Allstate 2011 Annual Report Download - page 181

Download and view the complete annual report

Please find page 181 of the 2011 Allstate annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

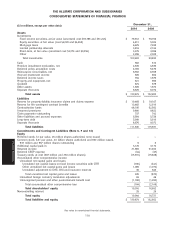

|

|

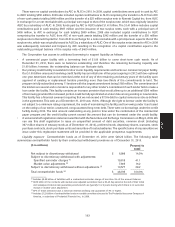

respectively, as well as the AA- financial strength rating of AIC. S&P downgraded the financial strength rating for ALIC

to A+ from AA-. The outlook for all S&P ratings was revised to stable from negative.

We have distinct and separately capitalized groups of subsidiaries licensed to sell property and casualty insurance

in New Jersey and Florida that maintain separate group ratings. The ratings of these groups are influenced by the risks

that relate specifically to each group. Many mortgage companies require property owners to have insurance from an

insurance carrier with a secure financial strength rating from an accredited rating agency. Allstate New Jersey

Insurance Company and Encompass Insurance Company of New Jersey, which write auto and homeowners insurance,

are rated A- by A.M. Best. Allstate New Jersey Insurance Company also has a Financial Stability Rating姞 of A’’ from

Demotech. The outlook for these ratings is stable. Castle Key Insurance Company and its subsidiaries, which underwrite

personal lines property insurance in Florida, are rated B- by A.M. Best. The outlook for the ratings of Castle Key

Insurance Company and its subsidiaries is negative. Castle Key Insurance Company and its subsidiaries also have

Financial Stability Ratings姞 of A’ from Demotech.

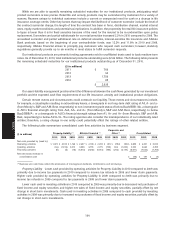

ALIC, AIC and the Corporation are party to the Amended and Restated Intercompany Liquidity Agreement

(‘‘Liquidity Agreement’’) which allows for short-term advances of funds to be made between parties for liquidity and

other general corporate purposes. The Liquidity Agreement does not establish a commitment to advance funds on the

part of any party. ALIC and AIC each serve as a lender and borrower and the Corporation serves only as a lender. AIC

also has a capital support agreement with ALIC. Under the capital support agreement, AIC is committed to provide

capital to ALIC to maintain an adequate capital level. The maximum amount of potential funding under each of these

agreements is $1.00 billion.

In addition to the Liquidity Agreement, the Corporation also has an intercompany loan agreement with certain of its

subsidiaries, which include, but are not limited to, AIC and ALIC. The amount of intercompany loans available to the

Corporation’s subsidiaries is at the discretion of the Corporation. The maximum amount of loans the Corporation will

have outstanding to all its eligible subsidiaries at any given point in time is limited to $1.00 billion. The Corporation may

use commercial paper borrowings, bank lines of credit and repurchase agreements to fund intercompany borrowings.

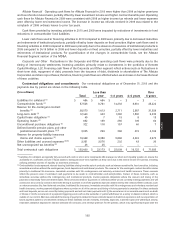

Allstate’s domestic property-liability and life insurance subsidiaries prepare their statutory-basis financial

statements in conformity with accounting practices prescribed or permitted by the insurance department of the

applicable state of domicile. Statutory surplus is a measure that is often used as a basis for determining dividend paying

capacity, operating leverage and premium growth capacity, and it is also reviewed by rating agencies in determining

their ratings. As of December 31, 2010, AIC’s statutory surplus is approximately $15.38 billion compared to $15.03 billion

as of December 31, 2009. These amounts include ALIC’s statutory surplus of approximately $3.34 billion as of

December 31, 2010, compared to $3.47 billion as of December 31, 2009.

The ratio of net premiums written to statutory surplus is a common measure of operating leverage used in the

property-casualty insurance industry and serves as an indicator of a company’s premium growth capacity. Ratios in

excess of 3 to 1 are typically considered outside the usual range by insurance regulators and rating agencies. AIC’s

premium to surplus ratio was 1.6x on December 31, 2010 compared to 1.7x in the prior year.

State laws specify regulatory actions if an insurer’s risk-based capital (‘‘RBC’’), a measure of an insurer’s solvency,

falls below certain levels. The NAIC has a standard formula for annually assessing RBC. The formula for calculating RBC

for property-liability companies takes into account asset and credit risks but places more emphasis on underwriting

factors for reserving and pricing. The formula for calculating RBC for life insurance companies takes into account

factors relating to insurance, business, asset and interest rate risks. As of December 31, 2010, the RBC for each of our

domestic insurance companies was within the range that we target.

The NAIC has also developed a set of financial relationships or tests known as the Insurance Regulatory

Information System to assist state regulators in monitoring the financial condition of insurance companies and

identifying companies that require special attention or actions by insurance regulatory authorities. The NAIC analyzes

financial data provided by insurance companies using prescribed ratios, each with defined ‘‘usual ranges’’. Generally,

regulators will begin to monitor an insurance company if its ratios fall outside the usual ranges for four or more of the

ratios. If an insurance company has insufficient capital, regulators may act to reduce the amount of insurance it can

issue. The ratios of our domestic insurance companies are within these ranges.

101

MD&A