’ set-top receivers equal at least $4 billion over the initial five year contract term

plus an additional one year optional extension period, or the Contract Term. DIRECTV U.S. has determined that, based upon

projected set-top receiver requirements, it is probable and reasonably estimable that the minimum purchase requirement will be

met for the $50 million rebate during the initial contract period. DIRECTV U.S. records a proportionate amount of the $50

million rebate as a credit to “Subscriber acquisition costs” and/or “Upgrade and retention costs” in the Consolidated Statements

of Operations upon set-top receiver activation, over the initial contract period with a corresponding entry to “Accounts

receivable, net” in the Consolidated Balance Sheets. However, DIRECTV U.S. will not be paid the $50 million rebate by

Thomson until it meets the minimum purchase requirement. DIRECTV U.S. bases its probability assessment for meeting the

minimum purchase requirement on its current and future business projections, including its belief that existing and new

subscribers will likely acquire new set-top receivers due to certain technological advances. Any negative trends in the purchase

of set-top receivers for existing and new subscribers may materially impact its ability to earn the rebate. On a quarterly basis,

DIRECTV U.S. will continue to assess whether the rebate is probable over the Contract Term. If DIRECTV U.S. subsequently

determines that it is no longer probable that it will earn the rebate, DIRECTV U.S. would be required to reverse the amount of

the credit recognized to date as a charge to the Consolidated Statements of Operations at the time such determination is made.

Financial Instruments and Investments. From time to time, we maintain investments in equity securities of unaffiliated

companies. We continually review our investments to determine whether a decline in fair value below the cost basis is “other-

than-temporary.” We consider, among other factors: the magnitude and duration of the decline; the financial health and business

outlook of the investee, including industry and sector performance, changes in technology, and operational and financing cash

flow factors; and our intent and ability to hold the investment. If we judge the decline in fair value to be other-than-temporary,

we write-down the cost basis of the security to fair value and recognize the amount in the Consolidated Statements of

Operations as part of “Other, net.” Future adverse changes in market conditions or poor operating results of underlying

investments could result in losses or an inability to recover an investment’s carrying value, thereby possibly requiring a charge

in a future period.

ACCOUNTING CHANGES

Subscriber Acquisition, Upgrade and Retention Costs. Effective January 1, 2004, we changed our method of accounting for

subscriber acquisition, upgrade and retention costs. Previously, we deferred a portion of these costs, equal to the amount of

profit to be earned from the subscriber, typically over the 12 month subscriber contract, and amortized to expense over the

contract period. We now expense all subscriber acquisition, upgrade and retention costs as incurred as subscribers activate the

DIRECTV service. We determined that expensing such costs was preferable to the prior accounting method after considering

the accounting practices of competitors and companies within similar industries and the added clarity and ease of understanding

our reported results for investors. As a result of the change, on January 1, 2004, we expensed our deferred subscriber acquisition

cost

50