Avon 2014 Annual Report Download - page 30

Download and view the complete annual report

Please find page 30 of the 2014 Avon annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

|

|

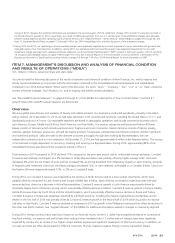

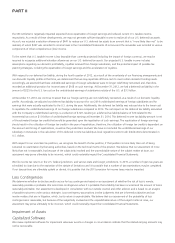

PART II

Impact on Operating Profit

2014 2013 2012 2011 2010

Costs to implement restructuring initiatives related to our

cost savings initiative, multi-year restructuring programs,

and other restructuring initiatives $114.2 $ 65.9 $124.7 $40.0 $80.7

Venezuelan special items(2) 137.1 49.6 – – 79.5

FCPA accrual(3) 46.0 89.0 – – –

Pension settlement charge(4) 36.4 – – – –

Asset impairment and other charges(5) – 159.3 44.0 – –

In addition to the items impacting operating profit identified above, loss from continuing operations, net of tax during 2014 was negatively impactedbya

non-cash income tax charge of $404.9. This was primarily due to a valuation allowance of $383.5 to reduce our deferred tax assets to an amount that is

“more likely than not” to be realized, which was recorded in the fourth quarter of 2014. In addition, loss from continuing operations, net of tax during 2014

was favorably impacted by the $18.5 net tax benefit recorded in the fourth quarter of 2014 related to the finalization of the Foreign Corrupt Practices Act

(“FCPA”) settlements. See Note 7, Income Taxes on pages F-21 through F-25 of our 2014 Annual Report, for more information.

In addition to the items impacting operating profit identified above, loss from continuing operations, net of tax during 2013 was impacted by a loss on

extinguishment of debt of $73.0 before tax ($46.2 after tax) in the first quarter of 2013 caused by the make-whole premium and the write-off of debt

issuance costs associated with the prepayment of our Private Notes (as defined in “Capital Resources” within MD&A on pages 55 through 57), as well as the

write-off of debt issuance costs associated with the early repayment of $380 of the outstanding principal amount of the term loan agreement (as definedin

“Capital Resources” within MD&A on pages 55 through 57). Loss from continuing operations, net of tax during 2013 was also impacted by a loss on

extinguishment of debt of $13.0 before tax ($8.2 after tax) in the second quarter of 2013 caused by the make-whole premium and the write-off of debt

issuance costs and discounts, partially offset by a deferred gain associated with the January 2013 interest-rate swap agreement termination, associated with

the prepayment of the 2014 Notes (as defined in “Capital Resources” within MD&A on pages 55 through 57). In addition, loss from continuing operations,

net of tax during 2013 was impacted by valuation allowances for deferred tax assets of $41.8 related to Venezuela and $9.2 related to China. See Note 5,

Debt and Other Financing on pages F-17 through F-20 of our 2014 Annual Report, “Results Of Operations – Consolidated” within MD&A on pages 33

through 40, and Note 7, Income Taxes on pages F-21 through F-25 of our 2014 Annual Report for more information.

In addition to the items impacting operating profit identified above, income from continuing operations, net of tax during 2012 was impacted by a benefit

recorded to other expense, net of $23.8 before tax ($15.7 after tax) due to the release of a provision in the fourth quarter associated with the excess cost of

acquiring U.S. dollars in Venezuela at the regulated market rate as compared with the official exchange rate. This provision was released as the Company

capitalized the associated intercompany liabilities. Also, during the fourth quarter of 2012, we determined that the Company may repatriate offshore cash to

meet certain domestic funding needs. Accordingly, we are no longer asserting that the undistributed earnings of foreign subsidiaries are indefinitely

reinvested, and therefore, we recorded an additional provision for income taxes of $168.3. See “Results Of Operations – Consolidated” within MD&A on

pages 33 through 40, and Note 7, Income Taxes on pages F-21 through F-25 of our 2014 Annual Report for more information.

(2) During 2014, 2013 and 2010, our operating profit and operating margin were negatively impacted by the devaluation of the Venezuelan currency, and in

2010 this was coupled with a required change to account for operations in Venezuela on a highly inflationary basis.

In February 2014, the Venezuelan government announced a foreign exchange system (“SICAD II”) and we concluded that we should utilize the SICAD II

exchange rate to remeasure our Venezuelan operations effective March 31, 2014. At March 31, 2014, the SICAD II exchange rate was approximately 50, as

compared to the official exchange rate of 6.30 that we used previously, which caused the recognition of a devaluation of approximately 88%. As a result of

using the historical United States (“U.S.”) dollar cost basis of non-monetary assets, such as inventories, these assets continued to be remeasured, following

the change to the SICAD II rate, at the applicable rate at the time of acquisition. As a result, we determined that an adjustment of $115.7 to cost of sales was

needed to reflect certain non-monetary assets at their net realizable value, which was recorded in the first quarter of 2014. In 2014, we recognized an

additional negative impact of $21.4 to operating profit relating to these non-monetary assets. In addition to the negative impact to operating profit, as a

result of the devaluation of Venezuelan currency, during 2014, we recorded an after-tax loss of $41.8 ($53.7 in other expense, net, and a benefit of $11.9 in

income taxes), primarily reflecting the write-down of monetary assets and liabilities.

In 2013, as a result of using the historical U.S. dollar cost basis of non-monetary assets, such as inventories, acquired prior to the devaluation, 2013 operating

profit was negatively impacted by $49.6, due to the difference between the historical U.S. dollar cost at the previous official exchange rate of 4.30 and the

official exchange rate of 6.30. In addition to the negative impact to operating profit, as a result of the devaluation of Venezuelan currency, during 2013, we

recorded an after-tax loss of $50.7 ($34.1 in other expense, net, and $16.6 in income taxes), primarily reflecting the write-down of monetary assets and

liabilities and deferred tax benefits.

In 2010, as a result of using the historical U.S. dollar cost basis of non-monetary assets, such as inventories, acquired prior to the devaluation, during 2010

operating profit was negatively impacted by $79.5 for the difference between the historical U.S. dollar cost at the previous official exchange rate of 2.15 and

the official exchange rate of 4.30. In addition to the negative impact to operating profit, as a result of the devaluation of Venezuelan currency, during 2010,

we recorded an after-tax loss of $58.8 ($46.1 in other expense, net, and $12.7 in income taxes), primarily reflecting the write-down of monetary assets and

liabilities and deferred tax benefits.

See discussion of Venezuela in “Segment Review – Latin America” within MD&A on pages 40 through 45 for more information.

(3) During 2014, our operating profit and operating margin were negatively impacted by the additional $46 accrual, and during 2013, our operating profit and

operating margin were negatively impacted by the $89 accrual, both recorded for the settlements related to the FCPA investigations. See Note 15,

Contingencies on pages F-47 through F-49 of our 2014 Annual Report for more information.

(4) During 2014, our operating profit and operating margin were negatively impacted by settlement charges associated with the U.S. pension plan. As a result of

the payments made to former employees who are vested and participate in the U.S. pension plan, in the second quarter of 2014, we recorded a settlement