Allstate 2012 Annual Report Download - page 176

Download and view the complete annual report

Please find page 176 of the 2012 Allstate annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

|

|

There were no capital contributions by AIC to ALIC in 2011 or 2010. In 2009, capital contributions of $697 million

were paid by AIC to ALIC.

The Corporation has access to additional borrowing to support liquidity as follows:

• A commercial paper facility with a borrowing limit of $1.00 billion to cover short-term cash needs. As of

December 31, 2011, there were no balances outstanding and therefore the remaining borrowing capacity was

$1.00 billion; however, the outstanding balance can fluctuate daily.

• Our primary credit facility is available for short-term liquidity requirements and backs our commercial paper facility.

Our $1.00 billion unsecured revolving credit facility has an initial term of five years expiring in May 2012. The facility

is fully subscribed among 11 lenders with the largest commitment being $185 million. We have the option to extend

the expiration by one year upon approval of existing or replacement lenders providing more than two-thirds of the

commitments to lend. The commitments of the lenders are several and no lender is responsible for any other

lender’s commitment if such lender fails to make a loan under the facility. This facility contains an increase provision

that would allow up to an additional $500 million of borrowing provided the increased portion could be fully

syndicated at a later date among existing or new lenders. This facility has a financial covenant requiring that we not

exceed a 37.5% debt to capital resources ratio as defined in the agreement. This ratio as of December 31, 2011 was

20.0%. Although the right to borrow under the facility is not subject to a minimum rating requirement, the costs of

maintaining the facility and borrowing under it are based on the ratings of our senior, unsecured, nonguaranteed

long-term debt. There were no borrowings under the credit facility during 2011. The total amount outstanding at any

point in time under the combination of the commercial paper program and the credit facility cannot exceed the

amount that can be borrowed under the credit facility.

• A universal shelf registration statement was filed with the Securities and Exchange Commission on May 8, 2009.

We can use this shelf registration to issue an unspecified amount of debt securities, common stock (including

399 million shares of treasury stock as of December 31, 2011), preferred stock, depositary shares, warrants, stock

purchase contracts, stock purchase units and securities of trust subsidiaries. The specific terms of any securities we

issue under this registration statement will be provided in the applicable prospectus supplements.

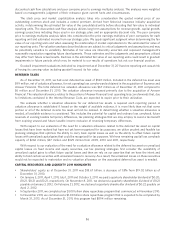

Liquidity exposure Contractholder funds as of December 31, 2011 were $42.33 billion. The following table

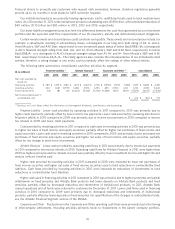

summarizes contractholder funds by their contractual withdrawal provisions as of December 31, 2011.

($ in millions) Percent to

total

Not subject to discretionary withdrawal $ 6,072 14.3%

Subject to discretionary withdrawal with adjustments:

Specified surrender charges (1) 16,079 38.0

Market value adjustments (2) 6,435 15.2

Subject to discretionary withdrawal without adjustments (3) 13,746 32.5

Total contractholder funds (4) $ 42,332 100.0%

(1) Includes $8.76 billion of liabilities with a contractual surrender charge of less than 5% of the account balance.

(2) $5.28 billion of the contracts with market value adjusted surrenders have a 30-45 day period at the end of their initial

and subsequent interest rate guarantee periods (which are typically 5 or 6 years) during which there is no surrender

charge or market value adjustment.

(3) 70% of these contracts have a minimum interest crediting rate guarantee of 3% or higher.

(4) Includes $1.16 billion of contractholder funds on variable annuities reinsured to The Prudential Insurance Company of

America, a subsidiary of Prudential Financial Inc., in 2006.

While we are able to quantify remaining scheduled maturities for our institutional products, anticipating retail

product surrenders is less precise. Retail life and annuity products may be surrendered by customers for a variety of

reasons. Reasons unique to individual customers include a current or unexpected need for cash or a change in life

insurance coverage needs. Other key factors that may impact the likelihood of customer surrender include the level of

the contract surrender charge, the length of time the contract has been in force, distribution channel, market interest

rates, equity market conditions and potential tax implications. In addition, the propensity for retail life insurance policies

to lapse is lower than it is for fixed annuities because of the need for the insured to be re-underwritten upon policy

replacement. Surrenders and partial withdrawals for our retail annuities increased 21.9% in 2011 compared to 2010. The

annualized surrender and partial withdrawal rate on deferred annuities and interest-sensitive life insurance products,

based on the beginning of year contractholder funds, was 12.6% and 10.1% in 2011 and 2010, respectively. Allstate

90