Avon 2013 Annual Report Download - page 47

Download and view the complete annual report

Please find page 47 of the 2013 Avon annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

|

|

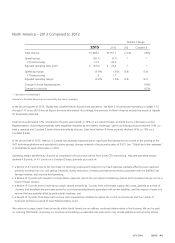

• a benefit of 1.9 points due to higher gross margin caused primarily by 1.5 points from the favorable net impact of mix and pricing.

Benefits from pricing include the realization of price increases in advance of costs in markets experiencing relatively high inflation

(Venezuela and Argentina), while mix negatively impacted gross margin due to higher growth in Fashion & Home. In addition, there were

various other insignificant items that favorably impacted gross margin. These items were partially offset by .6 points from the unfavorable

impact of foreign exchange; and

• a decline of .5 points from higher transportation costs, primarily in Venezuela.

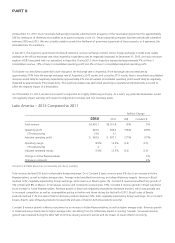

Currency restrictions enacted by the Venezuelan government in 2003 have impacted the ability of Avon Venezuela to obtain foreign

currency at the official rate to pay for imported products. Since 2003, Avon Venezuela had been obtaining its foreign currency needs beyond

the amounts that could be obtained at official rates through non-government sources where the exchange rates were less favorable than

the official rate (“parallel market”). In late May 2010, the Venezuelan government took control over the previously freely-traded parallel

market, by implementing a regulated (“SITME”) market in early June 2010. The SITME market was eliminated in February 2013 in

conjunction with the government’s devaluation of its currency as described below. In March 2013, the government announced a foreign

exchange system (“SICAD”) that increases government control over the allocation of U.S. dollars in the country. The availability of U.S.

dollars under the SICAD market for Avon has been limited to-date. We are still evaluating our future access to funds through the SICAD or

other similar markets.

We account for Venezuela as a highly inflationary economy. Effective February 13, 2013, the official exchange rate moved from 4.30 to

6.30, a devaluation of 32%. As a result of the change in the official rate to 6.30, we recorded a one-time, after-tax loss of $51 ($34 in other

expense, net and $17 in income taxes) in the first quarter of 2013, primarily reflecting the write-down of monetary assets and liabilities and

deferred tax benefits. Additionally, certain non-monetary assets are carried at the U.S. historic dollar cost subsequent to the devaluation.

Therefore, these costs impacted the income statement during 2013 at a disproportionate rate as they were not devalued based on the new

exchange rates, but were expensed at their U.S. historic dollar value. As a result of using the U.S. historic dollar cost basis of non-monetary

assets, such as inventory, acquired prior to the devaluation, 2013 operating profit and net income were negatively impacted by $50, due to

the difference between the historical cost at the previous official exchange rate of 4.30 and the new official exchange rate of 6.30. Results

for periods prior to 2013 were not impacted by the change in the official rate in February of 2013.

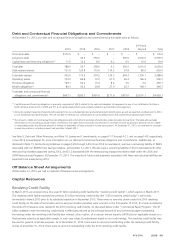

At December 31, 2013, we had a net asset position of $252 associated with our operations in Venezuela, which included cash balances of

$136, of which approximately $135 was denominated in Bolívares remeasured at the December 31, 2013 official exchange rate of 6.30. Of

the $252 net asset position, approximately $92 was associated with Bolívar-denominated monetary net assets and prepaid income taxes.

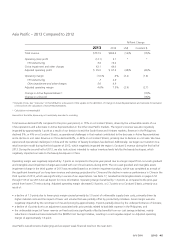

During 2013, Avon Venezuela represented approximately 5% of Avon’s consolidated revenue and 7% of Avon’s consolidated Adjusted

operating profit. The costs associated with acquiring goods that required settlement in U.S. dollars included within Venezuela’s operating

profit were not significant during 2013, and were approximately $18 during 2012.

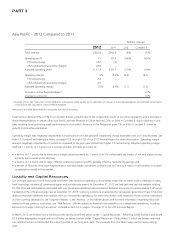

To illustrate our sensitivity to potential future changes in the official exchange rate in Venezuela, if the official exchange rate was further

devalued by 50% as of December 31, 2013, or from the official rate of 6.3 to a rate of 12.6 Bolívares to the U.S. dollar, our results would be

negatively impacted as follows:

• As a result of the use of a further devalued exchange rate for the remeasurement of Avon Venezuela’s revenues and profits, Avon’s

annualized consolidated revenues would likely be negatively impacted by approximately 2% and annualized consolidated operating profit

would likely be negatively impacted by approximately 3% prospectively, assuming no operational improvements occurred to offset the

negative impact of a further devaluation.

• Avon’s consolidated operating profit during the first twelve months following the devaluation, in this example, would likely be negatively

impacted by approximately 11%, assuming no offsetting operational improvements. The larger negative impact on operating profit during

the first twelve months as compared to the prospective impact is caused by costs of non-monetary assets being carried at historical dollar

cost in accordance with the requirement to account for Venezuela as a highly inflationary economy while revenue would be remeasured

at the further devalued rate.

• We would likely incur an immediate charge of approximately $37 (a charge of approximately $42 in other expense, net and a benefit of

approximately $5 in income taxes) associated with the $92 of Bolívar-denominated monetary net assets and prepaid income taxes.

Additionally, if an alternative source of exchange, which may include the SICAD market, were to become widely available at 12.6 Bolívares to

the U.S. dollar, which would represent a 50% devaluation from the official exchange rate for the existing U.S. dollar-denominated liabilities, as

of December 31, 2013, we would likely incur an immediate charge of approximately $2, and may also incur higher ongoing costs.

A V O N 2013 39