Avon 2014 Annual Report Download - page 109

Download and view the complete annual report

Please find page 109 of the 2014 Avon annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

|

|

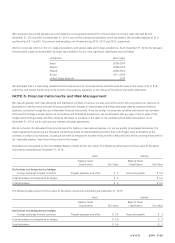

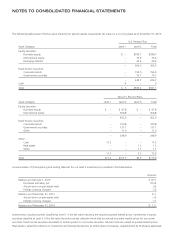

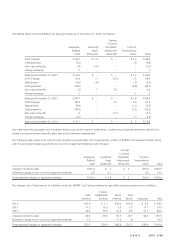

The U.S. pension plans include a funded qualified plan and unfunded non-qualified plans. As of December 31, 2014, the U.S. qualified

pension plan had benefit obligations of $673.1 and plan assets of $506.5. As of December 31, 2013, the U.S. qualified pension plan had

benefit obligations of $624.1 and plan assets of $531.1. We believe we have adequate investments and cash flows to fund the liabilities

associated with the unfunded non-qualified plans.

Components of Net Periodic Benefit Cost and Other Amounts Recognized in Other

Comprehensive Loss

Pension Benefits

Postretirement BenefitsU.S. Plans Non-U.S. Plans

2014 2013 2012 2014 2013 2012 2014 2013 2012

Net Periodic Benefit Cost:

Service cost $ 14.1 $ 15.7 $ 15.1 $ 8.5 $ 12.2 $ 18.0 $ 1.1 $ 1.8 $ 1.9

Interest cost 27.8 27.5 29.6 36.5 36.8 39.8 4.9 5.1 5.8

Expected return on plan assets (35.8) (37.4) (36.0) (43.3) (40.7) (39.1) – – –

Amortization of prior service credit (.3) (.3) (.3) (.1) (.2) (1.3) (4.5) (4.8) (13.2)

Amortization of net actuarial losses 45.1 47.2 43.7 9.8 12.8 17.6 1.4 2.5 4.1

Settlements/curtailments 38.0 – .8 2.7 (4.3) 1.9 (2.7) (1.8) (1.0)

Other – – – .6 .7 .7 – – –

Net periodic benefit cost $ 88.9 $ 52.7 $ 52.9 $ 14.7 $ 17.3 $ 37.6 $ .2 $ 2.8 $ (2.4)

Other Changes in Plan Assets and

Benefit Obligations Recognized in

Other Comprehensive (Loss) Income:

Actuarial losses (gains) $105.9 $ (80.8) $ 37.7 $ 99.2 $(14.8) $ 31.0 $ 3.6 $(22.9) $ 4.7

Prior service (credit) cost (2.0) – – – – 4.8 – (1.3) –

Amortization of prior service credit .3 .3 .3 .1 7.9 2.4 7.3 7.1 14.6

Amortization of net actuarial losses (81.5) (47.2) (43.7) (13.1) (17.7) (21.8) (1.7) (3.4) (4.1)

Foreign currency changes – – – (31.3) .5 10.4 (.1) (.2) (.2)

Total recognized in other comprehensive (loss)

income*

$ 22.7 $(127.7) $ (5.7) $ 54.9 $(24.1) $ 26.8 $ 9.1 $(20.7) $15.0

Total recognized in net periodic benefit cost

and other comprehensive (loss) income $111.6 $ (75.0) $ 47.2 $ 69.6 $ (6.8) $ 64.4 $ 9.3 $(17.9) $12.6

* Amounts represent the pre-tax effect included within other comprehensive (loss) income. The net of tax amounts are included within the Consolidated

Statements of Comprehensive Income.

In an effort to reduce our pension benefit obligations, in March 2014, we offered former employees who are vested and participate in the

PRA a payment that would fully settle our pension plan obligation to those participants who elected to receive such payment. The election

period ended during the second quarter of 2014 and the payments were made in June 2014 from our plan assets. As a result of the lump-

sum payments made, in the second quarter of 2014, we recorded a settlement charge of $23.5. Because the settlement threshold was

exceeded in the second quarter of 2014, settlement charges of $5.4 and $7.5 were also recorded in the third and fourth quarters of 2014,

respectively, as a result of additional payments from the PRA. These settlement charges were allocated between Global Expenses and the

operating results of North America.

The amounts in AOCI that are expected to be recognized as components of net periodic benefit cost during 2015 are as follows:

Pension Benefits Postretirement

BenefitsU.S. Plans Non-U.S. Plans

Net actuarial loss $46.4 $11.4 $ 2.1

Prior service credit (.7) (.1) (4.1)

A V O N 2014 F-35