Allstate 2011 Annual Report Download - page 215

Download and view the complete annual report

Please find page 215 of the 2011 Allstate annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

whether a significant decrease in the volume and level of activity for a specific asset has occurred include the level of

new issuances in the primary market, trading volume in the secondary market, the level of credit spreads over historical

levels, applicable bid-ask spreads, and price consensus among market participants and other pricing sources.

The second situation where the Company classifies securities in Level 3 is where specific inputs significant to the

fair value estimation models are not market observable. This occurs in two primary instances. The first relates to the

Company’s use of broker quotes. The second relates to auction rate securities (‘‘ARS’’) backed by student loans for

which a key input, the anticipated date liquidity will return to this market, is not market observable.

Certain assets are not carried at fair value on a recurring basis, including investments such as mortgage loans,

limited partnership interests, bank loans and policy loans. Accordingly, such investments are only included in the fair

value hierarchy disclosure when the investment is subject to remeasurement at fair value after initial recognition and the

resulting remeasurement is reflected in the consolidated financial statements. In addition, derivatives embedded in

fixed income securities are not disclosed in the hierarchy as free-standing derivatives since they are presented with the

host contracts in fixed income securities. As of December 31, 2010, 74.1% of total assets are measured at fair value and

0.9% of total liabilities are measured at fair value.

In determining fair value, the Company principally uses the market approach which generally utilizes market

transaction data for the same or similar instruments. To a lesser extent, the Company uses the income approach which

involves determining fair values from discounted cash flow methodologies. For the majority of Level 2 and Level 3

valuations, a combination of the market and income approaches is used.

Summary of significant valuation techniques for assets and liabilities measured at fair value on a recurring basis

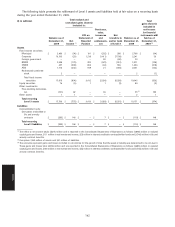

Level 1 measurements

• Fixed income securities: Comprise U.S. Treasuries. Valuation is based on unadjusted quoted prices for

identical assets in active markets that the Company can access.

• Equity securities: Comprise actively traded, exchange-listed U.S. and international equity securities. Valuation

is based on unadjusted quoted prices for identical assets in active markets that the Company can access.

• Short-term: Comprise actively traded money market funds that have daily quoted net asset values for identical

assets that the Company can access.

• Separate account assets: Comprise actively traded mutual funds that have daily quoted net asset values for

identical assets that the Company can access. Net asset values for the actively traded mutual funds in which

the separate account assets are invested are obtained daily from the fund managers.

Level 2 measurements

• Fixed income securities:

U.S. government and agencies: The primary inputs to the valuation include quoted prices for identical or similar

assets in markets that are not active, contractual cash flows, benchmark yields and credit spreads.

Municipal: The primary inputs to the valuation include quoted prices for identical or similar assets in markets

that are not active, contractual cash flows, benchmark yields and credit spreads.

Corporate, including privately placed: The primary inputs to the valuation include quoted prices for identical or

similar assets in markets that are not active, contractual cash flows, benchmark yields and credit spreads. Also

included are privately placed securities valued using a discounted cash flow model that is widely accepted in

the financial services industry and uses market observable inputs and inputs derived principally from, or

corroborated by, observable market data. The primary inputs to the discounted cash flow model include an

interest rate yield curve, as well as published credit spreads for similar assets in markets that are not active that

incorporate the credit quality and industry sector of the issuer.

Foreign government: The primary inputs to the valuation include quoted prices for identical or similar assets in

markets that are not active, contractual cash flows, benchmark yields and credit spreads.

RMBS – U.S. government sponsored entities (‘‘U.S. Agency’’), Prime residential mortgage-backed securities

(‘‘Prime’’) and Alt-A residential mortgage-backed securities (‘‘Alt-A’’); ABS – auto and student loans and

other: The primary inputs to the valuation include quoted prices for identical or similar assets in markets that

are not active, contractual cash flows, benchmark yields, prepayment speeds, collateral performance and credit

spreads.

135

Notes