Allstate 2011 Annual Report Download - page 236

Download and view the complete annual report

Please find page 236 of the 2011 Allstate annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

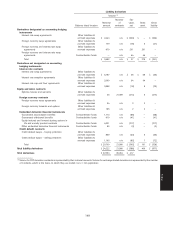

Incurred claims and claims expense represents the sum of paid losses and reserve changes in the calendar year.

This expense includes losses from catastrophes of $2.21 billion, $2.07 billion and $3.34 billion in 2010, 2009 and 2008,

respectively, net of reinsurance and other recoveries (see Note 9). In 2008, losses from catastrophes included

$1.31 billion, net of recoveries, related to Hurricanes Ike and Gustav. These estimates include net losses in personal lines

auto and property policies and net losses on commercial policies. Included in 2008 losses from catastrophes are

accruals for assessments from the Texas Windstorm Insurance Association (‘‘TWIA’’) (see Note 13).

Catastrophes are an inherent risk of the property-liability insurance business that have contributed to, and will

continue to contribute to, material year-to-year fluctuations in the Company’s results of operations and financial

position.

The Company calculates and records a single best reserve estimate for losses from catastrophes, in conformance

with generally accepted actuarial standards. As a result, management believes that no other estimate is better than the

recorded amount. Due to the uncertainties involved, including the factors described above, the ultimate cost of losses

may vary materially from recorded amounts, which are based on management’s best estimates. Accordingly,

management believes that it is not practical to develop a meaningful range for any such changes in losses incurred.

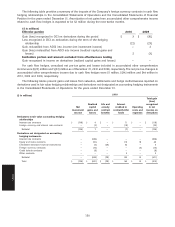

During 2010, incurred claims and claims expense related to prior years was primarily composed of net decreases in

auto reserves of $179 million primarily due to claim severity development that was better than expected partially offset

by a litigation settlement, net decreases in homeowners reserves of $23 million due to favorable catastrophe reserve

reestimates partially offset by a litigation settlement, and net increases in other reserves of $15 million. Incurred claims

and claims expense includes favorable catastrophe loss reestimates of $163 million, net of reinsurance and other

recoveries.

During 2009, incurred claims and claims expense related to prior years was primarily composed of net decreases in

homeowners and auto reserves of $168 million and $57 million, respectively, partially offset by increases in other

reserves of $89 million. Incurred claims and claims expense includes favorable catastrophe loss reestimates of

$169 million, net of reinsurance and other recoveries, primarily attributable to favorable reserve reestimates from

Hurricanes Ike and Gustav and a catastrophe related subrogation recovery.

During 2008, incurred claims and claims expense related to prior years was primarily composed of net decreases in

auto reserves of $27 million offset by increases in homeowners reserves of $124 million due to catastrophe loss

reestimates, and increases in other reserves of $55 million. The $27 million favorable decreases in auto reserves and

$55 million unfavorable increases in other reserves includes $45 million of IBNR losses reclassified from auto reserves

to other reserves to be consistent with the recording of excess liability policy premiums and losses. Incurred claims and

claims expense includes unfavorable catastrophe loss reestimates of $125 million, net of reinsurance and other

recoveries, primarily attributable to increased claim loss and expense reserves for litigation filed in conjunction with a

Louisiana deadline for filing suits related to Hurricane Katrina.

Management believes that the reserve for property-liability insurance claims and claims expense, net of

reinsurance recoverables, is appropriately established in the aggregate and adequate to cover the ultimate net cost of

reported and unreported claims arising from losses which had occurred by the date of the Consolidated Statements of

Financial Position based on available facts, technology, laws and regulations.

For further discussion of asbestos and environmental reserves, see Note 13.

8. Reserve for Life-Contingent Contract Benefits and Contractholder Funds

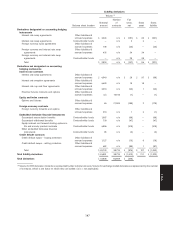

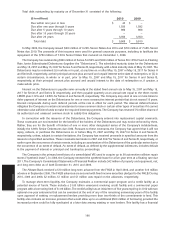

As of December 31, the reserve for life-contingent contract benefits consists of the following:

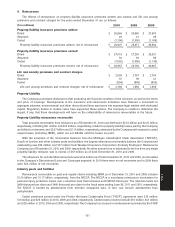

($ in millions) 2010 2009

Immediate fixed annuities:

Structured settlement annuities $ 6,522 $ 6,406

Other immediate fixed annuities 2,215 2,048

Traditional life insurance 2,938 2,850

Accident and health insurance 1,720 1,514

Other 87 92

Total reserve for life-contingent contract benefits $ 13,482 $ 12,910

156

Notes