Burger King 2013 Annual Report Download - page 98

Download and view the complete annual report

Please find page 98 of the 2013 Burger King annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

|

|

Table of Contents

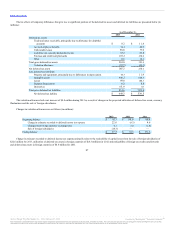

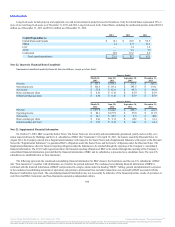

The Cap Agreements are designated as cash flow hedges and to the extent they are effective in offsetting the variability of the variable rate interest

payments, changes in the derivatives’ fair values are not included in current earnings but are included in accumulated other comprehensive income (AOCI) in

the accompanying condensed consolidated balance sheets. At each cap maturity date, the portion of the fair value attributable to the matured cap will be

reclassified from AOCI into earnings as a component of interest expense.

From time to time, as we prepay portions of the 2012 Term Loan Facility, we may modify our Cap Agreements to reduce the notional amount. The terms

of the Cap Agreements will not otherwise be revised by these modifications. On the modification date, the portion of the fair value attributable to the modified

cap will be reclassified from AOCI into earnings as a component of interest expense.

To protect the value of our investments in our foreign operations against adverse changes in foreign currency exchange rates, we may, from time to time,

hedge a portion of our net investment in one or more of our foreign subsidiaries. At December 31, 2013, we had outstanding cross-currency rate swaps with an

aggregate notional value of $430.0 million to hedge a portion of the net investment in our Switzerland subsidiary, Burger King Europe GmbH. A total notional

value of $230.0 million of these swaps are contracts to exchange quarterly fixed-rate interest payments we make in Euros for quarterly fixed-rate interest

payments we receive in U.S. dollars and mature on October 19, 2016. A total notional value of $200.0 million of these swaps are contracts to exchange

quarterly floating-rate interest payments we make in Euros based on EURIBOR for quarterly floating-rate interest payments we receive in U.S. dollars based

on LIBOR and mature on September 28, 2017. These cross-currency rate swaps also require the exchange of Euros and U.S. dollar principal payments upon

maturity. Changes in the fair value of these instruments are recognized in AOCI to offset the change in the carrying amount of the net investment being hedged.

Amounts are reclassified out of AOCI into earnings when the hedged net investment is either sold or substantially liquidated.

At December 31, 2013, we had outstanding three forward-starting interest rate swaps with a total notional value of $2.3 billion to hedge the variability of

forecasted interest payments attributable to changes in LIBOR. The forward-starting interest rate swaps effectively fix LIBOR on $1.0 billion of floating-rate

debt beginning 2015 and an additional $1.3 billion of floating-rate debt starting 2016. The hedges have a seven year maturity. We account for these hedges as

cash flow hedges, and as such, the effective portion of unrealized changes in market value has been recorded in AOCI and is reclassified to income during the

period in which the hedge transaction affects earnings. Gains and losses from hedge ineffectiveness are recognized in current earnings.

From time to time, we enter into foreign currency forward contracts to economically hedge the remeasurement of certain foreign currency-denominated

intercompany loans receivable and other foreign-currency denominated assets recorded in our consolidated balance sheets. The forward currency forward

contracts are not designated as hedging instruments. Gains and losses on foreign currency forward contracts are recognized in other (income) expense, net and

are offset by the gains or losses resulting from the settlement of the underlying foreign currency denominated assets and liabilities. At December 31, 2013, we

had no outstanding foreign currency forward contracts.

By entering into derivative instrument contracts, we are exposed to counterparty credit risk. Counterparty credit risk is the failure of the counterparty to

perform under the terms of the derivative contract. When the fair value of a derivative contract is in an asset position, the counterparty has a liability to us,

which creates credit risk for us. We attempt to minimize this risk by selecting counterparties with investment grade credit ratings and regularly monitoring our

market position with each counterparty.

Our derivative instruments do not contain any credit-risk related contingent features.

96

Source: Burger King Worldwide, Inc., 10-K, February 21, 2014 Powered by Morningstar® Document Research℠

The information contained herein may not be copied, adapted or distributed and is not warranted to be accurate, complete or timely. The user assumes all risks for any damages or losses arising from any use of this

information, except to the extent such damages or losses cannot be limited or excluded by applicable law. Past financial performance is no guarantee of future results.