Allstate 2012 Annual Report Download - page 169

Download and view the complete annual report

Please find page 169 of the 2012 Allstate annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

|

|

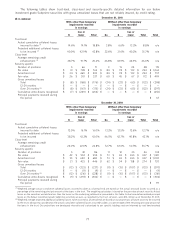

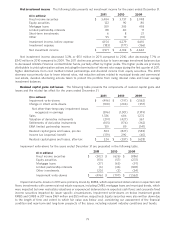

Equity price risk is the risk that we will incur losses due to adverse changes in the general levels of the equity

markets. As of December 31, 2011, we held $4.26 billion in common stocks and exchange traded and mutual funds and

$4.82 billion in other securities with equity risk (including primarily limited partnership interests, non-redeemable

preferred securities and equity-linked notes), compared to $4.67 billion and $4.88 billion, respectively, as of

December 31, 2010. 95.7% and 63.3% of these totals, respectively, represented assets of the Property-Liability

operations as of December 31, 2011, compared to 95.5% and 63.1%, respectively, as of December 31, 2010.

As of December 31, 2011, our portfolio of common stocks and other securities with equity risk had a cash market

portfolio beta of 0.72, compared to a beta of 0.74 as of December 31, 2010. Beta represents a widely used methodology

to describe, quantitatively, an investment’s market risk characteristics relative to an index such as the S&P 500. Based

on the beta analysis, we estimate that if the S&P 500 increases or decreases by 10%, the fair value of our equity

investments will increase or decrease by 7.2%, respectively. Based upon the information and assumptions we used to

calculate beta as of December 31, 2011, we estimate that an immediate decrease in the S&P 500 of 10% would decrease

the net fair value of our equity investments identified above by $652 million, compared to $695 million as of

December 31, 2010, and an immediate increase in the S&P 500 of 10% would increase the net fair value by $654 million

compared to $708 million as of December 31, 2010. In calculating the impact of a 10% S&P index perturbation on the

value of the puts, we have assumed index volatility remains constant. The selection of a 10% immediate decrease or

increase in the S&P 500 should not be construed as our prediction of future market events, but only as an illustration of

the potential effect of such an event.

The beta of our common stocks and other securities with equity risk was determined by calculating the change in

the fair value of the portfolio resulting from stressing the equity market up and down 10%. The illustrations noted above

may not reflect our actual experience if the future composition of the portfolio (hence its beta) and correlation

relationships differ from the historical relationships.

As of December 31, 2011 and 2010, we had separate accounts assets related to variable annuity and variable life

contracts with account values totaling $6.98 billion and $8.68 billion, respectively. Equity risk exists for contract charges

based on separate account balances and guarantees for death and/or income benefits provided by our variable

products. In 2006, we disposed of substantially all of the variable annuity business through reinsurance agreements

with The Prudential Insurance Company of America, a subsidiary of Prudential Financial Inc. and therefore mitigated this

aspect of our risk. Equity risk for our variable life business relates to contract charges and policyholder benefits. Total

variable life contract charges for 2011 and 2010 were $76 million and $80 million, respectively. Separate account

liabilities related to variable life contracts were $716 million and $775 million in December 31, 2011 and 2010,

respectively.

As of December 31, 2011 and 2010 we had $3.86 billion and $4.70 billion, respectively, in equity-indexed annuity

liabilities that provide customers with interest crediting rates based on the performance of the S&P 500. We hedge the

majority of the risk associated with these liabilities using equity-indexed options and futures, interest rate swaps, and

eurodollar futures, maintaining risk within specified value-at-risk limits.

Foreign currency exchange rate risk is the risk that we will incur economic losses due to adverse changes in foreign

currency exchange rates. This risk primarily arises from our foreign equity investments, including real estate funds and

private equity funds, and our Canadian and Northern Ireland operations. We also have certain fixed income securities

that are denominated in foreign currencies; however, derivatives are used to hedge the foreign currency risk of

approximately 38% of the fixed income securities.

As of December 31, 2011, we had $1.24 billion in foreign currency denominated equity investments, $786 million net

investment in our foreign subsidiaries, and $363 million in unhedged non-dollar pay fixed income securities. These

amounts were $1.70 billion, $773 million, and $91 million, respectively, as of December 31, 2010. 90.0% of the foreign

currency exposure is in the Property-Liability business.

Based upon the information and assumptions used as of December 31, 2011, we estimate that a 10% immediate

unfavorable change in each of the foreign currency exchange rates to which we are exposed would decrease the value of

our foreign currency denominated instruments by $225 million, compared with an estimated $257 million decrease as

of December 31, 2010. The selection of a 10% immediate decrease in all currency exchange rates should not be

construed as our prediction of future market events, but only as an illustration of the potential effect of such an event.

Our currency exposure is diversified across 33 currencies as of December 31, 2011, compared to 32 currencies as of

December 31, 2010. Our largest individual foreign currency exposures as of December 31, 2011 were to the Canadian

dollar (39.6%) and the Japanese Yen (10.4%). The largest individual foreign currency exposures as of December 31,

83