Wells Fargo 2013 Annual Report Download - page 86

Download and view the complete annual report

Please find page 86 of the 2013 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

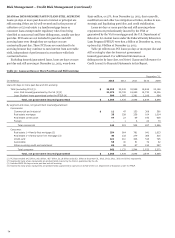

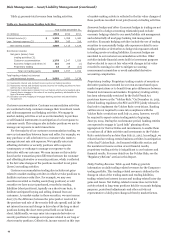

Asset/Liability Management

Asset/liability management involves evaluating, monitoring and

managing interest rate risk, market risk, liquidity and funding.

Primary oversight of these risks resides with the Finance

Committee of our Board of Directors (Board), which oversees the

administration and effectiveness of financial risk management

policies and processes used to assess and manage these risks. At

the management level we utilize a Corporate Asset/Liability

Management Committee (Corporate ALCO), which consists of

senior financial and business executives, to oversee these risks

and report on them periodically to the Board’s Finance

Committee. Each of our principal lines of business has its own

asset/liability management committee and process linked to the

Corporate ALCO process. As discussed in more detail for trading

activities below, we employ separate management level oversight

specific to the market risks related to our trading activities.

Market risk, in its broadest sense, refers to the possibility that

losses will result from the impact of adverse changes in market

rates and prices on our trading and non-trading portfolios and

financial instruments.

INTEREST RATE RISK Interest rate risk, which potentially can

have a significant earnings impact, is an integral part of being a

financial intermediary. We are subject to interest rate risk

because:

x

x

x

x

x

assets and liabilities may mature or reprice at different

times (for example, if assets reprice faster than liabilities

and interest rates are generally falling, earnings will initially

decline);

assets and liabilities may reprice at the same time but by

different amounts (for example, when the general level of

interest rates is falling, we may reduce rates paid on

checking and savings deposit accounts by an amount that is

less than the general decline in market interest rates);

short-term and long-term market interest rates may change

by different amounts (for example, the shape of the yield

curve may affect new loan yields and funding costs

differently);

the remaining maturity of various assets or liabilities may

shorten or lengthen as interest rates change (for example, if

long-term mortgage interest rates decline sharply, MBS held

in the investment securities portfolio may prepay

significantly earlier than anticipated, which could reduce

portfolio income); or

interest rates may also have a direct or indirect effect on

loan demand, collateral values, credit losses, mortgage

origination volume, the fair value of MSRs and other

financial instruments, the value of the pension liability and

other items affecting earnings.

We assess interest rate risk by comparing outcomes under

various earnings simulations using many interest rate scenarios

that differ in the direction of interest rate changes, the degree of

change over time, the speed of change and the projected shape of

the yield curve. These simulations require assumptions

regarding how changes in interest rates and related market

conditions could influence drivers of earnings and balance sheet

composition such as loan origination demand, prepayment

speeds, deposit balances and mix, as well as pricing strategies.

Our risk measures include both net interest income

sensitivity and interest rate sensitive noninterest income and

expense impacts. We refer to the combination of these exposures

as interest rate sensitive earnings. In general, the Company is

positioned to benefit from higher interest rates. Currently, our

profile is such that net interest income will benefit from higher

interest rates as our assets reprice faster and to a greater degree

than our liabilities, and, in response to lower market rates, our

assets will reprice downward and to a greater degree than our

liabilities. Our interest rate sensitive noninterest income and

expense is largely driven by mortgage activity, and tends to move

in the opposite direction of our net interest income. So, in

response to higher interest rates, mortgage activity, primarily

refinancing activity, generally declines. And in response to lower

rates, mortgage activity generally increases. Mortgage results are

also impacted by the valuation of MSRs and related hedge

positions. See the “Risk Management – Mortgage Banking

Interest Rate and Market Risk” section in this Report for more

information.

The degree to which these sensitivities offset each other is

dependent upon the timing and magnitude of changes in interest

rates, and the slope of the yield curve. During a transition to a

higher or lower interest rate environment, a reduction or

increase in interest-sensitive earnings from the mortgage

banking business could occur quickly, while the benefit or

detriment from balance sheet repricing could take more time to

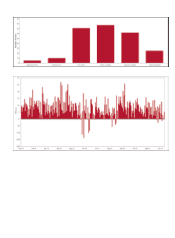

develop. For example, our lower rate scenarios (scenario 1 and

scenario 2) in the following table initially measure a decline in

long-term interest rates versus our most likely scenario.

Although the performance in both lower rate scenarios contains

initial benefit from increased mortgage banking activity, each

results in lower earnings relative to the most likely scenario over

time given pressure on net interest income. The higher rate

scenarios (scenario 3 and scenario 4) measure the impact of

varying degrees of rising short-term and long-term interest rates

over the course of the forecast horizon relative to the most likely

scenario, both resulting in positive earnings sensitivity.

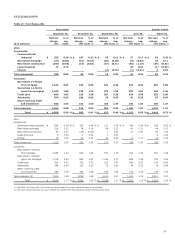

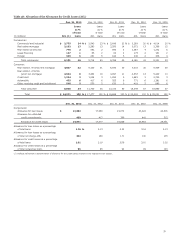

As of December 31, 2013, our most recent simulations

estimate earnings at risk over the next 24 months under a range

of both lower and higher interest rates. The results of the

simulations are summarized in Table 42, indicating cumulative

net income after tax earnings sensitivity relative to the most

likely earnings plan over the 24 month horizon (a positive range

indicates a beneficial earnings sensitivity measurement relative

to the most likely earnings plan).

84