Allstate 2012 Annual Report Download - page 147

Download and view the complete annual report

Please find page 147 of the 2012 Allstate annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

|

|

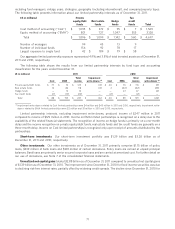

Amortization of DAC increased 66.6% or $237 million in 2011 compared to 2010 and decreased 63.1% or

$609 million in 2010 compared to 2009. The components of amortization of DAC are summarized in the following table

for the years ended December 31.

($ in millions) 2011 2010 2009

Amortization of DAC before amortization relating

to realized capital gains and losses, valuation

changes on embedded derivatives that are not

hedged and changes in assumptions $ 397 $ 326 $ 472

Amortization relating to realized capital gains and

losses (1) and valuation changes on embedded

derivatives that are not hedged 184 42 216

Amortization acceleration (deceleration) for

changes in assumptions (‘‘DAC unlocking’’) 12 (12) 277

Total amortization of DAC $ 593 $ 356 $ 965

(1) The impact of realized capital gains and losses on amortization of DAC is dependent upon the relationship between

the assets that give rise to the gain or loss and the product liability supported by the assets. Fluctuations result from

changes in the impact of realized capital gains and losses on actual and expected gross profits.

The increase of $237 million in 2011 was primarily due to increased amortization relating to realized capital gains,

lower amortization in the second quarter of 2010 resulting from decreased benefit spread on interest-sensitive life

insurance due to the reestimation of reserves, and an unfavorable change in amortization acceleration/deceleration for

changes in assumptions. In 2011, DAC amortization relating to realized capital gains and losses primarily resulted from

realized capital gains on sales of fixed income securities.

The decrease of $609 million in 2010 was primarily due to a favorable change in amortization acceleration/

deceleration for changes in assumptions, lower amortization relating to realized capital gains and losses, a decreased

amortization rate on fixed annuities and lower amortization from decreased benefit spread on interest-sensitive life

insurance due to the reestimation of reserves. In 2010, DAC amortization relating to realized capital gains and losses

primarily resulted from realized capital gains on derivatives and sales of fixed income securities.

During the first quarter of 2011, we completed our annual comprehensive review of the profitability of our products

to determine DAC balances for our interest-sensitive life, fixed annuities and other investment contracts which covers

assumptions for investment returns, including capital gains and losses, interest crediting rates to policyholders, the

effect of any hedges, persistency, mortality and expenses in all product lines. The review resulted in an acceleration of

DAC amortization (charge to income) of $12 million in the first quarter of 2011. Amortization acceleration of $17 million

related to interest-sensitive life insurance and was primarily due to an increase in projected expenses. Amortization

deceleration of $5 million related to equity-indexed annuities and was primarily due to an increase in projected

investment margins.

In 2010, our annual comprehensive review resulted in a deceleration of DAC amortization (credit to income) of

$12 million. Amortization deceleration of $45 million related to variable life insurance and was primarily due to

appreciation in the underlying separate account valuations. Amortization acceleration of $32 million related to interest-

sensitive life insurance and was primarily due to an increase in projected realized capital losses and lower projected

renewal premium (which is also expected to reduce persistency), partially offset by lower expenses.

In 2009, our annual comprehensive review resulted in the acceleration of DAC amortization of $277 million.

$289 million related to fixed annuities, of which $210 million was attributable to market value adjusted annuities, and

$18 million related to variable life insurance. Partially offsetting these amounts was amortization deceleration for

interest-sensitive life insurance of $30 million. The principal assumption impacting fixed annuity amortization

acceleration was an increase in the level of expected realized capital losses in 2009 and 2010. For interest-sensitive life

insurance, the amortization deceleration was due to a favorable change in our mortality assumptions, partially offset by

increased expected capital losses.

61