Avon 2013 Annual Report Download - page 58

Download and view the complete annual report

Please find page 58 of the 2013 Avon annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

|

|

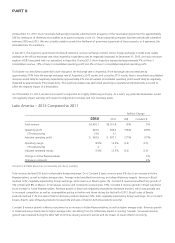

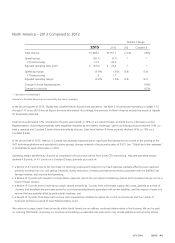

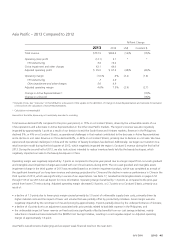

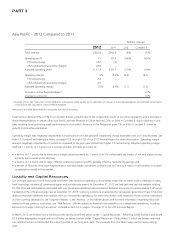

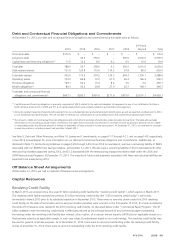

PART II

Term Loan Agreement

On June 29, 2012, we entered into a $500.0 term loan agreement (the “term loan agreement”). Subsequently on August 2, 2012, we

borrowed an incremental $50.0 of principal from subscriptions by new lenders under the term loan agreement. Pursuant to the term loan

agreement, we are required to repay an amount equal to 25% of the aggregate remaining principal amount of the term loan on June 29,

2014, and the remaining outstanding principal amount of the term loan on June 29, 2015. Amounts repaid or prepaid under the term loan

agreement may not be reborrowed. Borrowings under the term loan agreement bear interest, at our option, at a rate per annum equal to

LIBOR plus an applicable margin or a floating base rate plus an applicable margin, in each case subject to adjustment based on our credit

ratings. The term loan agreement also provides for mandatory prepayments and voluntary prepayments. Subject to certain exceptions

(including the issuance of commercial paper and draw-downs on our revolving credit facility), we are required to prepay the term loan in an

amount equal to 50% of the net cash proceeds received from any incurrence of debt for borrowed money in excess of $500.

In March 2013, we entered into the first amendment to the term loan agreement. This amendment primarily related to (i) adding a provision

whereby the lenders may, at our discretion, decline receipt of prepayments, and (ii) adding a subsidiary debt covenant and conforming the

interest coverage ratio and leverage ratio covenants to those contained in the revolving credit facility (discussed below under “Debt

Covenants”). Later in March 2013, we repaid $380.0 of the outstanding principal amount of the term loan agreement with a portion of the

proceeds from the issuance of the Notes (as defined below under “Public Notes”), which repayment resulted in a loss in the first quarter of

2013 of $1.6 on extinguishment of debt associated with the write-off of debt issuance costs related to the term loan agreement. On July 25,

2013, we prepaid $117.5 of the outstanding principal balance under the term loan agreement, without prepayment penalties. At

December 31, 2013, there was $52.5 outstanding under the term loan agreement.

Debt Covenants

The revolving credit facility and the term loan agreement (collectively, “the debt agreements”) contain covenants limiting our ability to incur

liens and enter into mergers and consolidations or sales of substantially all our assets. The debt agreements also contain covenants that limit

our subsidiary debt to existing subsidiary debt at February 28, 2013 plus $500.0, with certain other exceptions. In addition, the debt

agreements contain financial covenants which require our interest coverage ratio at the end of each fiscal quarter to equal or exceed 4:1 and

our leverage ratio to not be greater than 3.75:1 at the end of the fiscal quarter ended December 31, 2013 and each subsequent fiscal

quarter on or prior to September 30, 2014, and 3.5:1 at the end of each fiscal quarter thereafter. In addition, the debt agreements contain

customary events of default and cross-default provisions. The interest coverage ratio is determined by dividing our consolidated EBIT (as

defined in the debt agreements) by our consolidated interest expense, in each case for the period of four fiscal quarters ending on the date

of determination. The leverage ratio is determined by dividing the amount of our consolidated funded debt on the date of determination by

our consolidated EBITDA (as defined in the debt agreements) for the period of four fiscal quarters ending on the date of determination.

When calculating the interest coverage and leverage ratios, the debt agreements allow us, subject to certain conditions and limitations, to

add back to our consolidated net income, among other items: (i) extraordinary and other non-cash losses and expenses, (ii) one-time fees,

cash charges and other cash expenses, premiums or penalties incurred in connection with any asset sale, equity issuance or incurrence or

repayment of debt or refinancing or modification or amendment of any debt instrument and (iii) cash charges and other cash expenses,

premiums or penalties incurred in connection with any restructuring or relating to any legal or regulatory action, settlement, judgment or

ruling, in an aggregate amount not to exceed $400.0 for the period from October 1, 2012 until the termination of commitments under the

debt agreements; provided, that restructuring charges incurred after December 31, 2014 shall not be added back to our consolidated net

income. As of December 31, 2013, and based on then applicable interest rates, the full $1 billion revolving credit facility, less the principal

amount of commercial paper outstanding (which was $0 at December 31, 2013), could have been drawn down without violating any

covenant. We were in compliance with our interest coverage and leverage ratios under the debt agreements for the four fiscal quarters

ended December 31, 2013.

The indentures governing the notes described under the caption “Public Notes” below contain certain covenants, including limitations on

the incurrence of liens and restrictions on the incurrence of sale/leaseback transactions and transactions involving a merger, consolidation or

sale of substantially all of our assets. In addition, these indentures contain customary events of default and cross-default provisions. Further,

we would be required to make an offer to repurchase the 5.75% Notes due March 1, 2018, the 6.50% Notes, due March 1, 2019 and each

series of the Notes (as defined below) at a price equal to 101% of their aggregate principal amount plus accrued and unpaid interest in the

event of a change in control involving Avon and a corresponding credit ratings downgrade to below investment grade. In addition, the

indenture governing the Notes contains interest rate adjustment provisions depending on our credit ratings.