Avon 2014 Annual Report Download - page 51

Download and view the complete annual report

Please find page 51 of the 2014 Avon annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

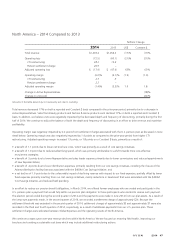

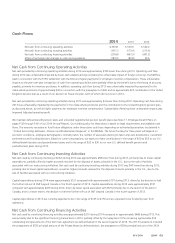

|

|

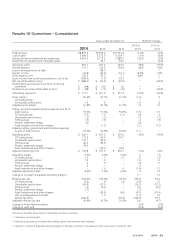

2014. We recognized an additional negative impact of approximately $21 to operating profit and net income relating to these non-

monetary assets in the second, third and fourth quarters of 2014. In addition, at March 31, 2014, we reviewed Avon Venezuela’s long-lived

assets to determine whether the carrying amount of the assets were recoverable, and determined that they were. As such, no impairment of

Avon Venezuela’s long-lived assets was required; however, further devaluations or regulatory actions may impair the carrying value of Avon

Venezuela’s long-lived assets, which was approximately $107 at December 31, 2014.

At December 31, 2014, we had a net asset position of $100 associated with our operations in Venezuela, which included cash balances of

approximately $4, of which approximately $3 was denominated in Bolívares. Of the $100 net asset position, a net liability of approximately

$5 was associated with Bolívar-denominated monetary net assets. During 2014, Avon Venezuela (using the 6.30 exchange rate for the first

quarter and the SICAD II rate beginning in the second quarter) represented approximately 2% of Avon’s consolidated revenue and 3% of

Avon’s consolidated Adjusted operating profit. If we had remeasured Avon Venezuela’s income statement at the SICAD II rate of

approximately 50 for the entire year ended December 31, 2014, Avon Venezuela would have represented approximately 1% of Avon’s

consolidated revenue and approximately 1% of Avon’s consolidated Adjusted operating profit.

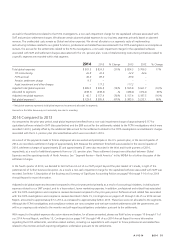

There also could be ongoing impacts primarily related to the remeasurement of Avon Venezuela’s financial statements. To illustrate our

sensitivity to potential future changes in the foreign exchange rates in Venezuela, if we were to utilize an exchange rate of approximately

170 Bolívares to the U.S. dollar to remeasure our Venezuelan operations as of December 31, 2014 (a devaluation of approximately 70%

from the exchange rate of approximately 50), and using 2014 results, Avon’s annualized consolidated results would be negatively impacted

as follows:

• As a result of the use of a further devalued exchange rate for the remeasurement of Avon Venezuela’s revenues and profits, Avon’s

annualized consolidated revenues would likely be negatively impacted by approximately 1% and annualized consolidated Adjusted

operating profit would likely be negatively impacted by approximately 1% prospectively, assuming no operational improvements occurred

to offset the negative impact of a further devaluation.

• Avon’s consolidated Adjusted operating profit during the first twelve months following the devaluation would likely be negatively

impacted by approximately 5%, assuming no offsetting operational improvements or any impairment of Avon Venezuela’s long-lived

assets. The larger negative impact on Adjusted operating profit during the first twelve months as compared to the prospective impact is

caused by costs of non-monetary assets, primarily inventories, being carried at their historical U.S. dollar cost in accordance with the

requirement to account for Venezuela as a highly inflationary economy while revenue would be remeasured at the further devalued rate.

• We would likely incur an immediate benefit of approximately $3 (primarily in other expense, net) associated with the net liability of

Bolívar-denominated monetary net assets.

In 2014, the Venezuelan government also issued a Law on Fair Pricing, establishing a maximum profit margin. During 2014, this law did not

have a significant effect on Avon Venezuela’s results; however, it is uncertain how this law may be interpreted and enforced in the future.

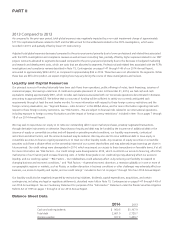

Argentina Discussion

In late 2011, the Argentine government introduced restrictive foreign currency exchange controls. Unless foreign exchange is made more

readily available at the official exchange rate, Avon Argentina’s operations may be negatively impacted. At December 31, 2014, we had a

net asset position of approximately $91 associated with our operations in Argentina. During 2014, Avon Argentina represented

approximately 4% of Avon’s consolidated revenue and approximately 6% of Avon’s consolidated Adjusted operating profit.

To illustrate our sensitivity to potential future changes in the exchange rate in Argentina, if the exchange rate was devalued by

approximately 50% from the average exchange rate of Argentina’s 2014 results, and using 2014 results, Avon’s annualized consolidated

revenues would likely be negatively impacted by approximately 2% and annualized consolidated Adjusted operating profit would likely be

negatively impacted by approximately 4% prospectively. This sensitivity analysis was performed assuming no operational improvements

occurred to offset the negative impact of a devaluation.

As of December 31, 2014, we did not account for Argentina as a highly inflationary economy. As a result, any potential devaluation would

not negatively impact earnings with respect to Argentina’s monetary and non-monetary assets.

A V O N 2014 43