Allstate 2013 Annual Report Download - page 227

Download and view the complete annual report

Please find page 227 of the 2013 Allstate annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

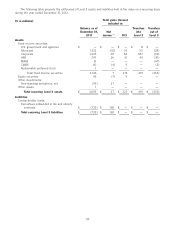

|

|

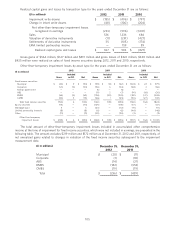

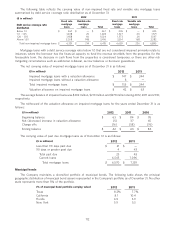

represented in the Company’s mortgage loan portfolio. No other state represented more than 5% of the portfolio as of

December 31.

(% of mortgage loan portfolio carrying value) 2012 2011

California 23.6 22.6%

Illinois 8.1 9.1

New York 6.4 5.8

Texas 6.4 6.2

New Jersey 6.2 6.5

Pennsylvania 4.9 5.3

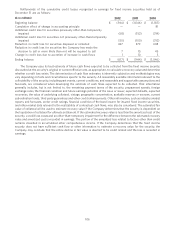

The types of properties collateralizing the mortgage loans as of December 31 are as follows:

(% of mortgage loan portfolio carrying value) 2012 2011

Office buildings 26.6% 27.9%

Retail 22.7 24.8

Apartment complex 20.6 19.6

Warehouse 19.7 19.4

Other 10.4 8.3

Total 100.0% 100.0%

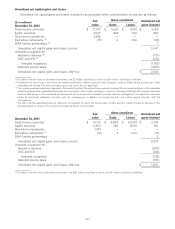

The contractual maturities of the mortgage loan portfolio as of December 31, 2012, excluding $4 million of

mortgage loans in the process of foreclosure, are as follows:

($ in millions) Number of Carrying

loans value Percent

2013 42 $ 339 5.2%

2014 64 758 11.5

2015 67 968 14.7

2016 72 813 12.4

Thereafter 334 3,688 56.2

Total 579 $ 6,566 100.0%

Mortgage loans are evaluated for impairment on a specific loan basis through a quarterly credit monitoring process

and review of key credit quality indicators. Mortgage loans are considered impaired when it is probable that the

Company will not collect the contractual principal and interest. Valuation allowances are established for impaired loans

to reduce the carrying value to the fair value of the collateral less costs to sell or the present value of the loan’s expected

future repayment cash flows discounted at the loan’s original effective interest rate. Impaired mortgage loans may not

have a valuation allowance when the fair value of the collateral less costs to sell is higher than the carrying value.

Valuation allowances are adjusted for subsequent changes in the fair value of the collateral less costs to sell. Mortgage

loans are charged off against their corresponding valuation allowances when there is no reasonable expectation of

recovery. The impairment evaluation is non-statistical in respect to the aggregate portfolio but considers facts and

circumstances attributable to each loan. It is not considered probable that additional impairment losses, beyond those

identified on a specific loan basis, have been incurred as of December 31, 2012.

Accrual of income is suspended for mortgage loans that are in default or when full and timely collection of principal

and interest payments is not probable. Cash receipts on mortgage loans on nonaccrual status are generally recorded as

a reduction of carrying value.

Debt service coverage ratio is considered a key credit quality indicator when mortgage loans are evaluated for

impairment. Debt service coverage ratio represents the amount of estimated cash flows from the property available to

the borrower to meet principal and interest payment obligations. Debt service coverage ratio estimates are updated

annually or more frequently if conditions are warranted based on the Company’s credit monitoring process.

111