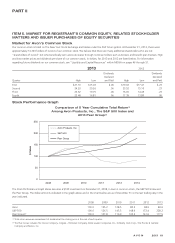

Avon 2013 Annual Report Download - page 35

Download and view the complete annual report

Please find page 35 of the 2013 Avon annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

|

|

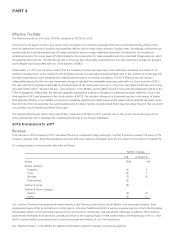

Taxes

At December 31, 2013, we had net deferred tax assets of $1,144 (net of valuation allowances of $783).

With respect to our deferred tax assets, at December 31, 2013, we had recognized deferred tax assets relating to tax loss carryforwards of

$756, primarily from foreign jurisdictions, for which a valuation allowance of $718 has been provided. We also had recognized deferred tax

assets of $585 relating to excess foreign tax credit carryforwards of which $57, $44, $54, $124, $79 and $227 expire at the end of 2018,

2019, 2020, 2021, 2022 and 2023, respectively. We have a history of domestic source losses and our excess foreign tax credits have

primarily resulted from having a greater domestic source loss in recent years which reduces foreign source income. During 2013, our

domestic source loss included the tax losses generated from the sale of our Silpada business and our losses on extinguishment of debt,

which led to an increase in our excess foreign tax credit carryforwards generated in 2013, which expire in 2023. Our ability to utilize these

foreign tax credits is dependent on future U.S. taxable income. At December 31, 2013, we would need to generate approximately $1.7

billion of excess net foreign source income in order to realize the deferred tax assets. There are a number of variables to consider in

determining the projected realization of excess foreign tax credits including the amount of any domestic source loss and the type, jurisdiction

and timing of any foreign source income. Based on our projections, we estimate that it will take several years to generate sufficient excess

net foreign source income to realize these excess foreign tax credits, which expire 10 years after being created.

We record a valuation allowance to reduce our deferred tax assets to an amount that is “more likely than not” to be realized. Evaluating the

need for and quantifying the valuation allowance often requires significant judgment and extensive analysis of all the weighted positive and

negative evidence available to the Company in order to determine whether all or some portion of the deferred tax assets will not be realized.

In performing this analysis, the Company’s forecasted domestic and foreign taxable income and the existence of potential prudent and

feasible tax planning strategies that would enable the Company to utilize some or all of its excess foreign tax credits were taken into

consideration.

As a result of this analysis, we have concluded that the tax benefits associated with the excess foreign tax credits are “more likely than not”

to be realized prior to expiration. Our conclusion is based on forecasted future U.S. taxable income, including domestic profitability, royalties

received from foreign subsidiaries, and the potential impact of possible tax planning strategies, including the repatriation of foreign earnings

and the acceleration of royalties. Assumptions embedded in our forecasted future U.S. taxable income include continued international

growth, the stabilization of the U.S. business and the reduction of corporate expenses. To the extent U.S. taxable income is less favorable

than currently projected, our ability to utilize these foreign tax credits may be negatively affected.

With respect to our deferred tax liability, during the fourth quarter of 2012, as a result of the uncertainty of our financing arrangements and

our domestic liquidity profile at that time, we determined that we may repatriate offshore cash to meet certain domestic funding needs.

Accordingly, we asserted that these undistributed earnings of foreign subsidiaries were no longer indefinitely reinvested and, therefore,

recorded an additional provision for income taxes of $168 on such earnings. At December 31, 2012, we had a deferred tax liability in the

amount of $225 for the U.S. tax cost on the undistributed earnings of subsidiaries outside of the U.S. of $3.1 billion.

At December 31, 2013, we continue to assert that our undistributed earnings of foreign subsidiaries are not indefinitely reinvested, as a

result of our domestic liquidity profile. Accordingly, we adjusted our deferred tax liability to account for our 2013 undistributed earnings of

foreign subsidiaries and for earnings that were actually repatriated to the U.S. during the year. Additionally, the deferred tax liability was

reduced due to the lower cost to repatriate the undistributed earnings of our foreign subsidiaries compared to 2012. The net impact on the

deferred tax liability associated with the Company’s undistributed earnings is a reduction of $82, resulting in a deferred tax liability balance

of $143 related to the incremental U.S. tax cost on $2.6 billion of undistributed foreign earnings at December 31, 2013. This deferred

income tax liability amount is net of the estimated foreign tax credits that would be generated upon the repatriation of such earnings. The

repatriation of foreign earnings should result in the utilization of foreign tax credits in the year of repatriation; therefore, the utilization of

foreign tax credits is dependent on the amount and timing of repatriations, as well as the jurisdictions involved. We have not included the

undistributed earnings of our subsidiary in Venezuela in the calculation of this deferred income tax liability as local regulations restrict cash

distributions denominated in U.S. dollars.

With respect to our uncertain tax positions, we recognize the benefit of a tax position, if that position is more likely than not of being

sustained on examination by the taxing authorities, based on the technical merits of the position. We believe that our assessment of more

likely than not is reasonable, but because of the subjectivity involved and the unpredictable nature of the subject matter at issue, our

assessment may prove ultimately to be incorrect, which could materially impact the Consolidated Financial Statements.

A V O N 2013 27