Avon 2014 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2014 Avon annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

|

|

PART II

Foreign Currency Risk

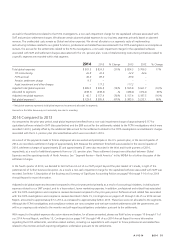

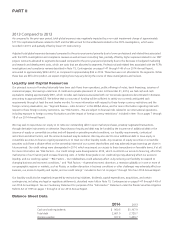

We conduct business globally, with operations in various locations around the world. Over the past three years, approximately 87% of our

consolidated revenue was derived from operations of subsidiaries outside of the United States (“U.S”). The functional currency for most of

our foreign operations is their local currency. We are exposed to changes in financial market conditions in the normal course of our

operations, primarily due to international businesses and transactions denominated in foreign currencies and the use of various financial

instruments. We are not able to project, in any meaningful way, the possible effect of these foreign currency fluctuations on translated

amounts or future earnings. At December 31, 2014, the primary foreign currencies for which we had net underlying foreign currency

exchange rate exposures were the Argentine peso, Brazilian real, British pound, Canadian dollar, Chilean peso, Colombian peso, the euro,

Mexican peso, Peruvian new sol, Philippine peso, Polish zloty, Romanian leu, Russian ruble, South Africa rand, Turkish lira, Ukrainian hryvna

and Venezuelan bolívar.

We may reduce our exposure to fluctuations in cash flows associated with changes in foreign exchange rates by creating offsetting

positions, including through the use of derivative financial instruments. Our hedges of our foreign currency exposure are not designed to,

and, therefore, cannot entirely eliminate the effect of changes in foreign exchange rates on our consolidated financial position, results of

operations and cash flows.

Our foreign-currency financial instruments were analyzed at year-end to determine their sensitivity to foreign exchange rate changes. Based

on our outstanding foreign exchange contracts at December 31, 2014, the impact of a hypothetical 10% appreciation or 10% depreciation

of the U.S. dollar against our foreign exchange contracts would not represent a material potential change in fair value, earnings or cash

flows. This potential change does not consider our underlying foreign currency exposures. The hypothetical impact was calculated on the

open positions using forward rates at December 31, 2014, adjusted for an assumed 10% appreciation or 10% depreciation of the U.S.

dollar against these hedging contracts.

Credit Risk of Financial Instruments

We attempt to minimize our credit exposure to counterparties by entering into derivative transactions and similar agreements with major

international financial institutions with “A” or higher credit ratings as issued by Standard & Poor’s Corporation. Our foreign currency and

interest-rate derivatives are comprised of over-the-counter forward contracts, swaps or options with major international financial institutions.

Although our theoretical credit risk is the replacement cost at the then estimated fair value of these instruments, we believe that the risk of

incurring credit risk losses is remote and that such losses, if any, would not be material.

Non-performance of the counterparties on the balance of all the foreign exchange agreements would have resulted in a write-off of $.6 at

December 31, 2014. In addition, in the event of non-performance by such counterparties, we would be exposed to market risk on the

underlying items being hedged as a result of changes in foreign exchange rates.

See Note 8, Financial Instruments and Risk Management on pages F-25 through F-27 of our 2014 Annual Report for more information.

ITEM 8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA

Reference is made to the Index on page F-1 of our Consolidated Financial Statements and Notes thereto contained herein.

ITEM 9. CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON

ACCOUNTING AND FINANCIAL DISCLOSURE

Not applicable.

ITEM 9A. CONTROLS AND PROCEDURES

Evaluation of Disclosure Controls and Procedures

As of the end of the period covered by this report, our principal executive and principal financial officers carried out an evaluation of the

effectiveness of the design and operation of our disclosure controls and procedures pursuant to Rule 13a-15 of the Securities Exchange Act

of 1934, as amended (the “Exchange Act”). In designing and evaluating our disclosure controls and procedures, management recognizes

that any controls and procedures, no matter how well designed and operated, can provide only reasonable assurance of achieving the