Avon 2014 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2014 Avon annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

|

|

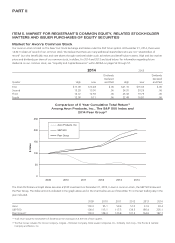

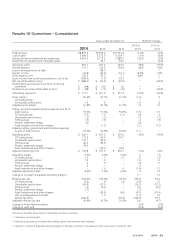

PART II

the SEC settlement, negatively impacted expected future repatriation of foreign earnings and reduced current U.S. taxable income,

respectively. As a result of these developments, we may not generate sufficient taxable income to realize all of our U.S. deferred tax assets.

As such, we recorded a valuation allowance of $441 to reduce our U.S. deferred tax assets to an amount that is “more likely than not” to be

realized, of which $367 was recorded to income taxes in the Consolidated Statements of Income and the remainder was recorded to various

components of other comprehensive (loss) income.

To the extent that U.S. taxable income is less favorable than currently projected (including the impact of foreign currency), we may be

required to recognize additional valuation allowances on our U.S. deferred tax assets. Our projected U.S. taxable income includes

assumptions regarding our domestic profitability, royalties received from foreign subsidiaries, and the potential impact of possible tax

planning strategies, including the repatriation of foreign earnings and the acceleration of royalties.

With respect to our deferred tax liability, during the fourth quarter of 2012, as a result of the uncertainty of our financing arrangements and

our domestic liquidity profile at that time, we determined that we may repatriate offshore cash to meet certain domestic funding needs.

Accordingly, we asserted that these undistributed earnings of foreign subsidiaries were no longer indefinitely reinvested and, therefore,

recorded an additional provision for income taxes of $168 on such earnings. At December 31, 2012, we had a deferred tax liability in the

amount of $225 for the U.S. tax cost on the undistributed earnings of subsidiaries outside of the U.S. of $3.1 billion.

At December 31, 2014, we continue to assert that our foreign earnings are not indefinitely reinvested, as a result of our domestic liquidity

profile. Accordingly, we adjusted our deferred tax liability to account for our 2014 undistributed earnings of foreign subsidiaries and for

earnings that were actually repatriated to the U.S. during the year. Additionally, the deferred tax liability was reduced due to the lower cost

to repatriate the undistributed earnings of our foreign subsidiaries compared to 2013. The net impact on the deferred tax liability associated

with the Company’s undistributed earnings is a reduction of $129, resulting in a deferred tax liability balance of $14 related to the

incremental tax cost on $1.9 billion of undistributed foreign earnings at December 31, 2014. This deferred income tax liability amount is net

of the estimated foreign tax credits that would be generated upon the repatriation of such earnings. The repatriation of foreign earnings

should result in the utilization of foreign tax credits in the year of repatriation; therefore, the utilization of foreign tax credits is dependent on

the amount and timing of repatriations, as well as the jurisdictions involved. We have not included the undistributed earnings of our

subsidiary in Venezuela in the calculation of this deferred income tax liability as local regulations restrict cash distributions denominated in

U.S. dollars.

With respect to our uncertain tax positions, we recognize the benefit of a tax position, if that position is more likely than not of being

sustained on examination by the taxing authorities, based on the technical merits of the position. We believe that our assessment of more

likely than not is reasonable, but because of the subjectivity involved and the unpredictable nature of the subject matter at issue, our

assessment may prove ultimately to be incorrect, which could materially impact the Consolidated Financial Statements.

We file income tax returns in the U.S. federal jurisdiction, and various state and foreign jurisdictions. In 2015, a number of open tax years are

scheduled to close due to the expiration of the statute of limitations and it is possible that a number of tax examinations may be completed.

If our tax positions are ultimately upheld or denied, it is possible that the 2015 provision for income taxes may be impacted.

Loss Contingencies

We determine whether to disclose and/or accrue for loss contingencies based on an assessment of whether the risk of loss is remote,

reasonably possible or probable. We record loss contingencies when it is probable that a liability has been incurred and the amount of loss is

reasonably estimable. Our assessment is developed in consultation with our outside counsel and other advisors and is based on an analysis

of possible outcomes under various strategies. Loss contingency assumptions involve judgments that are inherently subjective and can

involve matters that are in litigation, which, by its nature is unpredictable. We believe that our assessment of the probability of loss

contingencies is reasonable, but because of the subjectivity involved and the unpredictable nature of the subject matter at issue, our

assessment may prove ultimately to be incorrect, which could materially impact the Consolidated Financial Statements.

Impairment of Assets

Capitalized Software

We review capitalized software for impairment whenever events or changes in circumstances indicate that the related carrying amounts may

not be recoverable.