Allstate 2013 Annual Report Download - page 157

Download and view the complete annual report

Please find page 157 of the 2013 Allstate annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

|

|

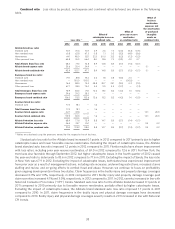

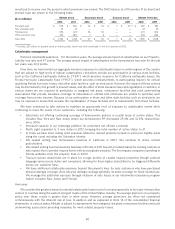

We have addressed our risk of hurricane loss by, among other actions, purchasing reinsurance for specific states

and on a countrywide basis for our personal lines property insurance in areas most exposed to hurricanes, limiting

personal homeowners new business writings in coastal areas in southern and eastern states, implementing tropical

cyclone deductibles where appropriate, and not offering continuing coverage on certain policies in coastal counties in

certain states. We continue to seek appropriate returns for the risks we write. This may require further actions, similar to

those already taken, in geographies where we are not getting appropriate returns. However, we may maintain or

opportunistically increase our presence in areas where we achieve adequate returns and do not materially increase our

hurricane risk.

Earthquakes

Actions taken to reduce our exposure from earthquake coverage are substantially complete. These actions included

purchasing reinsurance on a countrywide basis and in the state of Kentucky, no longer offering new optional earthquake

coverage in most states, removing optional earthquake coverage upon renewal in most states, and entering into

arrangements in many states to make earthquake coverage available through other insurers for new and renewal

business.

We expect to retain approximately 30,000 PIF with earthquake coverage due to regulatory and other reasons. We

also will continue to have exposure to earthquake risk on certain policies that do not specifically exclude coverage for

earthquake losses, including our auto policies, and to fires following earthquakes. Allstate policyholders in the state of

California are offered coverage through the CEA, a privately-financed, publicly-managed state agency created to provide

insurance coverage for earthquake damage. Allstate is subject to assessments from the CEA under certain

circumstances as explained in Note 14 of the consolidated financial statements.

Fires Following Earthquakes

Actions taken related to our risk of loss from fires following earthquakes include changing homeowners

underwriting requirements in California, purchasing reinsurance for Kentucky personal lines property risks, and

purchasing nationwide occurrence reinsurance, excluding Florida and New Jersey.

Wildfires

Actions we are taking to reduce our risk of loss from wildfires include changing homeowners underwriting

requirements in certain states and purchasing nationwide occurrence reinsurance.

Reinsurance

A description of our current catastrophe reinsurance program appears in Note 10 of the consolidated financial

statements.

DISCONTINUED LINES AND COVERAGES SEGMENT

Overview The Discontinued Lines and Coverages segment includes results from insurance coverage that we no

longer write and results for certain commercial and other businesses in run-off. Our exposure to asbestos,

environmental and other discontinued lines claims is reported in this segment. We have assigned management of this

segment to a designated group of professionals with expertise in claims handling, policy coverage interpretation,

exposure identification and reinsurance collection. As part of its responsibilities, this group may at times be engaged in

policy buybacks, settlements and reinsurance assumed and ceded commutations.

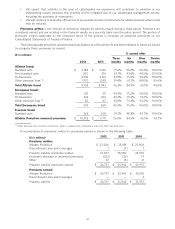

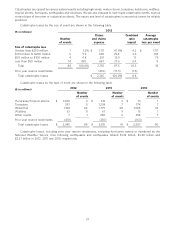

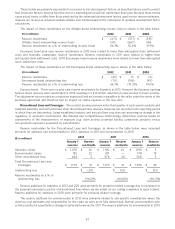

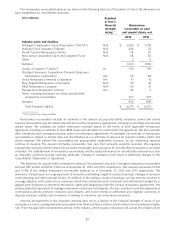

Summarized underwriting results for the years ended December 31 are presented in the following table.

($ in millions) 2012 2011 2010

Premiums written $ 1 $ (1) $ 1

Premiums earned $ — $ — $ 2

Claims and claims expense (51) (21) (28)

Operating costs and expenses (2) (4) (5)

Underwriting loss $ (53) $ (25) $ (31)

The underwriting loss of $53 million in 2012 related to a $26 million unfavorable reestimate of asbestos reserves, a

$22 million unfavorable reestimate of environmental reserves and a $5 million unfavorable reestimate of other reserves,

primarily as a result of our annual review using established industry and actuarial best practices, partially offset by a

$14 million decrease in our allowance for future uncollectable reinsurance. The cost of administering claims settlements

totaled $11 million for each of 2012 and 2011 and $13 million in 2010.

41