Allstate 2012 Annual Report Download - page 172

Download and view the complete annual report

Please find page 172 of the 2012 Allstate annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

|

|

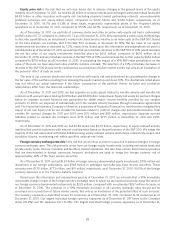

discounted cash flow calculations and peer company price to earnings multiples analysis. The analyses were weighted

based on management’s judgment of their relevance given current facts and circumstances.

The stock price and market capitalization analysis takes into consideration the quoted market price of our

outstanding common stock and includes a control premium, derived from historical insurance industry acquisition

activity, in determining the estimated fair value of the consolidated entity before allocating that fair value to individual

reporting units. The discounted cash flow analysis utilizes long term assumptions for revenue growth, capital growth,

earnings projections including those used in our strategic plan, and an appropriate discount rate. The peer company

price to earnings multiples analysis takes into consideration the price earnings multiples of peer companies for each

reporting unit and estimated income from our strategic plan. We apply significant judgment when determining the fair

value of our reporting units and when assessing the relationship of market capitalization to the estimated fair value of

our reporting units. The valuation analyses described above are subject to critical judgments and assumptions and may

be potentially sensitive to variability. Estimates of fair value are inherently uncertain and represent management’s

reasonable expectation regarding future developments. These estimates and the judgments and assumptions utilized

may differ from future actual results. Declines in the estimated fair value of our reporting units could result in goodwill

impairments in future periods which may be material to our results of operations but not our financial position.

Goodwill impairment evaluations indicated no impairment as of December 31, 2011 and no reporting unit was at risk

of having its carrying value including goodwill exceed its fair value.

DEFERRED TAXES

As of December 31, 2011, we had a net deferred tax asset of $520 million. Included in the deferred tax asset was

$99 million, net of valuation allowance, for net operating loss carryforwards obtained in the acquisition of Esurance and

Answer Financial. The total deferred tax valuation allowance was $67 million as of December 31, 2011 compared to

$6 million as of December 31, 2010. The valuation allowance increased primarily due to the acquisition of Answer

Financial. The valuation allowance relates to the portion of Answer Financial’s net operating loss carryforwards that, due

to limitations contained in the Internal Revenue Code, are expected to expire prior to their utilization.

We evaluate whether a valuation allowance for our deferred tax assets is required each reporting period. A

valuation allowance is established if, based on the weight of available evidence, it is more likely than not that some

portion or all of the deferred income tax asset will not be realized. In determining whether a valuation allowance is

needed, all available evidence is considered. This includes the potential for capital and ordinary loss carryback, future

reversals of existing taxable temporary differences, tax planning strategies that we may employ to avoid a tax benefit

from expiring unused and future taxable income exclusive of reversing temporary differences.

With respect to our evaluation of the need for a valuation allowance related to the deferred tax asset on capital

losses that have been realized but have not yet been recognized for tax purposes, we utilize prudent and feasible tax

planning strategies that optimize the ability to carry back capital losses as well as the ability to offset future capital

losses with unrealized capital gains that could be recognized for tax purposes. We have remaining capital loss carryback

capacity of $266 million, $37 million and $329 million from 2009, 2010 and 2011, respectively.

With respect to our evaluation of the need for a valuation allowance related to the deferred tax asset on unrealized

capital losses on fixed income and equity securities, our tax planning strategies first consider the availability of

unrealized capital gains to offset future capital losses and then we rely on our assertion that we have the intent and

ability to hold certain securities with unrealized losses to recovery. As a result, the unrealized losses on these securities

would not be expected to materialize and no valuation allowance on the associated deferred tax asset is needed.

CAPITAL RESOURCES AND LIQUIDITY 2011 HIGHLIGHTS

• Shareholders’ equity as of December 31, 2011 was $18.67 billion, a decrease of 1.8% from $19.02 billion as of

December 31, 2010.

• On January 3, 2011, April 1, 2011, July 1, 2011 and October 3, 2011, we paid a quarterly shareholder dividend of $0.20,

$0.21, $0.21 and $0.21, respectively. On November 8, 2011, we declared a quarterly shareholder dividend of $0.21

payable on January 3, 2012. On February 21, 2012, we declared a quarterly shareholder dividend of $0.22 payable on

April 2, 2012.

• In September 2011, we completed our $1.00 billion share repurchase program that commenced in November 2010.

• In November 2011, we commenced a $1.00 billion share repurchase program that is expected to be completed by

March 31, 2013. As of December 31, 2011, this program had $894 million remaining.

86