Avon 2013 Annual Report Download - page 86

Download and view the complete annual report

Please find page 86 of the 2013 Avon annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

|

|

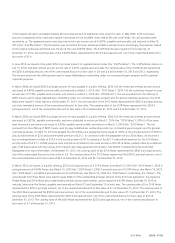

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

2012 Silpada Impairment Assessment

In the fourth quarter of 2012, we completed the annual goodwill and indefinite-lived intangible assets impairment assessments and

subsequently determined that the goodwill, indefinite-lived trademark and finite-lived customer relationships associated with Silpada were

impaired. As a result, the carrying amount of Silpada’s goodwill was reduced from $116.7 to its estimated fair value of $44.6, resulting in a

non-cash impairment charge of $72.1. In addition, the carrying amount of Silpada’s indefinite-lived trademark was reduced from $85.0 to its

estimated fair value of $40.0, resulting in a non-cash impairment charge of $45.0, and the carrying amount of Silpada’s finite-lived customer

relationships was reduced from $131.9 to its estimated fair value of $40.0, resulting in a non-cash impairment charge of $91.9.

Throughout the first nine months of 2012, Silpada continued to perform generally in line with our revenue and earnings forecast and there

were no significant changes to our long-term outlook for the business, which was utilized in determining the estimated fair value in our

2011 impairment analysis. Our revenue and earnings forecast for 2012 had projected improvements to the trends (i.e., a reduction of the

year-over-year revenue declines) in the latter portion of 2012. In 2012, in an effort to promote sales and grow the business, we made

changes to certain members of the Silpada management team, including bringing in personnel who had previously managed other Avon

businesses. Among the initiatives implemented by the new Silpada management team was a recruiting incentive program which we had

believed would benefit our Representative counts and Representative productivity primarily in the latter portion of 2012, and in turn improve

the performance of the business. While we saw improvement in our Representative additions, the recruiting incentive program did not result

in the expected Representative productivity.

In the fourth quarter of 2012, which is generally the quarter with the largest dollar value of revenue for the Silpada business, it became

apparent that we would not achieve our forecasted revenue and earnings for 2012, partially due to the recruiting incentive program not

driving the expected Representative productivity, and as a result, Silpada experienced weaker than expected performance in the fourth

quarter of 2012. The revenue performance in the fourth quarter of 2012 was approximately 19% less than the estimates utilized in our

2011 impairment analysis. Based on these continued trends, in the latter part of the fourth quarter of 2012, in conjunction with the 2013

planning process and the early stages of our evaluation of strategic alternatives for the business, we lowered our long-term revenue and

earnings projections for Silpada in our DCF model to reflect a more moderate recovery of the business. The more moderate recovery of the

business was believed to be appropriate due to the lack of sales momentum in the business and the continued inability of Silpada to achieve

our financial performance expectations.

The decline in the fair values of the Silpada reporting unit, the trademark, and the customer relationships was primarily driven by the

reduction in the forecasted long-term growth rates and cash flows used to estimate fair value. The lower than expected financial results for

fiscal year 2012 served as the baseline for the long-term projections of the business. Fiscal year 2012 revenue for Silpada was approximately

10% less than the estimates utilized in our 2011 impairment analysis and 19% less than fiscal year 2011 results. We forecasted revenue and

the resulting cash flows over ten years using a DCF model which included a terminal value at the end of the projection period.

2011 Silpada Impairment Assessment

During our year-end 2011 close process, we completed our annual goodwill impairment assessment and subsequently determined that the

goodwill associated with Silpada was impaired. As a result of our impairment testing, we recorded a non-cash before tax impairment charge

of $198.0 to reduce the carrying amount of goodwill for Silpada to its estimated fair value. Following the impairment charge, the carrying

value of the Silpada goodwill was $116.7.

Our impairment testing for indefinite-lived intangible assets also indicated a decline in the fair value of our Silpada trademark intangible

asset below its respective carrying value. This resulted in a non-cash before tax impairment charge of $65.0 to reduce the carrying amount

of this asset to its estimated fair value. Following the impairment charge, the carrying value of the Silpada trademark was $85.0.

Following weaker than expected performance in the fourth quarter of 2011, we lowered our revenue and earnings projections for Silpada

largely due to the rise in silver prices, which nearly doubled since the acquisition, and the negative impact of pricing on revenues and

margins. The decline in the fair values of the Silpada reporting unit and the underlying trademark was driven by the reduction in the

forecasted growth rates and cash flows used to estimate fair value. We forecasted revenue and the resulting cash flows over ten years using

a DCF model which included a terminal value at the end of the projection period.

Avon Japan

On November 8, 2010, the Company announced that Avon International Operations, Inc. (“AIO”), a wholly-owned subsidiary of the

Company, had agreed to sell the ownership interest in Avon Products Company Limited (“Avon Japan”) held by AIO pursuant to a tender