Allstate 2012 Annual Report Download - page 154

Download and view the complete annual report

Please find page 154 of the 2012 Allstate annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

|

|

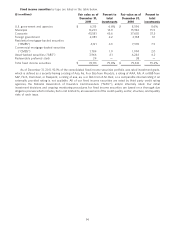

Municipal bonds, including tax exempt, taxable and ARS securities, totaled $14.24 billion as of December 31, 2011

with an unrealized net capital gain of $607 million. The municipal bond portfolio includes general obligations of state

and local issuers, revenue bonds and pre-refunded bonds, which are bonds for which an irrevocable trust has been

established to fund the remaining payments of principal and interest.

The following table summarizes by state the fair value, amortized cost and credit rating of our municipal bonds,

excluding $1.39 billion of pre-refunded bonds, as of December 31, 2011.

($ in millions) State Average

general Local general Amortized credit

State obligation obligation Revenue (1) Fair value cost rating

California $ 76 $ 626 $ 632 $ 1,334 $ 1,316 A

Texas 24 391 574 989 922 Aa

Florida 43 163 558 764 728 A

New York 33 108 535 676 637 Aa

Ohio 99 197 249 545 530 A

Illinois — 147 347 494 457 A

Missouri 30 131 286 447 429 A

Delaware — — 393 393 428 Aa

Pennsylvania 94 92 200 386 378 Aa

Michigan 33 137 211 381 365 Aa

All others 1,127 1,422 3,898 6,447 6,164 A

Total $ 1,559 $ 3,414 $ 7,883 $ 12,856 $ 12,354 A

(1) The nature of the activities supporting revenue bonds is highly diversified and includes transportation, health care, industrial

development, housing, higher education, utilities, recreation/convention centers and other activities.

Our practice for acquiring and monitoring municipal bonds is predominantly based on the underlying credit quality

of the primary obligor. We currently rely on the primary obligor to pay all contractual cash flows and are not relying on

bond insurers for payments. As a result of downgrades in the insurers’ credit ratings, the ratings of the insured municipal

bonds generally reflect the underlying ratings of the primary obligor. As of December 31, 2011, 99.3% of our insured

municipal bond portfolio is rated investment grade.

ARS totaled $742 million with an unrealized net capital loss of $80 million as of December 31, 2011. Our holdings

primarily have a credit rating of Aaa. As of December 31, 2011, $710 million of our ARS backed by student loans was

80% to 100% insured by the U.S. Department of Education. All of our ARS holdings are experiencing failed auctions and

we receive the failed auction rate or, for those which contain maximum reset rate formulas, we receive the contractual

maximum rate. We anticipate that failed auctions may persist and most of our holdings will continue to pay the failed

auction rate or, for those that contain maximum rate reset formulas, the maximum rate. Auctions continue to be

conducted as scheduled for each of the securities.

Corporate bonds, including publicly traded and privately placed, totaled $43.58 billion as of December 31, 2011 with

an unrealized net capital gain of $2.36 billion. Privately placed securities primarily consist of corporate issued senior

debt securities that are directly negotiated with the borrower or are in unregistered form.

Our portfolio of privately placed securities is broadly diversified by issuer, industry sector and country. The portfolio

is made up of 525 issuers. Privately placed corporate obligations contain structural security features such as financial

covenants and call protections that provide investors greater protection against credit deterioration, reinvestment risk

or fluctuations in interest rates than those typically found in publicly registered debt securities. Additionally,

investments in these securities are made after extensive due diligence of the issuer, typically including direct discussions

with senior management and on-site visits to company facilities. Ongoing monitoring includes direct periodic dialog

with senior management of the issuer and continuous monitoring of operating performance and financial position. Every

issue not rated by an independent rating agency is internally rated with a formal rating affirmation at least once a year.

Foreign government securities totaled $2.08 billion as of December 31, 2011, with 100% rated investment grade and

an unrealized net capital gain of $215 million. Of these securities, 18.8% are backed by the U.S. government, 35.1% are in

Canadian governmental securities held in our Canadian subsidiary and the remaining 46.1% are highly diversified in

other foreign governments.

68