Wells Fargo 2013 Annual Report Download - page 72

Download and view the complete annual report

Please find page 72 of the 2013 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

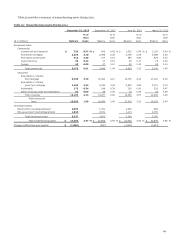

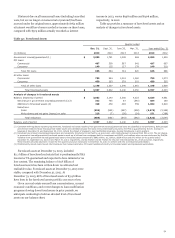

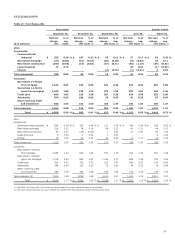

Risk Management – Credit Risk Management (continued)

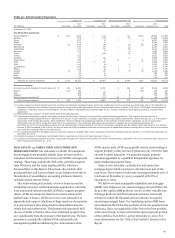

Table 31 provides an analysis of the changes in nonaccrual

loans.

Table 31: Analysis of Changes in Nonaccrual Loans

Quarter ended

Dec. 31, Sept. 30, June 30, Mar. 31, Year ended Dec. 31,

(in millions) 2013 2013 2013 2013 2013 2012

Commercial nonaccrual loans

Balance, beginning of period $ 3,886 4,455 5,242 5,824 5,824 8,217

Inflows 520 490 557 611 2,178 3,812

Outflows:

Returned to accruing (67) (192) (128) (109) (496) (655)

Foreclosures (34) (77) (120) (91) (322) (469)

Charge-offs (191) (150) (193) (189) (723) (1,435)

Payments, sales and other (1) (639) (640) (903) (804) (2,986) (3,646)

Total outflows (931) (1,059) (1,344) (1,193) (4,527) (6,205)

Balance, end of period 3,475 3,886 4,455 5,242 3,475 5,824

Consumer nonaccrual loans

Balance, beginning of period 13,007 13,460 14,284 14,662 14,662 13,087

Inflows 1,691 2,015 2,071 2,340 8,117 14,569

Outflows:

Returned to accruing (953) (997) (1,156) (1,031) (4,137) (4,219)

Foreclosures (162) (167) (95) (173) (597) (745)

Charge-offs (437) (480) (651) (775) (2,343) (4,541)

Payments, sales and other (1) (953) (824) (993) (739) (3,509) (3,489)

Total outflows (2,505) (2,468) (2,895) (2,718) (10,586) (12,994)

Balance, end of period 12,193 13,007 13,460 14,284 12,193 14,662

Total nonaccrual loans $ 15,668 16,893 17,915 19,526 15,668 20,486

(1) Other outflows include the effects of VIE deconsolidations and adjustments for loans carried at fair value.

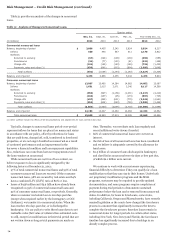

Typically, changes to nonaccrual loans period-over-period

represent inflows for loans that are placed on nonaccrual status

in accordance with our policy, offset by reductions for loans

that are paid down, charged off, sold, transferred to foreclosed

properties, or are no longer classified as nonaccrual as a result

of continued performance and an improvement in the

borrower’s financial condition and loan repayment capabilities.

Also, reductions can come from borrower repayments even if

the loan remains on nonaccrual.

While nonaccrual loans are not free of loss content, we

believe exposure to loss is significantly mitigated by the

following factors at December 31, 2013:

x 97% of total commercial nonaccrual loans and 99% of total

consumer nonaccrual loans are secured. Of the consumer

nonaccrual loans, 98% are secured by real estate and 64%

have a combined LTV (CLTV) ratio of 80% or less.

x losses of $938 million and $3.9 billion have already been

recognized on 35% of commercial nonaccrual loans and

52% of consumer nonaccrual loans, respectively. Generally,

when a consumer real estate loan is 120 days past due

(except when required earlier by the Interagency or OCC

Guidance), we transfer it to nonaccrual status. When the

loan reaches 180 days past due, or is discharged in

bankruptcy, it is our policy to write these loans down to net

realizable value (fair value of collateral less estimated costs

to sell), except for modifications in their trial period that are

not written down as long as trial payments are made on

time. Thereafter, we reevaluate each loan regularly and

record additional write-downs if needed.

x 66% of commercial nonaccrual loans were current on

interest.

x the risk of loss of all nonaccrual loans has been considered

and we believe is adequately covered by the allowance for

loan losses.

x $2.3 billion of consumer loans discharged in bankruptcy

and classified as nonaccrual were 60 days or less past due,

of which $2.1 billion were current.

We continue to work with our customers experiencing

financial difficulty to determine if they can qualify for a loan

modification so that they can stay in their homes. Under both

our proprietary modification programs and the MHA

programs, customers may be required to provide updated

documentation, and some programs require completion of

payment during trial periods to demonstrate sustained

performance before the loan can be removed from nonaccrual

status. In addition, for loans in foreclosure, some states,

including California, Oregon and Massachusetts, have recently

enacted legislation or the courts have changed the foreclosure

process in a manner that significantly increases the time to

complete the foreclosure process; therefore loans remain in

nonaccrual status for longer periods. In certain other states,

including New York, New Jersey and Florida, the foreclosure

timeline has significantly increased due to backlogs in an

already complex process.

70